The Biden administration is pursuing nothing short of a complete turnaround on taxation. One week after US President Joe Biden unveiled a $2 trillion infrastructure investment target, emerging details of the tax plan designed to pay for it have been met with much resistance by corporate America.

In summary, the ‘Made in America’ tax plan will mean significantly higher taxes for US corporations both domestically and abroad.

A US Treasury report released on 7 April outlines that the proposal would raise the US corporation tax rate from 21% to 28%.

On top of that, it would establish a minimum 15% tax on book income, because this profit reported to investors is routinely higher than the taxable income reported to US tax authorities, the report said.

For foreign earned income, the tax plan would double the rate at which overseas earnings are taxed from 10.5% to 21%. Any tax deductions claimed by companies that make payments to related parties in low-tax jurisdictions would be eliminated.

Because all this might entice companies to relocate from the US to low-tax jurisdictions through mergers and acquisitions, the plan proposes stronger “anti-inversion” rules.

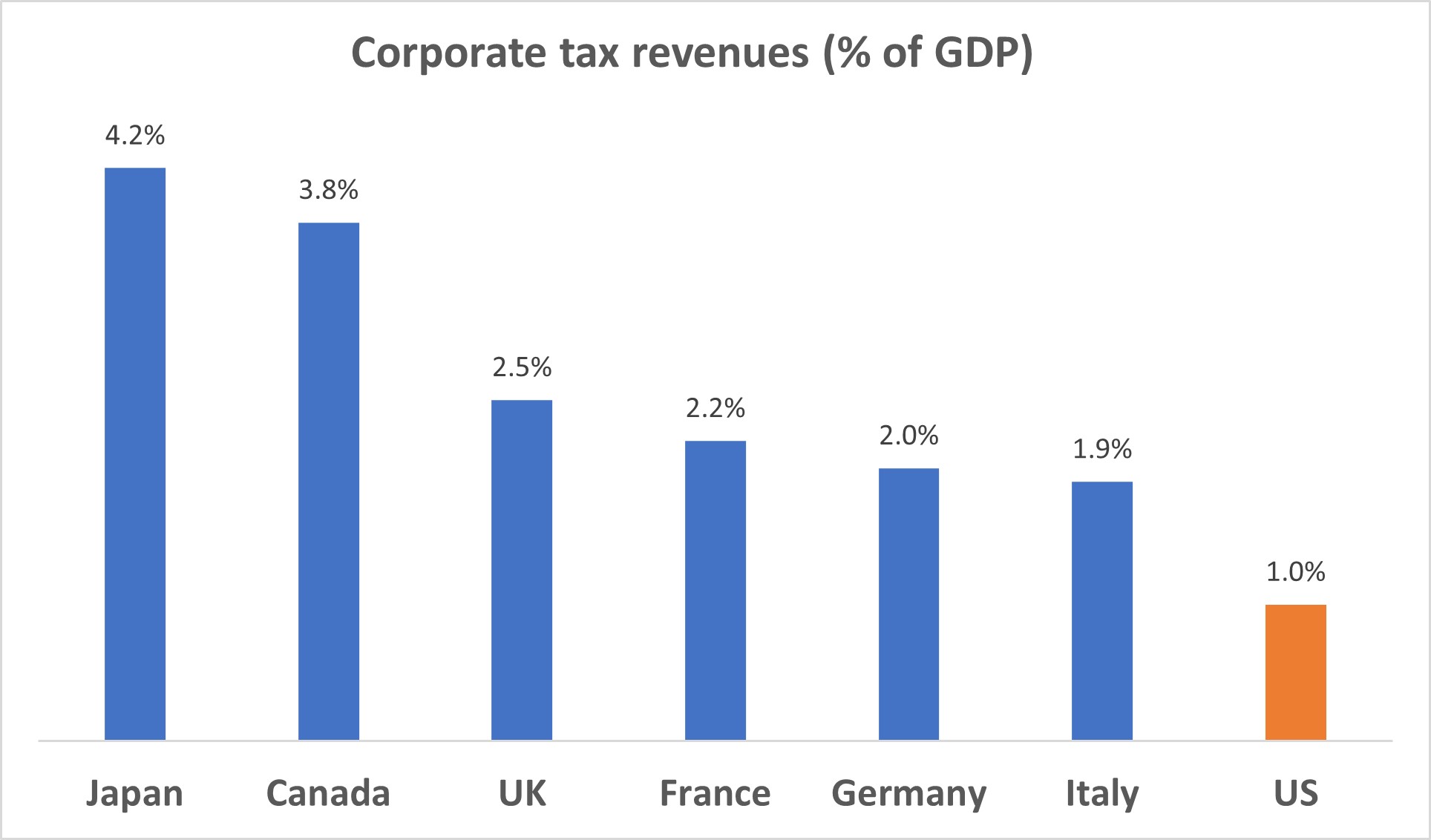

The US Treasury noted that corporate tax collections in the United States are at historic lows and well below what other countries collect.

Before the tax reform in 2017, US multinationals’ foreign profits were taxed at the domestic rate when repatriated to the US. This provided an incentive to keep those profits overseas.

Before the tax reform in 2017, US multinationals’ foreign profits were taxed at the domestic rate when repatriated to the US. This provided an incentive to keep those profits overseas.

Since then, U.S. firms have been subject to a minimum tax on their global intangible low-taxed income (GILTI). This tax exempts the first 10 percent of returns on foreign tangible assets, and GILTI is taxed at 10.5%, approximately half of the corporate tax rate.

But the Treasury suggests that the GILTI rate is too low, there are too many exemptions and the regime maintains profit shifting incentives because tax liabilities are calculated on a global basis.

Havens for US profits

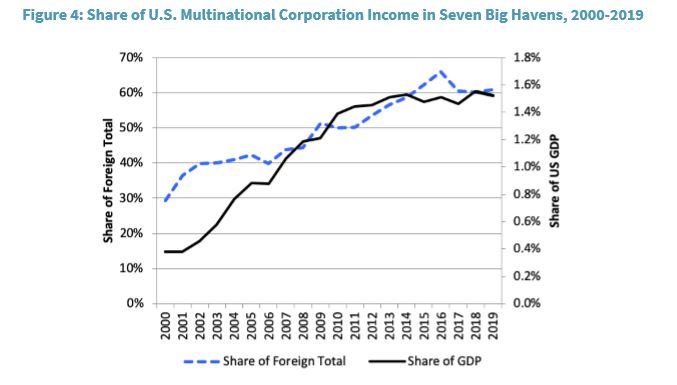

Because of this, the report noted, seven of the top 10 locations for the profits of multinationals in 2018 were in tax havens.

Bermuda alone accounts for 10% of all foreign profits reported by US multinationals. The share of total foreign income in the seven havens, including the Cayman Islands, were as high as before the tax reform at 61% of after-tax income, or 1.5% of GDP.

“Despite attempts to rein in profit shifting, tax havens are as available today as they were prior to the 2017 tax reform,” the US Treasury said.

In addition to doubling the tax rate for foreign earned income, the ‘Made in America’ tax plan would eliminate a tax exemption for the first 10% return on foreign assets and calculate the GILTI minimum tax on a per-country basis, thereby “ending the ability of multinationals to shield income in tax havens from U.S. taxes with taxes paid to higher tax countries”.

The Treasury Department and the Joint Committee on Taxation estimate this transition would raise more than $500 billion in revenue in the following decade.

In addition, the proposal would repeal and replace the Base Erosion and Anti-Abuse Tax (BEAT) to better counter the profit shifting foreign-headquartered multinationals.

In total, the plan would return more than $2 trillion in profits over the next ten years into the U.S. corporate tax base.

International cooperation

The new US administration recognises that for the proposal to work, it will need the support of most of the largest countries in the world.

US Treasury Secretary Janet Yellen has argued in favour of a global minimum corporate tax rate in a speech to the Chicago Council on Global Affairs on 5 April.

“Together we can use a global minimum tax to make sure the global economy thrives based on a more level playing field in the taxation of multinational corporations, and spurs innovation, growth and prosperity,” Yellen said.

The US administration believes countries worldwide are locked in a race to the bottom as far as corporate tax rates are concerned. In fact, the average statutory corporate rate among OECD countries has fallen from 32.2% in 2000 to 23.3% last year.

The Treasury report said, “When countries compete against each other to attract multinationals’ profits and activities by lowering their corporate rates, the result is a race to the bottom that makes it difficult for the United States—and other countries—to raise enough revenue to support necessary investments, and allows countries to try to gain a competitive edge by undercutting each other’s tax systems.”

The US government believes the President’s plan would provide a strong incentive to bring nations to the bargaining table and “join the United States in taking the first step to adopt strong minimum taxes on corporations”.

In recent years, countries, including the US, have worked under the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting to agree a reform of global corporate tax rules together with an agreed minimum rate that all multinationals must pay.

Under these plans, home countries of multinational corporations would apply a minimum tax when offshore affiliates are taxed below an agreed upon minimum tax rate.

Negotiations reached an impasse last year when attempts to counter tax issues arising from the digitalisation of the economy were perceived by the US as targeting predominantly American tech companies.

That resistance may have weakened now. EU countries and the UK have said this week any agreement on a global minimum rate would have to be tied to the reform of tax rules that would subject tech companies to pay taxes not only where they reside but also where they make substantial sales and have a large consumer base.

Germany and France have backed the US tax proposal and expressed optimism that together with Yellen a comprehensive agreement on both the taxation of digital services and a global minimum corporate tax rate could be reached in the summer.

This was confirmed on Wednesday when the US Treasury, with the aim of galvanizing OECD negotiations, sent out a document to the OECD Global Forum members laying out a proposal that would tax multinational companies based on their sales in each country rather than their physical presence, as is currently the case.

It may well be the bargaining chip for the US to demand a higher global minimum corporate tax rate.

So far, OECD discussions have focused on a 12.5% minimum tax rate, the same as Ireland’s.

The US would like to see a rate much closer to its proposed 21% GILTI rate, not least because Ireland has become a centre for US tech companies and the destination of many US corporate inversions for tax reasons.

Jude Scott, CEO of Cayman Finance said in a statement that his organisation “believes a global minimum tax should only be introduced if it is (a) fair to all countries, regardless of size or level of development, and (b) truly creates a level playing field for tax neutral jurisdictions with all jurisdictions offering preferential tax regimes, or providing tax neutrality through other means such as the use of tax transparent entities, such as exist in many OECD and EU jurisdictions”.

The framework proposed by the OECD for a global minimum tax presently falls short of these two principles and would need to be revised in several other areas.

Implementation

The implementation of a global minimum corporate tax rate will not be as straightforward as setting minimum rate, once this has been agreed.

The OECD proposal requires agreement on a set of interconnected rules that includes an Income Inclusion Rule, an Undertaxed Payments Rule, the Subject to Tax Rule, as well as agreement on the order of the rules, the calculation of the effective tax rate and the allocation of the top-up tax. There also needs to be agreement on the tax base, the definition of covered taxes and other technical matters, as well as exemptions.

Then there needs to be agreement on how America’s Global Intangible Low Taxed Income (GILTI) regime would be treated as compliant with these rules.

The objective is no less complex: it is to ensure that multinationals are taxed a certain minimum, while avoiding double taxation or taxation where there is no economic profit. The rules must cope with both different tax systems and business operating models. There should be a level playing field and transparency. And administrative and compliance cost should be kept as low as possible.

US businesses, trade associations and lobby groups have criticised the Biden tax plans for putting US companies at a competitive disadvantage and costing American jobs. It is, therefore, possible that plan might be watered down by lawmakers before it is adopted. Nevertheless, agreement on a global corporate minimum tax has become much more likely under the Biden administration.

Related Videos