High inflation and energy costs, lower unemployment but also slowing wage growth in a weakening economy, make up the picture that is emerging in many developed economies.

Both the US and Europe are recording the highest inflation rates in decades.

Inflation

In the Organisation for Economic Co-operation and Development area, inflation rose to 6.6% in the 12 months to December 2021, the highest rate since 1991. This compared with 5.9% in November 2021 and just 1.2% in December 2020.

High inflation was partially driven by Turkey (36.1%), but even if Turkey is excluded, inflation hit 5.6%. Energy prices alone were up 25.6% across OECD-member countries and food prices were 6.8% higher.

For 2021 as a whole, annual inflation in the OECD rose to 4.0%, compared with 1.4% in 2020, the highest annual average rate since 2000. Energy prices increased by 15.4%, the highest rate since 1981.

Employment

Unemployment meanwhile continued to decline in the area for the eighth consecutive month. It now stands at 5.4%, just 0.1 percentage point above the rate recorded before the COVID pandemic in February 2020.

In Australia, Chile, France, Iceland, Italy, Lithuania, Luxembourg, the Netherlands, New Zealand, Portugal, Spain and Turkey the unemployment rate is lower than before the start of the pandemic. In the euro area it has declined to 7%.

In the US and the UK, the employment market risks overheating with many companies reporting high vacancies and difficulties recruiting the workers they need.

Wage and income growth

However, despite the high inflation and comparatively low unemployment, wages are not expected to rise everywhere.

In the UK, the Bank of England projected last week the weakest post-tax labour income growth in more than seven decades with an expected decline of 2% this year and another 0.5% in 2023.

The BoE at the same time called for the moderation of wage growth, despite higher prices, to avoid an inflationary spiral and hitting private sector investments.

In the US, wage growth slowed to 1.2% in the fourth quarter of last year from 1.4% in the previous quarter, according to a US Department of Labour report.

But the slower pace, indicating an annual increase of about 5%, remains above the pre-pandemic trend of around 3%.

Hourly labour costs in the euro area rose by 2.5% year on year and in the EU by 2.9 % in the third quarter of 2021.

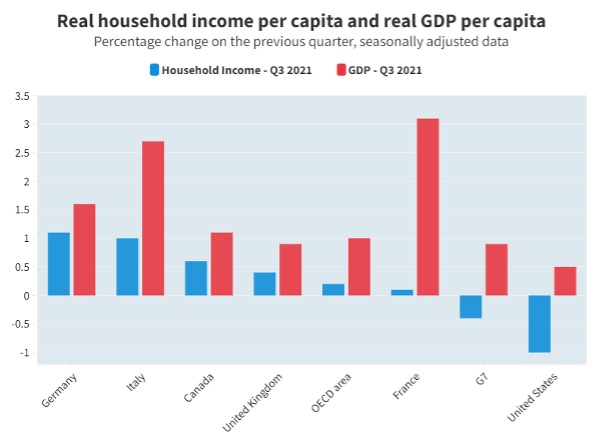

The level of household income per capita across the OECD area is now 4% higher than the pre-pandemic level recorded in the fourth quarter of 2019.

The level of household income per capita across the OECD area is now 4% higher than the pre-pandemic level recorded in the fourth quarter of 2019.

Despite two quarters of falling household income, real household income per capita in the US was 5.6% higher in the third quarter 2021 than before the pandemic and in Canada it was up 7.9%.

Economic outlook

Going forward, most metrics point to moderating economic growth.

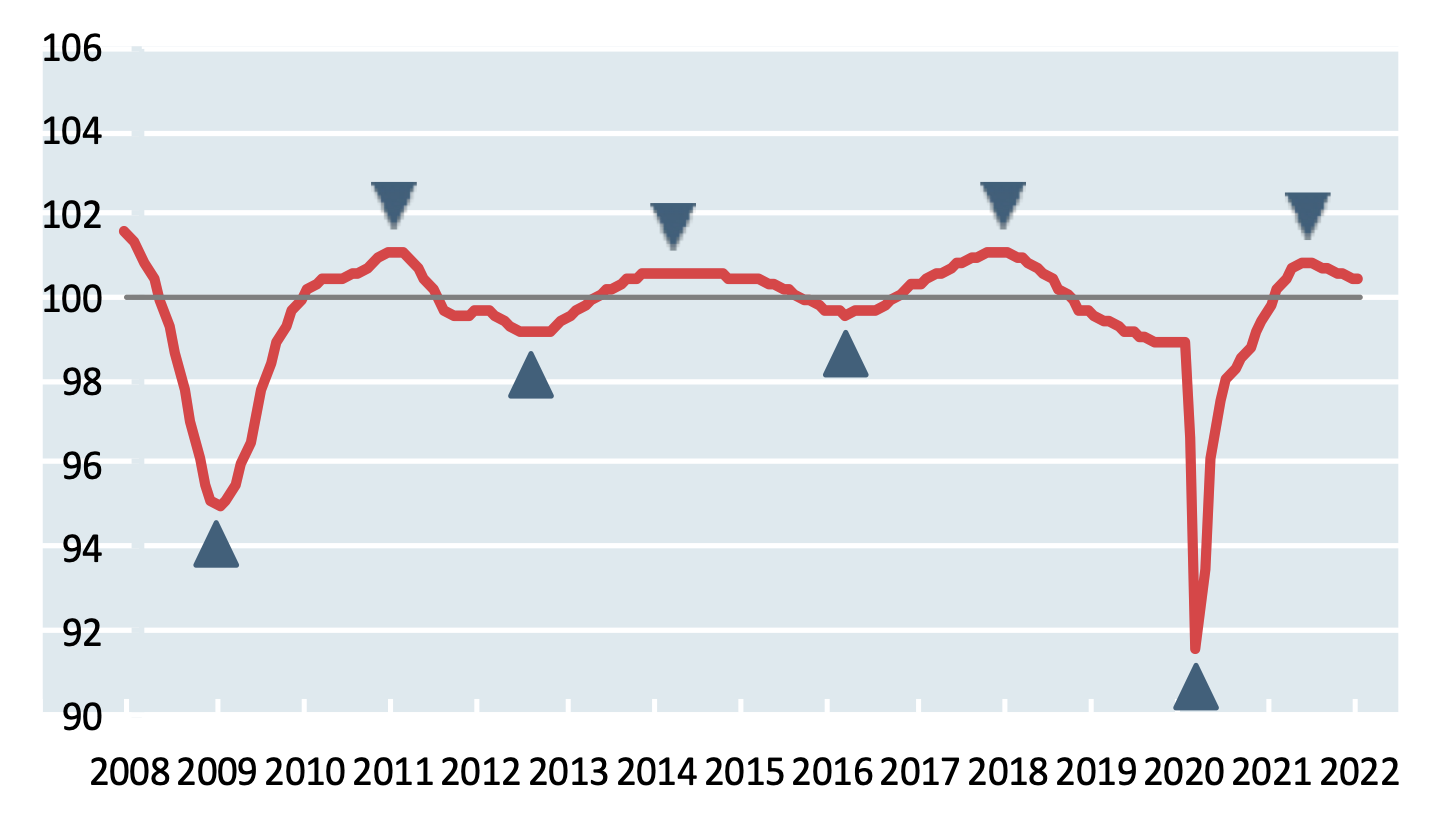

OECD composite leading indicators, which attempt to predict fluctuations in economic activity over the next six to nine months, show that Canada, Germany, Italy and the UK have likely passed a turning point in economic activity with more moderate growth to follow.

In the US, Japan and the euro area as a whole, the CLIs, which for example include order books, confidence indicators, building permits or new car registrations, have also passed a cyclical peak, but have since remained relatively stable.

Among the major emerging-market economies, leading indicators for China’s industrial sector show a loss of momentum, similar to India, and slower growth in Brazil.

In Russia, the leading indicators point to stable growth.

Related Videos