To say that 2022 was a difficult year for crypto is an understatement.

Dramatic declines in asset values, stablecoin collapses, bankruptcies of what appeared to be some the industry’s largest and most successful businesses, and widespread contagion meant a near-death experience for any digital asset venture.

The slashing of workforces and changes in senior management were the norm. What was first described as a crypto winter, increasingly felt like an ice age.

Yet, at the beginning of last year, it was not at all clear that 2022 would easily become the worst year for the crypto industry, the effects of which will be felt for years to come.

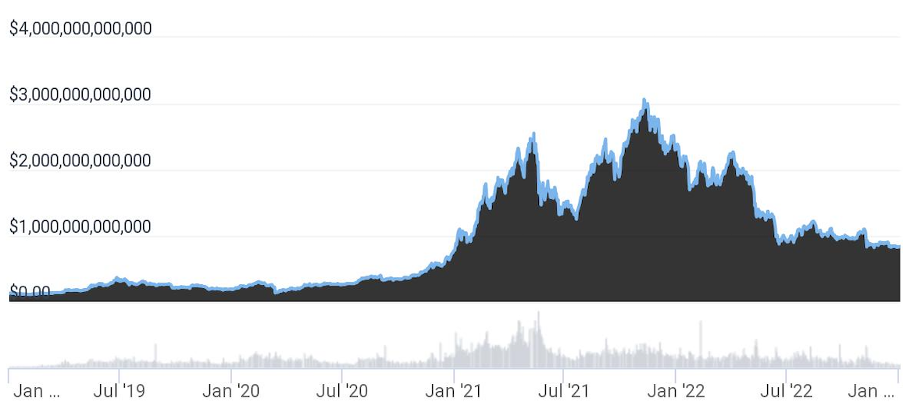

Bitcoin’s value had peaked at US$69,000 in November 2021 and most forecasters predicted a solid year for the industry.

Earlier in the year, venture capital firms continued to pour money into crypto investments. Crypto exchange FTX was one of many digital asset ventures that raised private funding in early 2022, valuing the business at $32 billion.

The market for non-fungible tokens boomed with a record monthly trading volume of $17.2 billion in January.

Bitcoin even recovered from a January collapse to $36,000, reaching $47,000 by the end of March.

Legislators in the United States and Europe announced measures, such as President Joe Biden’s Executive Order on Ensuring Responsible Development of Digital Assets or the European Union’s Markets in Crypto Assets Regulation, that vowed to coordinate regulatory efforts while enabling innovation.

Although the industry views regulation with skepticism, many believed that some added regulatory credibility could pave the way for wider mainstream adoption.

Terra implodes

That was all put into question in May when TerraUST, an algorithmic stablecoin and sister token LUNA imploded, wiping out almost $40 billion within a week.

Unlike collateralised stablecoins, like Tether or USD Coin, the algorithmic coin was initially backed only by a mint-and- burn mechanism linked to its sister token. Built-up reserves were held in the form of bitcoin and other cryptocurrencies, whose values plummeted at the first sign of a crisis.

Investors use stablecoins to hold their assets almost like cash, because it is more convenient and avoids the fees of converting them into actual fiat currency.

This meant the exposure to the failing stablecoin was large and far-reaching.

Equity investors in Terra lost money, and so did investors who were holding positions on Anchor, Terra’s high-yield staking protocol.

The firms with the largest exposure to the collapse included cryptocurrency hedge fund Three Arrows Capital (3AC) and crypto lenders Celsius Network and Voyager Digital, which have all filed for bankruptcy.

3AC, one of the most successful crypto funds, held the biggest position on Terra’s until-then profitable Anchor protocol.

The contagion spread even further because the almost $3 billion-hedge fund had borrowed widely, taking – some previously undisclosed – loans from Celsius, BlockFi, Genesis, Voyager Digital and exchanges like BitMEX and FTX.

At the time, FTX co-founder Sam Bankman-Fried appeared to be the saviour of the industry, offering to support failing businesses with loans and equity injections. BlockFi received money from FTX US and Bankman-Fried’s trading firm Alameda Research granted two lines of credit to Voyager.

The FTX CEO’s white knight image changed less than six months later when his own company filed for bankruptcy, and Bankman-Fried was arrested on fraud charges.

The allegation, which has been admitted by chief executive officer of Alameda Research Caroline Ellison and FTX co-founder Gary Wang in court, is that Alameda Research itself suffered large losses from the collapse of Terra. To cover up the losses, FTX moved client funds to Alameda.

FTX was not just a large cryptocurrency bankruptcy, it was the largest corporate bankruptcy of 2022. The 50 largest creditors are owed $3.1 billion, and the exchange had up to one million registered users.

Despite all that, crypto analytics firm Chainalysis has pointed out that FTX was not even the biggest calamity for investors this year.

“Both the depegging of Terra’s UST token and the collapse a few weeks later of Celsius and Three Arrows Capital (3AC) drove much bigger realized losses for investors: $20.5 billion in the case of UST and a whopping $33.0 billion in the case of Celsius and 3AC, versus just $9.0 billion for FTX,” Chainalysis summarised its own analysis.

Still, it is unlikely that the contagion will stop with FTX. BlockFi, barely saved by FTX in June, has filed for bankruptcy and crypto lender Genesis, owned by Digital Currency Group, has also been hit by the exchange’s collapse.

While the dust has not yet settled, Bitcoin fell 64% last year to $16,600. Ethereum, trading at around $1,200, is 70% off its value a year earlier and Solana, a token backed by Bankman-Fried was down 95% from its peak in November 2021. The trading volume of NFTs has almost entirely evaporated, down 97% from its peak in January 2021.

The market capitalisation of all cryptocurrencies has dropped from more than $3 trillion in November 2021 to just about $830 billion today, according to Coin Gecko.

Cayman exposure

FTX was headquartered in the Bahamas and had no significant affiliates in Cayman. This does not mean that the islands were left untouched by the digital asset crisis.

The new management of the part of FTX Group that is undergoing Chapter 11 in the United States has told the bankruptcy court that a quarter of FTX clients are based in the Cayman Islands.

Although this was not backed up by any data, and creditors are currently fighting in court to keep their names anonymous, this is likely a reference to the volume of investments made by trading firms registered in Cayman, as FTX was known as a trader-friendly exchange, offering leverage for investments.

3AC was registered in the British Virgin Islands but parts of the liquidation have touched on Cayman. The BVI liquidators have sought recognition of the Cayman courts, stating that some of the company’s assets appear to be on island.

A Cayman company used to commission a yacht from a shipyard in Italy for the company co-founder Zu Shu applied for court supervision of its voluntary liquidation in December. The company’s biggest creditor is 3AC.

How many Cayman funds and companies invested with 3AC or lent money to the hedge fund is not yet clear.

Earlier in the year, the collapse of Terra forced the closure of two Cayman-based funds managed by Invictus Capital, which also held assets with failed crypto lender Celsius.

Although the reputational fallout of FTX’s failure may still see all offshore financial centres tarnished with the same brush, the events of last year appear to justify Cayman’s cautious approach to regulating digital asset businesses.

So far, only 18 entities have obtained virtual asset service provider licenses from the Cayman Islands Monetary Authority. All of them are institutional rather than consumer focused.

But many more crypto companies are operating entities like holding companies or investment arms without a VASP licence. Decentralised autonomous organisations (DAOs), for instance, frequently use Cayman-based foundation companies for their legal entity structure but leave the digital asset operations to entities in the BVI or Panama.

The Cayman Islands government is currently revising its digital asset legislation to make it more commercially friendly.

This will be a difficult balancing act given the flux that the industry is undergoing.

More regulation coming

What was certainly a difficult year for any type of investment, including stocks and bonds, in traditional finance, has become an existential crisis for digital assets.

More regulation is almost inevitable. The arrest of Bankman-Fried, a large political donor and the industry’s biggest lobbyist for responsible regulation, is going to make lawmakers, in the US and elsewhere, less inclined to err on the side of a laissez-faire approach to digital assets.

Centralised exchanges that combine several functions, from deposit-taking, custody and market-making to margin lending, which in traditional finance are segregated, are in the spotlight.

Whether self-regulation by exchanges in the form of more transparency through audited reserve holdings is sufficient remains to be seen, particularly because many reputable audit firms have been dropping crypto mandates.

Decentralised finance (DeFi) with its decentralised exchanges, futures and securitised lending protocols always seemed more like a playground for margin and day traders, craving little to no regulation, rather than a sensible investment market for the average consumer.

Whatever shape future regulation is taking, at this stage the most probable way for crypto to be accepted is by becoming regulated and more like the old traditional financial system, taking it away from its core decentralised ideals.

Digital gold

Even for experienced investors, the value of bitcoin and other crypto assets remains incredibly volatile.

The last two to three years have cast doubts on digital assets as an uncorrelated asset class for investors. While correlations were low when stock markets were rising, crypto displayed a high correlation with falling equities.

The value of bitcoin and other cryptocurrency is largely dominated by the inflow or outflow of institutional investor money into the space. The general risk-off sentiment among institutional investors in 2022 dragged the crypto market with it, even before spectacular collapses led to contagion among key players.

At this stage, the crypto market is almost devoid of any large institutional investors.

Many in the industry underestimated just how much crypto asset values had benefited from quantitative easing and how much they would be hit when the free flow of money was curtailed.

Far from being the often-promised inflation hedge, crypto asset values were heavily influenced by the US Federal Reserve’s monetary policies. While in the past, interest rate hikes had driven digital asset values in either direction, there was only one response to last year’s seven interest rate actions: Down.

Changing narratives

All this leaves the crypto market struggling to define its identity, not only for investors as a speculative asset or store of value but in general. In contrast to traditional finance, which trades in or lends against real world assets, digital assets are almost entirely built on trust.

This trust has been shaken and the need for crypto is more than ever in question.

The digital asset industry has long struggled with its ever-changing narratives, accompanied by cheerleading hyperbole that promised to change the world with killer apps, just like the internet had done.

When Bitcoin first emerged, it was touted to be a technological revolution that would disrupt cross-border payments by cutting out inefficient middlemen via a decentralised, immutable and transparent peer-to-peer mechanism.

The Bitcoin white paper foresaw a transformation that would make sending payments to family and friends, as well as for commerce, as easy, cheap and fast as sending email.

More than a decade later ,the mechanism exists and functions perfectly well, but none of the predictions have come true. In fact, almost the exact opposite is the case.

Using cryptocurrencies for payments proves to be onerous, cumbersome, expensive, fraught with cybersecurity and other risks, and in some cases is not even fast.

What’s more, to gain access to crypto, the average consumer needs new, often less regulated, middlemen in the form of centralised exchanges.

So, a few years ago, the narrative changed.

New crypto advocates started to argue that rather than being a payment mechanism, it was the underlying blockchain or decentralised ledger technology (DLT) that would drive change and produce new, more efficient plumbing for anything from stock trading to managing supply chains.

But by 2022 most optimistic press releases had been replaced by announcements of blockchain venture closures and abandoned DLT projects.

Last year, the Australian Stock Exchange had to write off US$168 million on the development of a blockchain-based clearing and settlement mechanism for stocks. Similar projects in insurance for claims and settlement systems, as well as in banking, also failed.

Maersk and IBM announced in November that their supply-chain solution for shipping using blockchain technology was not commercially viable.

The more dominant narrative is now that the technology will power Web3, a new iteration of the internet, and underpin commerce in the fully immersive, virtual reality metaverse.

That may still happen, but the changing visions and promises give the impression of a technology looking for a purpose, rather than one that is serving a need.

In any case, building trust and the belief in a need for digital assets is more difficult now than it was a decade or even a year ago.

However, just like the 2008 financial crisis did not bring the end of hedge funds or mortgage-based securities, digital assets will recover under a different regulatory rulebook.

For crypto assets and the underlying technology to thrive, they will ultimately need to be more integrated into traditional finance. This in itself poses a much greater risk to financial stability and calls for more serious regulation.

Related Videos

excellent, informed and informative journalism

Like keyless car entry systems crypto currencies are a brilliant idea in search of a purpose.

No ordinary person, not involved in drug dealing, money-laundering etc. has any need for crypocurrencies.