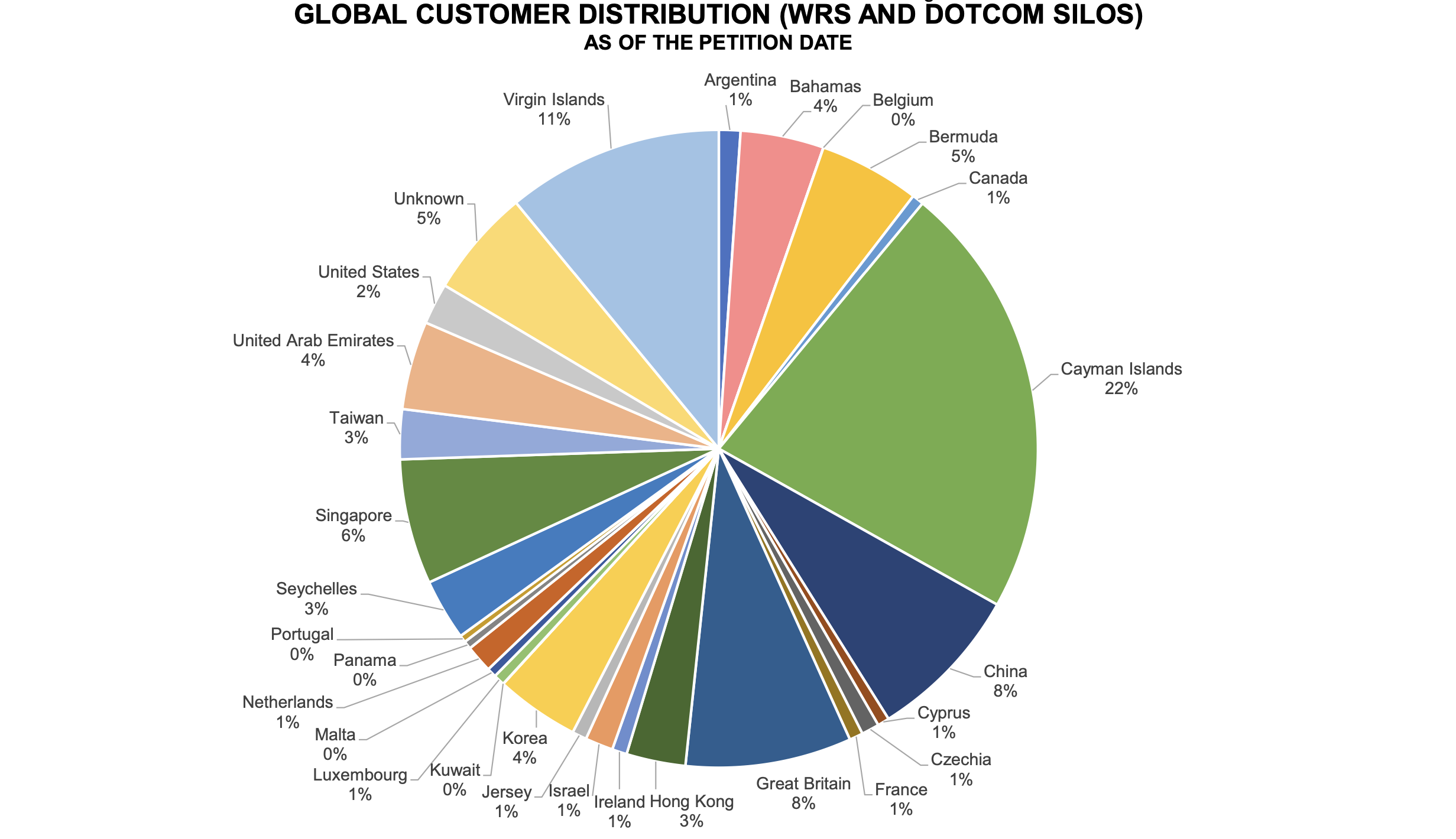

The administrators of collapsed crypto exchange FTX and related companies have claimed in a court filing that most of the group’s customers are from the Cayman Islands.

A chart titled ‘Global Customer Distribution’ annexed to a court application shows the Cayman Islands has a 22% share, followed by the British Virgin Islands with 11% and China and the UK with 8% each.

According to a separate court filing in federal bankruptcy court in Delaware, the 50 largest debtors of the group alone have claims for more than US$3 billion. The top 10 claimants are said to be owed more than $100 million each. The largest debtor has a claim for $226 million.

The names and addresses of the largest debtors are all anonymised.

Judge John T. Dorsey, who is overseeing the FTX bankruptcy case, approved a request, on an interim basis, from the debtors’ attorneys to redact the names of FTX’s creditors.

Earlier this year, FTX was valued by private investors at $32 billion, but the lawyers for FTX said it may have been more than $40 billion for the group.

Puzzling data

On the face of it, the 22% share of Cayman customers makes little sense.

In a bankruptcy filing on 14 Nov., FTX said that it has more than 100,000 creditors but that the figure could exceed 1 million.

Last year, the crypto exchange said it had more than 1.2 million registered users. If the percentage refers to users, the number would be larger than Cayman’s population and registered companies combined.

Offshore jurisdictions make up more than a third of FTX customers according to the data.

It is possible that users may have claimed to be from the Cayman Islands during the onboarding process and that FTX did not verify the information as part of its customer due diligence.

Typically, during registration crypto exchanges require a scan of a passport or other identification document, together with a photo and sometimes a utility bill.

Other countries appear to be underrepresented in the chart. According to Chainalysis data from last year, crypto adoption and transactions soared in Africa, in particular Nigeria and Kenya. Yet, these countries do not feature in the chart at all. Latin American countries are equally underrepresented or missing.

Exposed institutional investors

The other explanation could be that the chart refers to the dollar amount, rather than customers, and that investments would come from crypto investment funds. The high share of Cayman, BVI and Bermuda customers would point to corporate investment structures.

But, so far, not enough funds have come forward declaring they have funds tied up in FTX to explain Cayman’s 22% share.

Industry body Crypto UK told the Treasury select committee of the UK Parliament on 14 Nov. that most of the affected FTX customers were institutions.

FTX rival and leading cryptocurrency exchange Binance revealed that it previously held $580 million of FTX’s native token FTT and had only sold a portion. A Binance holding company is incorporated in the Cayman Islands.

Venture capital firm Sequoia Capital has marked its $213.5 million investment in FTX to zero, while Singapore’s state-owned holding company, Temasek, reportedly lost $205 million.

Crypto asset manager Ikigai said a large majority of the hedge fund’s total assets were placed with the collapsed exchange, and crypto lender Galaxy Digital stated it had lost $77 million.

Hedge fund Galois Capital said it had about $100 million stuck in FTX, while crypto broker Genesis Trading disclosed on 10 Nov. that it had about $175 million in locked funds on the exchange.

Stock market-listed exchange Coinbase, meanwhile, has lost $15 million.

Other companies that have reported at least some exposure to FTX include crypto-focused investment giant Pantera Capital, venture capital firm Multicoin Capital, digital asset investment and trading group CoinShares, Liquid Meta, stable coin issuer Circle, the trading arm of Amber Group, Wintermute, Crypto.com and Voyager Digital.

How many of these companies are exposed through Cayman-based entities is not known.

Unreliable information

It is not clear how much faith FTX’s new management has in the data presented to the court. John Ray, the group’s new CEO, is a restructuring specialist who oversaw the Enron bankruptcy. He told the court last Saturday in a filing he had never seen “such a complete failure of corporate controls and such a complete absence of trustworthy financial information”.

According to Ray, the company failed to keep proper books, records or security controls for the assets that it held on behalf of customers.

At a hearing on Tuesday, lawyers for FTX told the court the customer distribution is “as of the petition date based on the best information that we have”.

They said that 94% of customers belonged to FTX Trading Ltd, the US arm of the crypto exchange, while only 6% were customers of FTX Digital Markets Ltd, a Bahamian entity that on paper served the much larger international market.

That was because in May 2022, FTX never transferred its non-US customers to its new entity in the Bahamas, where FTX was headquartered.

The new management of FTX has established four silos for the company’s assets and various entities. The customer chart refers to two of them: the WRS (West Realm Shires) silo, which encompasses US holdings; and the dotcom silo, which includes the exchanges and international business.

Two other silos cover Alameda research, FTX founder Sam Bankman-Fried’s hedge fund and a venture silo of investments in crypto businesses.

James Bromley of law firm Sullivan & Cromwell told the bankruptcy court on Tuesday that a “substantial amount of assets” have either been stolen or are missing.

He said the company was run “as a personal fiefdom of Bankman-Fried”.

Almost $300 million had been spent on real estate in the Bahamas, which consisted largely of homes and vacation properties for senior executives.

“We have witnessed probably one of the most abrupt and difficult collapses in the history of corporate America,” Bromley added.

He said the company had failed because of a run on the exchange as well as a leadership crisis.

Related Videos