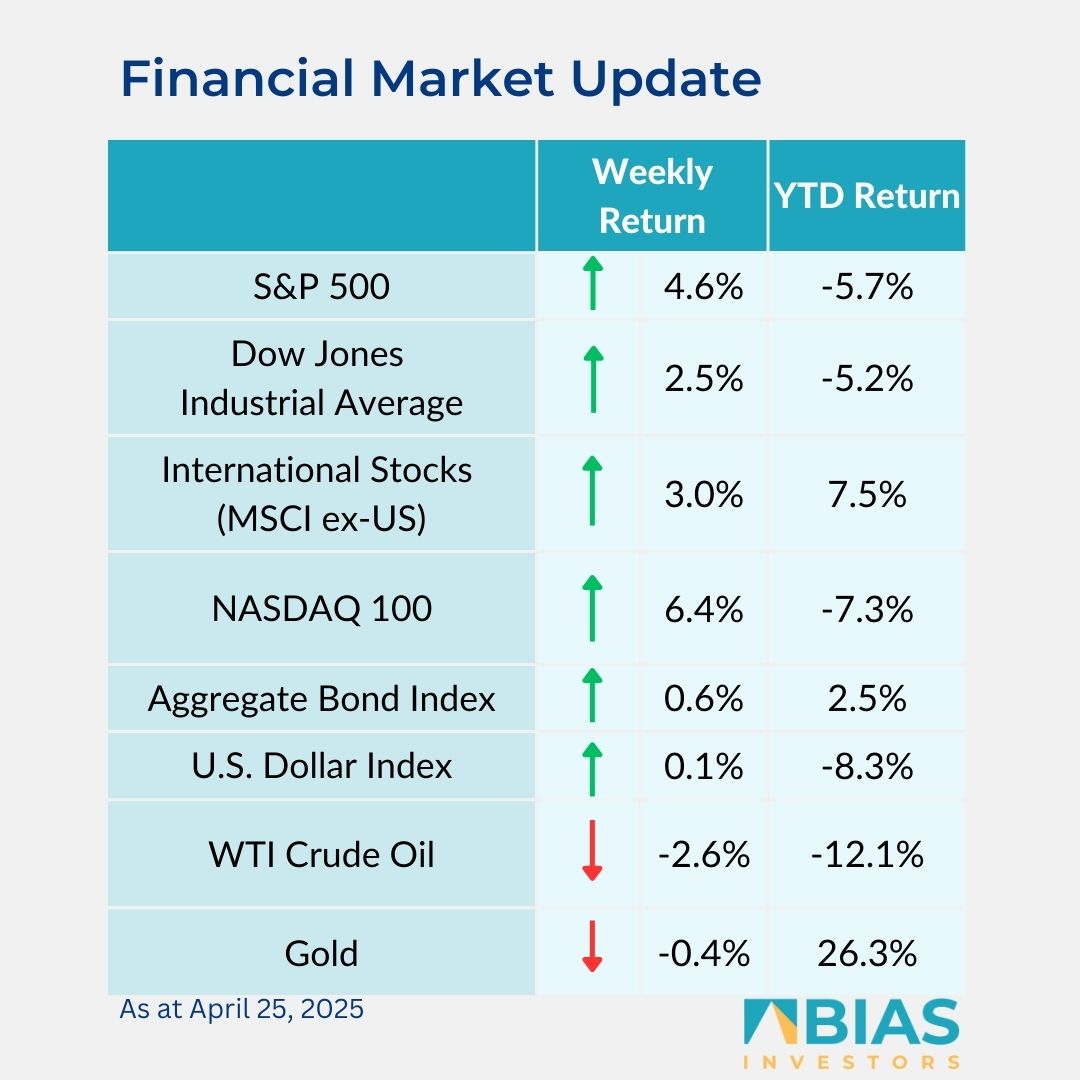

Equity markets clawed back some of their recent declines last week.

For the week, the S&P 500 Index was +4.6%, the Dow Jones Industrials +2.5%, and the NASDAQ +6.4%. The S&P 500 Index was led by the technology, consumer discretionary, and communication services sectors, while the consumer staples, real estate, and utility lagged.

The 10-year US Treasury note yield decreased to 4.260% at Friday’s close versus 4.337% the previous week.

This week brings multiple data points to assess the health of the economy. First quarter gross domestic product (GDP) and the March Personal Consumption Expenditures (PCE) Price Index are both scheduled for release on Wednesday. The April Employment Report is scheduled for Friday.

These reports should provide an early read, or at least a baseline, on any impact of tariffs on economic growth, inflation and employment.

The outlook for monetary policy has been in flux because of the economic policy rollout from the new administration. There is no change expected to the current 4.25% to 4.50% Fed funds target range at the 7 May Federal Open Market Committee (FOMC) meeting, but CME Fed funds futures indicate there could be up to 0.75% in reductions to the Fed funds rate by December.

First quarter earnings season continues this week with 180 companies in the S&P 500 Index scheduled to report earnings results. First quarter 2025 earnings growth is currently forecast at 10.1% year-over-year with 4.6% revenue growth. Full-year 2025 earnings are expected to grow by 9.7% with revenue growth of 5.0%.

In our ‘Dissecting headlines’ section, we look at expectations for the upcoming economic data.

Dissecting headlines: Economic pulse

The uncertainty hanging over the investment markets for the past few months has been a concern over how tariff and other fiscal policy initiatives from the Trump administration would impact economic growth, inflation, and employment. This week brings data on all three.

For economic growth the first quarter GDP is currently expected to show 2.3% growth year-over-year. Tariffs should not have had much specific impact on economic growth, as much of the change in tariff rates did not occur until later in the quarter or into the start of the second quarter, but it may have impacted some behaviour in advance of tariffs going into effect. The report should provide a good baseline for economic impact over the balance of the year.

For inflation, the March Personal Consumption Expenditures (PCE) Price Index is expected at +2.2% year-over-year and core PCE, which excludes the impact of food and energy prices, is expected at +2.6%. The PCE is the Fed’s preferred measure of inflation, so this report will help shape the monetary policy discussion at the May FOMC meeting.

For employment, the April Employment Situation Report is expected to show 130,000 growth in non-farm payrolls, down from 228,000 in March, and the unemployment rate is expected to remain steady at 4.2%.

At the March FOMC meeting, the committee members projected 2025 unemployment at 4.4%, so there is room for some weakening in the labour market under the Fed’s current forecast.

Several Federal Reserve officials have said that data on the economic impact of tariffs is important to properly make decisions on monetary policy. This week should be a good start to several months of data to consider.

![]()

BIAS Investors

24 Howard Street

Corporate Plaza Suites #81

Godfrey Nixon Way

George Town, Grand Cayman

Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos