CFA, MBA

Chief Investment Officer

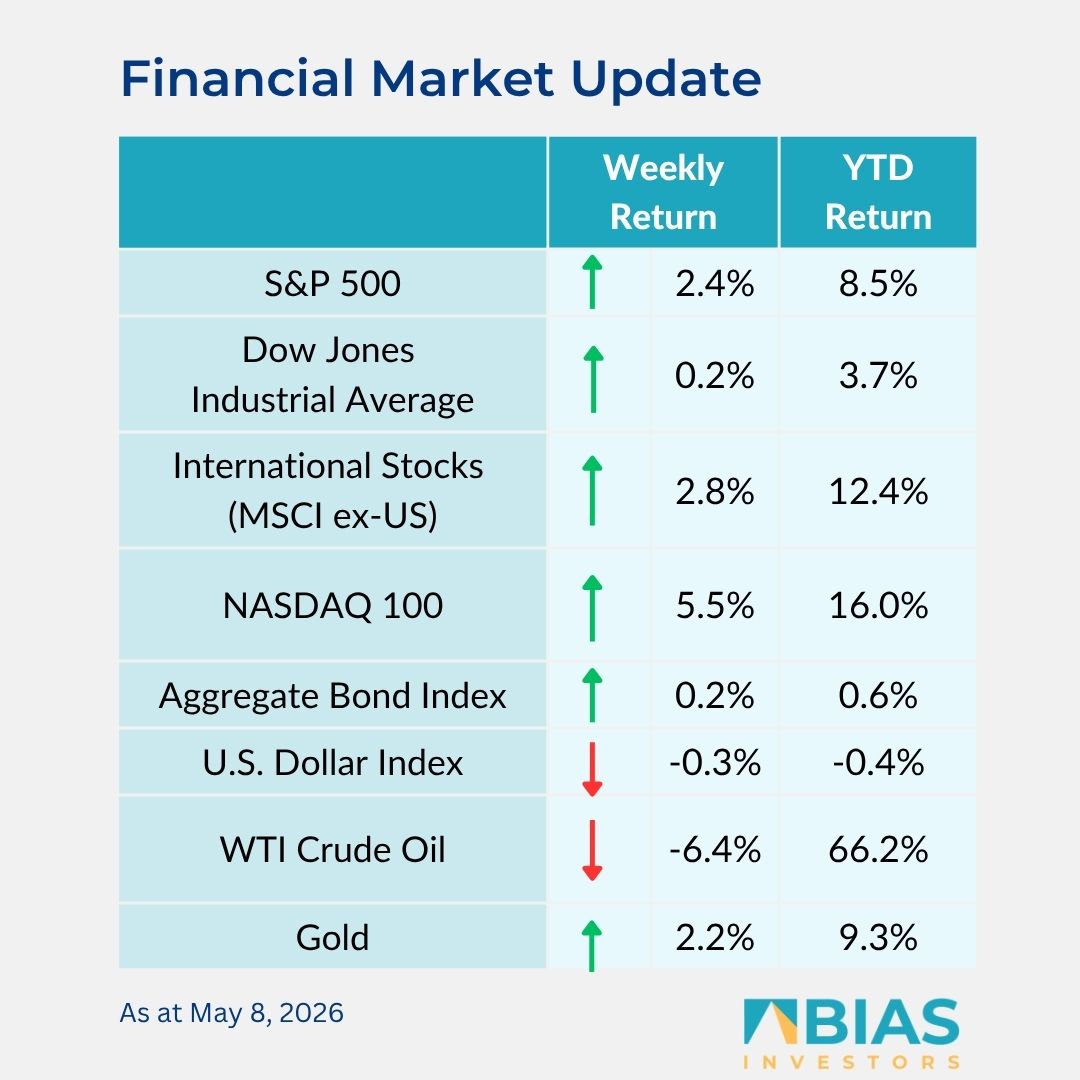

Rising earnings, decreasing geopolitical tensions, and healthy job growth pushed equities higher for the sixth consecutive week.

For the week, the S&P 500 Index was +2.4%, the Dow Jones Industrials +0.2%, and the NASDAQ +5.5%. The technology, communication services, and consumer discretionary sectors led the S&P 500 Index for the week, while the energy, utilities, and financial sectors lagged.

The 10-year US Treasury note yield was 4.366% at Friday’s close versus 4.383% the previous week.

The April employment report showed a stable labour market, with a net gain of 115,000 jobs versus an expectation of around 67,000 jobs and an unchanged unemployment rate at 4.3%.

This week we should see data on inflation for April with the Consumer Price Index report scheduled for Tuesday and the Producer Price Index report scheduled for Wednesday.

A Senate vote is expected this week on Kevin Warsh’s nomination to be the next Federal Reserve chairman. Current chairman Jerome Powell’s term expires this Friday, 15 May. This would put Warsh in position to preside over the next Federal Open Market Committee (FOMC) meeting in mid-June when the committee should publish its updated Summary of Economic Indicators to set its policy path for the second half of the year.

With 89% of companies in the S&P 500 Index already reported, the quarterly earnings reporting period continues this week with another 11 companies scheduled to report results.

First-quarter earnings are expected to grow by 27.7% and quarterly revenue growth is expected at 11.3%. Full-year 2026 earnings are expected to grow by 21.0% with revenue growth of 10.1%.

In our ‘Dissecting headlines’ section, we look at the state of the Federal Reserve that the new chairman is set to inherit.

Dissecting headlines: Inheriting the Fed

If Kevin Warsh is confirmed this week as the next Federal Reserve chairman, he takes on the Fed’s dual mandate of price stability and maximum sustainable employment.

On the first mandate, he oversees an inflationary environment, that while not at the extremely elevated 2022 levels, is still above the long-run goal of 2%.

The March report on Personal Consumption Expenditures (PCE) showed PCE prices 3.5% higher from a year earlier, and core PCE Prices – which exclude the impact of food and energy prices – 3.2% higher.

Improvements in core inflation are being counterbalanced by the current rise in energy prices due to the conflict in the Middle East. The impact of tariffs also still lingers as part of inflation concerns. Current PCE prices are well above the Fed’s forecast of 2.7% PCE prices and core PCE prices for 2026, and 2.2% for 2027.

On the second mandate, the labour market has surprised to the upside the past two months in job creation, but lay-off announcements, particularly in the technology sector, and the shift in potential job growth paths due to AI, create concerns. The current unemployment rate is 4.3% and inline with the Fed’s forecast of 4.4% for 2026, and 4.3% for 2027.

The new chairman will also inherit a balance sheet that is extremely large versus historical averages. The Fed balance sheet peaked in early 2022 as the Fed was purchasing treasury and mortgage debt to maintain liquidity in the economy during the pandemic.

That has been winding down for the past few years and is now around $6.6 trillion from its 2022 peak of almost $9 trillion. This is substantially higher than before the 2008 financial crisis when the balance sheet was less than $1 trillion and only around 6% of Gross Domestic Product (GDP). The current balance sheet is more than 20% of GDP.

Lastly, the newcChairman will need to contend with a Federal Open Market Committee (FOMC) that is not aligned on policy. There have been dissent voters at the past two FOMC meetings, with some advocating for higher rates and some for lower rates.

Building consensus and communicating that policy outlook at the June meeting will be an important first step early in his term.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos