CFA, MBA

Chief Investment Officer

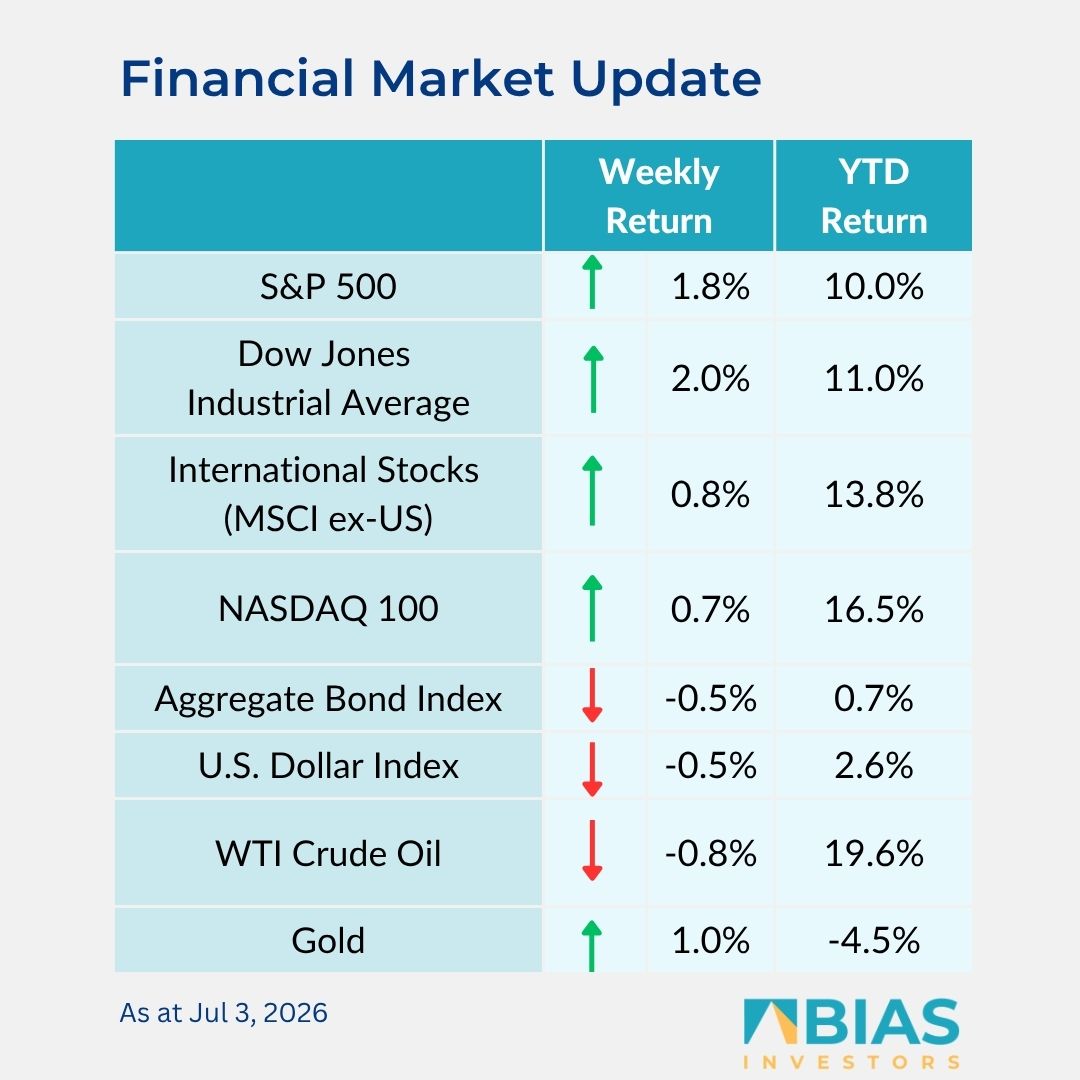

Equities closed the holiday-shortened week higher.

For the week, the S&P 500 Index was +1.8%, the Dow Jones Industrials +2%, and the NASDAQ +0.7%. The communication services, financials, and consumer discretionary sectors led the S&P 500 Index for the week, while the real estate, utility, and energy sectors lagged. The 10-year US Treasury note yield was 4.471% at Thursday’s close versus 4.370% the previous week.

Energy prices continue to decline. The national average price for regular unleaded gasoline peaked at $4.56 per gallon on 21 May before declining 16.6% to $3.80. Diesel fuel prices peaked at $5.40 per gallon on the same date and have since fallen 11.5% to $4.78.

The June Employment Situation report showed a net gain of 57,000 jobs versus an expectation of 110,000, and both with May and April job growth was revised lower.

The June unemployment rate fell to 4.2% from 4.3% in May due to a declining labour force participation rate. This weaker labour report, combined with lower energy prices, could slow some of the recent hawkish posture of the Federal Reserve.

Current CME Fed funds futures currently show a single 0.25% interest rate increase at the September meeting, in line with the recent policy projection from the Federal Open Market Committee.

There are three companies in the S&P 500 Index scheduled to report earnings this week. Second-quarter earnings are expected to grow by 23.3%, and quarterly revenue growth is expected at 12.2%. Full-year 2026 earnings are expected to grow by 24.1% with revenue growth of 10.8%.

In our ‘Dissecting headlines’ section, we look at investor sentiment to start the second half of the year.

Dissecting headlines: Market sentiment

Despite projections for more than 20% earnings-growth, and falling energy prices, investor sentiment is Bearish entering the second half of the year.

The American Association of Individual Investors Sentiment Survey has Bearish sentiment at 42.3% versus Bullish sentiment at 31.4% in its recent weekly survey.

The survey measures whether investors think the stock market will be higher or lower in the next six months. Bullish sentiment is below its historical average of 37.5%. Bearish sentiment is well above its historical average of 31.0%.

Periods of unusually bearish investor sentiment have often preceded above-average equity returns in the following 6-12 months, while excessive optimism has tended to be associated with more muted forward returns.

The CNN Fear & Greed Index currently has a reading of 34, which signals ‘Fear’. This index is made up of seven indicators to include stock price strength, market breadth, the put-call ratio, market volatility, difference in stock and bond returns, and junk bond demand.

Investor sentiment can swing quickly based on market movement or news. In the first half of 2026, the AAII index has seen Bullish sentiment as high as 49.5% and as low as 30.4%, and the Bearish sentiment has been as high as 52% and as low as 27.0%. Likewise, year-to-date, the CNN Index has been as high as 71 indicating ‘Greed’ and as low as 6% indicating ‘Extreme Fear’.

Markets can perform well when investors are climbing a wall of worry.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos