CFA, MBA

Chief Investment Officer

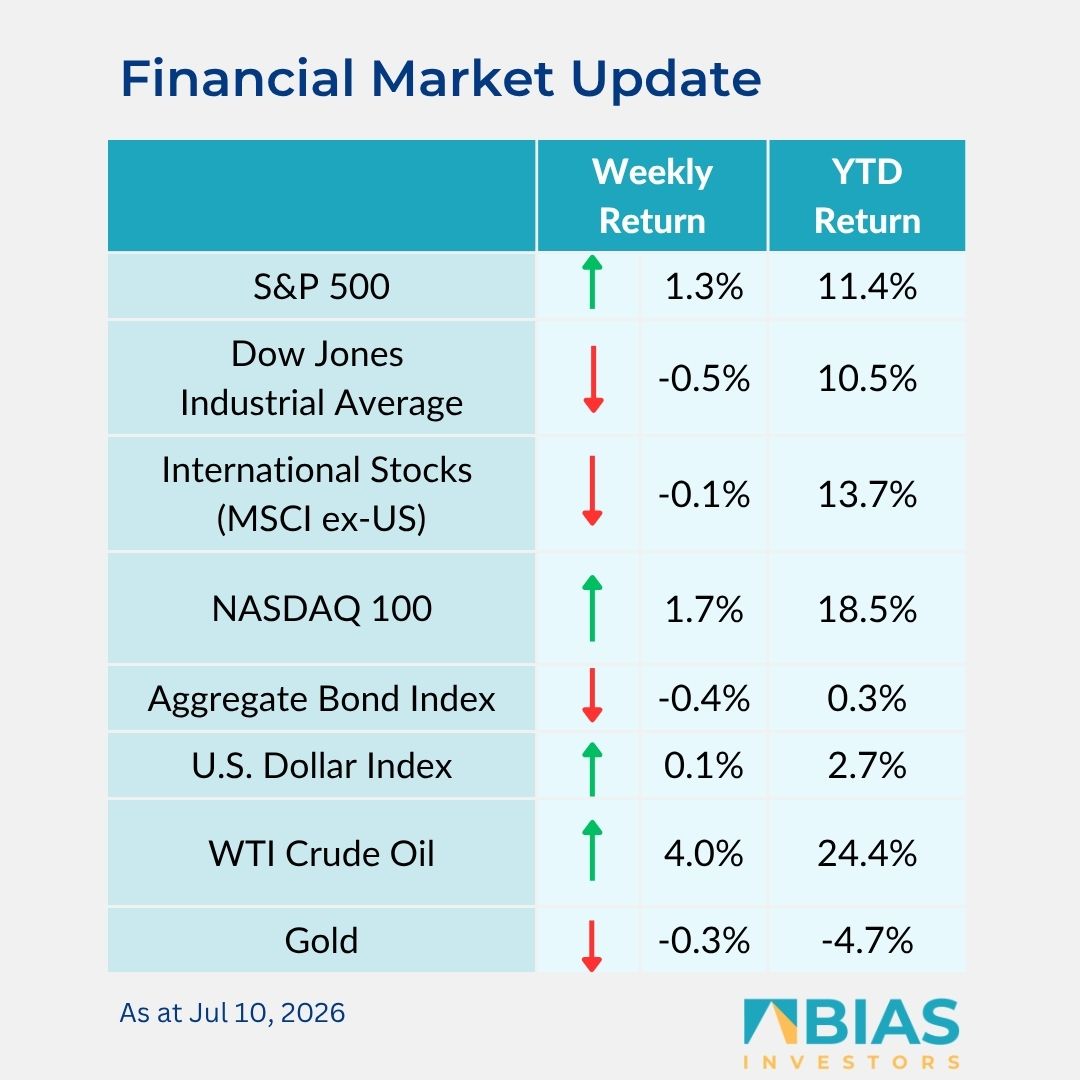

Equity markets were mixed last week with the S&P 500 Index and NASDAQ higher and the Dow Jones lower.

For the week, the S&P 500 Index was +1.3%, the Dow Jones Industrials -0.5%, and the NASDAQ +1.7%.

The technology, energy, and communication services sectors led the S&P 500 Index for the week, while the materials, healthcare, and consumer staples sectors lagged.

The 10-year US Treasury note yield was 4.563% at Friday’s close versus 4.471% the previous week.

The minutes of the June Federal Open Market Committee (FOMC) meeting indicated that inflation was the main point of discussion for policy decisions.

If inflation cools, rates could eventually remain steady or move lower. If inflation remains persistent, additional rate increases could become appropriate.

The FOMC also sees an economy with strong growth, productivity gains, healthy business investment, a stable labour market, and unemployment relatively low.

CME Fed funds futures currently show a single 0.25% interest rate increase at the September meeting, in line with the recent policy projection from the FOMC.

We will get data on June inflation with the Consumer Price Index scheduled for Tuesday, and Producer Price Index for Wednesday. We will also see data on June retail sales and regional economic insights from the Fed Beige Book.

We return to a focus on fundamentals this week as the main part of the second-quarter earnings reporting season begins with 31 companies in the S&P 500 Index scheduled to report earnings.

Second-quarter earnings are expected to grow by 23.6% and quarterly revenue growth is expected at 12.3%. Full-year 2026 earnings are expected to grow by 24.2% with revenue growth of 10.7%.

In our ‘Dissecting headlines’ section, we look at sector level earnings expectations for the second-quarter reporting period.

Dissecting headlines: Second quarter earnings

For the second quarter of 2026, S&P 500 Index earnings growth is currently forecast at +23.6%.

Data from FactSet shows 10 of the 11 sectors are forecast to show year-over-year earnings growth. The energy sector is expected to have the highest year-over-year growth at +122.9%, followed by the technology sector at +63.3%, and the materials sector at +35.3%.

Rounding out the growing sectors are utilities at +13.4%, industrials at +10%, communication services at +7.2%, consumer discretionary at +6.7%, financials at +6.6%, consumer staples at +5.2%, and real estate at +5.1%.

The only sector expected to show a decline in year-over-year earnings is the healthcare sector at -9%.

Second-quarter revenue growth for the S&P 500 Index is currently forecast at +12.3%. The highest revenue growth is expected in the technology sector at +34.2%, followed by energy at +27%, communication services at +13.7%, and financials at +9.5%.

All 11 sectors are forecast to show year-over-year revenue growth. The remaining seven sectors are real estate at +9.2%, utilities at +8.3%, consumer staples at +7.7%, industrials at +7.6%, consumer discretionary at +7.5%, materials at +7%, and healthcare at +4.5%.

Key themes are likely to be capital spending on AI and anticipated return on that spending, the health of the consumer, bank loan growth and credit quality, and the impact of higher energy prices.

The forward 12-month Price-to-Earnings (P/E) ratio for the S&P 500 is 20.5x. This is above the five-year average of 19.9x, and the10-year average of 19.0x. Quarterly results and second-half outlooks will be essential to equity performance.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos