The enactment of tariffs on countries that have not yet reached a trade deal and a weaker employment report for July sent stocks lower.

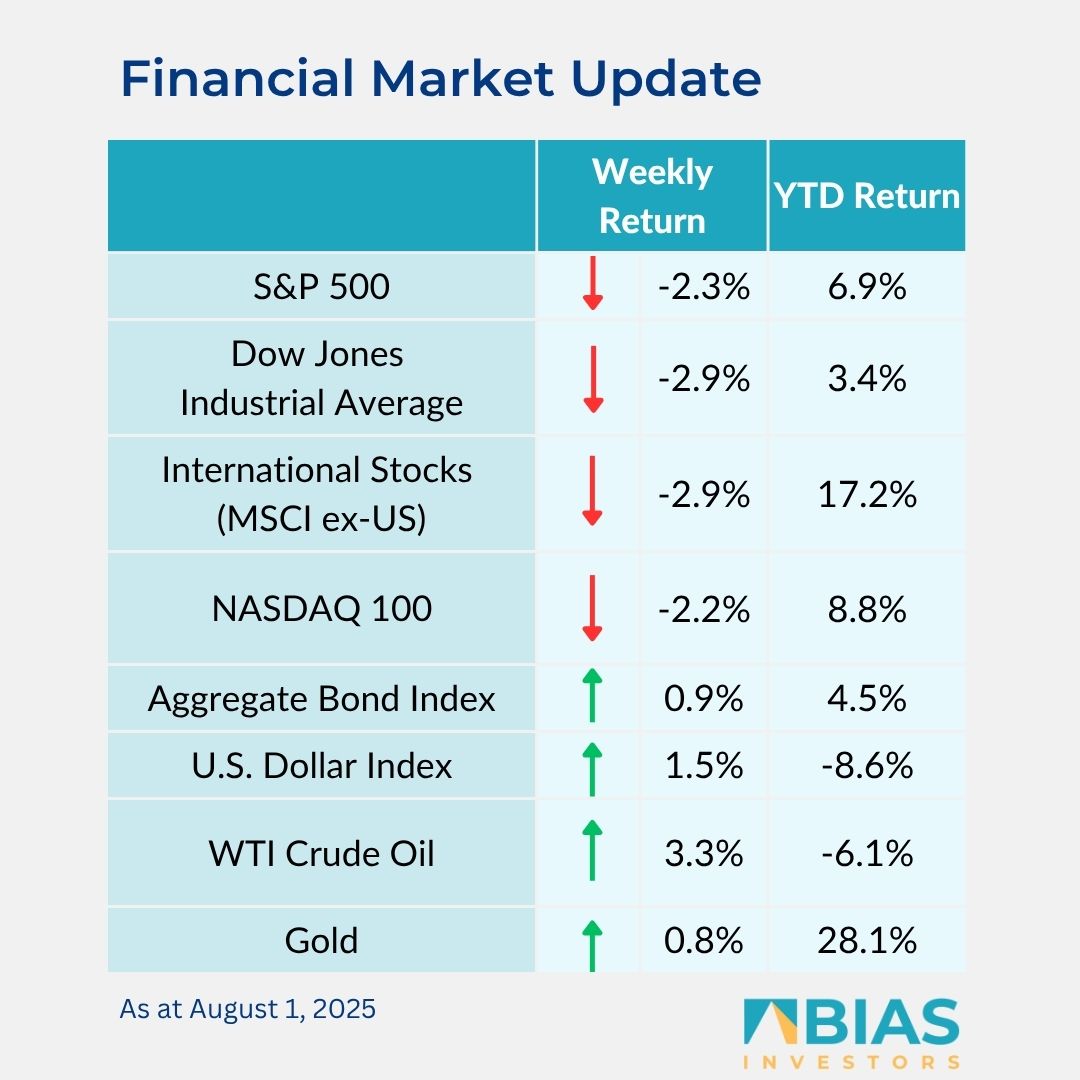

For the week, the S&P 500 Index was -2.3%, the Dow Jones Industrials -2.9%, and the NASDAQ -2.2%. The utility, communication services, and consumer staples sectors led the S&P 500 Index for the week, while the materials, consumer discretionary, and healthcare sectors lagged.

The 10-year US Treasury note yield decreased to 4.214% at Friday’s close versus 4.383% the previous week.

New tariffs went into effect 1 Aug. for countries that had not reached a trade deal with the United States. Mexico secured a 90-day extension, but other major trading partners to include Canada, India and Brazil have yet to reach an agreement. China’s 90-day extension is set to expire on 12 Aug.

The July Employment Situation report showed 73,000 net new jobs created versus an expectation of 110,000. The July unemployment rate rose to 4.2% versus 4.1% in June. June payrolls were revised to +14,000 versus a previous +147,000, and May payrolls were revised to +19,000 versus a previous +144,000. This was a significant revision for the two months.

The Federal Reserve held interest rates steady at its 4.25% to 4.5% target range at its July meeting. Following the weaker employment report, CME Fed funds futures now forecast a total of 0.75% in rate cuts spread across the last three meetings of the year starting in September.

We are heading into the last leg of the second quarter earnings reporting period. This week, 122 companies in the S&P 500 Index are scheduled to report earnings. Of the 66% of companies that have reported so far, 82% have reported upside results versus consensus expectations.

This has increased S&P 500 Index earnings growth expectations for the quarter to 10.3% from 4.8% at the start of the reporting period, and revenue growth to 6% from 4.2%. Full-year 2025 earnings are expected to grow by 9.9% with revenue growth of 5.6%.

In our ‘Dissecting headlines’ section, we take one more look at the trade and tariff landscape.

Dissecting headlines: Trade and tariff update

South Korea signed a trade agreement with the United States ahead of the 1 Aug. deadline. Mexico and the US also agreed to a 90-day extension to continue trade talks.

The South Korean agreement includes a 15% tariff on exports to the US, a $350 billion investment package, and an agreement to purchase $100 billion in energy from the US. The investment package is targeted toward shipbuilding, semiconductors, and other advanced technology.

The Mexico extension comes as they are actively negotiating a long-term trade agreement. China is moving toward the end of its 90-day extension which expires on 12 Aug.

The other major trading partners that have not reached an agreement are seeing their tariffs go higher. Canada will see tariffs rise to 35% from 25% on non-USMCA-compliant goods. India faces a 25% tariff, but is also in ongoing negotiations. Brazil will see tariffs rise to around 50% on most goods and no negotiations with the US are currently under way.

Even though 1 Aug. has passed, tariff negotiation news is likely to last well into the fall.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos