A flare up in US-China trade led to a sharp decline into Friday’s close.

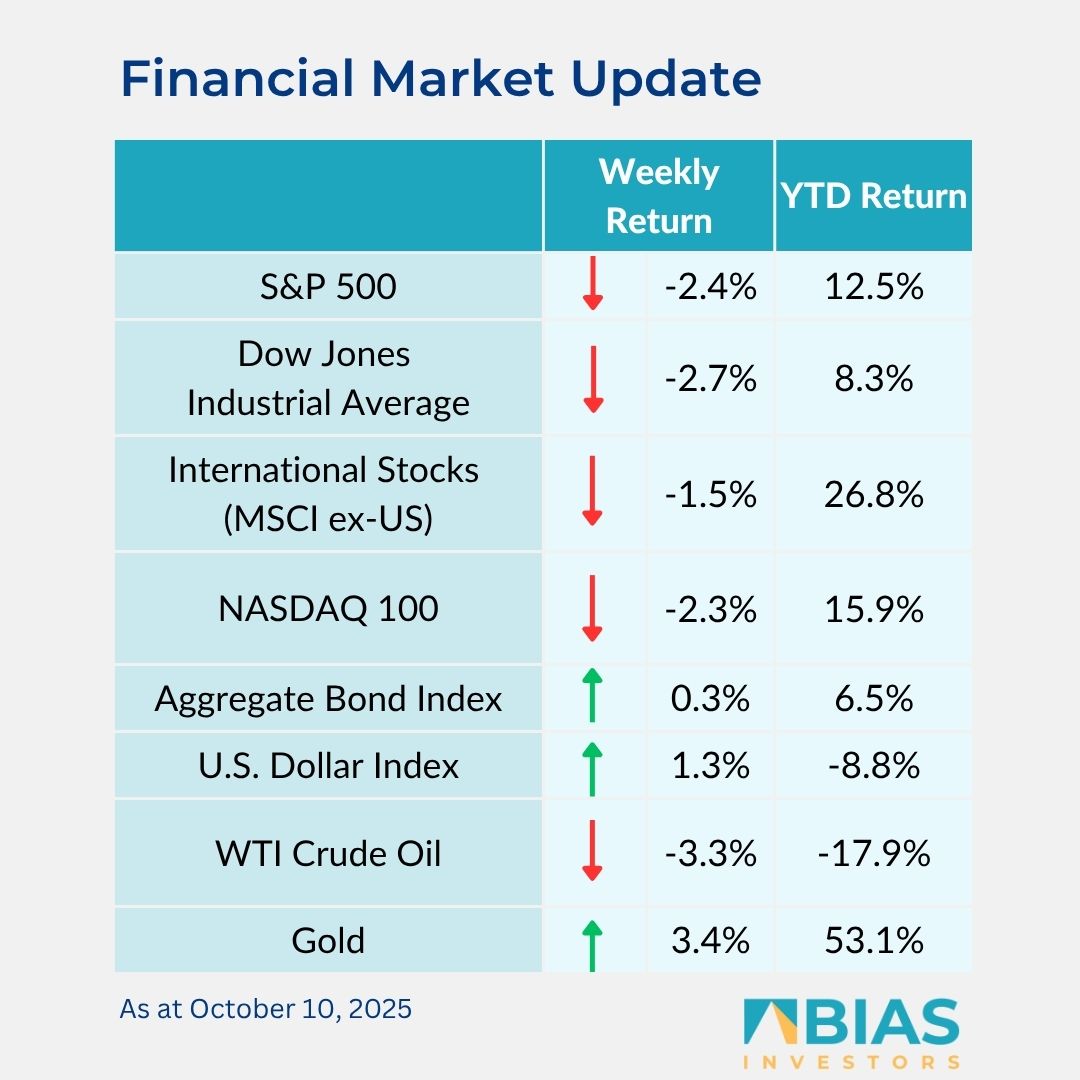

For the week, the S&P 500 Index was -2.4%, the Dow Jones Industrials -2.7%, and the NASDAQ -2.3%. The utility, consumer staples, and healthcare sectors led the S&P 500 Index for the week, while the energy, consumer discretionary, and real estate sectors lagged.

The 10-year US Treasury note yield decreased to 4.055% at Friday’s close versus 4.123% the previous week.

Tensions reemerged in US-China trade following a Chinese tightening of export controls on additional rare earth elements and retaliatory port fees on US ships docking in Chinese ports.

The US responded with President Trump announcing a 100% tariff on Chinese goods to take effect 1 Nov. The situation appears to have been defused over the weekend with President Trump saying, “Don’t worry about China, it will all be fine!”

Trade tensions aside, the US government remains closed. Both parties are likely to resume negotiations and rhetoric this week in search of a solution. Economic data is scarce due to the shutdown, but investors are still expecting a 0.25% rate cut at the 29 Oct. Federal Reserve meeting, and additional cuts in December and March.

The pace of quarterly earnings reports increases this week with 37 companies in the S&P 500 Index scheduled to report results. Third quarter S&P 500 Index earnings growth is forecast at 8%, with revenue growth of 6.3%. Full-year 2025 earnings are expected to grow by 10.9% with revenue growth of 6.1%.

In our ‘Dissecting headlines’ section, we preview the sector level outlook for third quarter earnings.

Dissecting headlines: Third quarter earnings

Beyond headlines of trade flare-ups and government closures, the rubber meets the road for equity investors when quarterly earnings are reported.

The heart of the third quarter earnings season kicks off this week with the large banks and companies in several other sectors.

For the third quarter, S&P 500 Index earnings growth is currently forecast at +8%. Data from FactSet shows seven of the 11 sectors are forecast to show year-over-year earnings growth.

The technology sector is expected to have the highest year-over-year growth at +20.9%, followed by the utility sector at +17.1%, materials at +13.7%, financials at +13.2%, and industrials at +9.8%.

Sectors with positive earnings growth, but below the overall Index level are communication services at +2.8% and real estate at +2.3%. The four sectors expected to show a decline in year-over-year earnings growth are the energy sector at -4.2%, consumer staples at -3.1%, healthcare at -1.7%, and consumer discretionary at -1.7%.

Revenue growth for the S&P 500 Index is currently forecast at +6.3%.

The highest revenue growth is expected in the technology sector at +14.2%, followed by the communication services sector at +8.5%, healthcare at +7.9%, financials at +6.6%, and utility at +6.5%.

Five sectors should see positive growth, but below the overall Index level with real estate at +5.7%, industrials at +4.7%, consumer discretionary at +4.6%, materials at +4%, and consumer staples at +3.4%. Only the energy sector is forecast to see a revenue decline at -1.8%.

The actual earnings results for companies and sectors relative to these expectations, along with their future outlooks, are key determinants of price performance.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos