The Federal Reserve lowered interest rates, the US and China made progress on trade and tariffs, and earnings were generally upbeat from several technology companies.

This all led to higher equity markets.

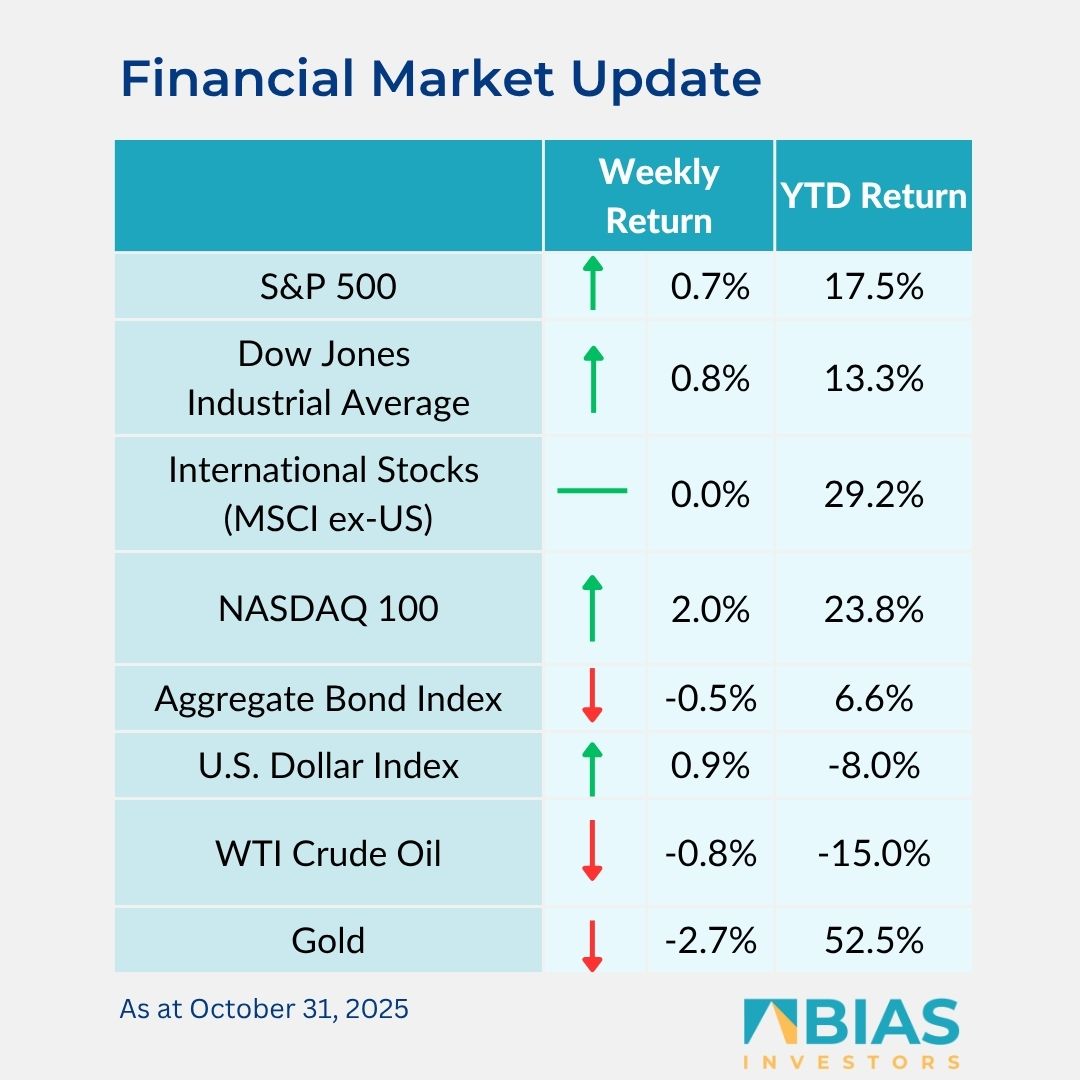

For the week, the S&P 500 Index was +0.7%, the Dow Jones Industrials +0.8, and the NASDAQ +2.0%. The technology, consumer discretionary, and communication services sectors led the S&P 500 Index, while the real estate, materials, and consumer staples sectors lagged.

The 10-year US Treasury note yield increased to 4.093% at Friday’s close versus 3.995% the previous week.

The Federal Reserve lowered the Fed funds rate by 0.25% to a 3.75% to 4% target range. In the post meeting news conference, Fed chairman Jerome Powell commented that an additional 0.25% rate cut at the December meeting is still far from certain, citing lack of data to assess the economy due to the government shutdown.

CME Fed funds futures are projecting the additional 0.25% cut in December, but probability for a cut in the first quarter of 2026 has been pushed out until April.

A meeting between presidents Trump and Xi produced a US–China trade deal lowering US tariffs on Chinese imports to 47% in exchange for China cracking down on fentanyl precursor chemicals.

China also pledged major soybean purchases and agreed to ease export controls on rare earths and magnets for at least one year.

We are past the midpoint of the quarterly earnings reports. This week has 136 companies in the S&P 500 Index scheduled to report results. Third quarter S&P 500 Index earnings growth is forecast at 10.7% with revenue growth of 7.9%.

This is a step-up from the 8% earnings growth and 6.3% revenue growth for the quarter expected at the start of the earnings period last month. Full-year 2025 earnings are expected to grow by 11.2% with revenue growth of 6.6%.

In our ‘Dissecting headlines’ section, we look at specifics on the Federal Reserve policy decision and the US–China trade agreement.

Dissecting headlines: Interest rates and Chine trade

While the Federal Reserve lowered short-term interest rates to a 3.75% to 4% target range last week, Fed chairman Jerome Powell expressed the idea there are still a wide range of outcomes possible for the December meeting and that another 0.25% rate cut is not a sure thing.

While the Fed chairman expressed that he thinks monetary policy is still restrictive to economic growth, the lack of government data creates a level of uncertainty that warrants a slower approach to policy decisions.

He used the analogy that when you are driving in fog, you slow down.

The committee vote to lower interest rates by 0.25% at the October meeting saw two dissentions, but on opposite sides. There was one vote from Kansas City Fed president Jeffrey Schmid to keep rates steady, and one vote from Fed governor Stephen Miran to reduce rates by 0.5%.

Highlights of the US–China trade agreement include China suspending export controls on rare earths, stemming the flow of fentanyl into the US by stopping shipment of precursor chemicals to North America and other parts of the world, and suspending retaliatory tariffs on US goods, mainly agricultural products.

China also agreed to purchase at least 12 million metric tons of US soybeans during the last two months of 2025, and at least 25 million metric tons per year from 2026 to 2028.

China will also resume purchases of US sorghum and hardwood logs.

The US will lower the tariffs on Chinese imports imposed to curb fentanyl flows by removing the 10% penalty tariff, dropping the tariff rate from 57% to 47%.

Both sides commented this was a framework for continued talks, so possibilities for additional actions exist on both sides.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos