New numbers show strongest economic growth since 2007, decreases in inflation

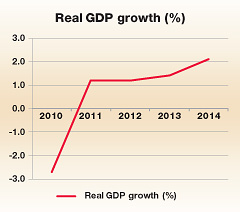

Gross domestic product for the Cayman Islands, a measure of economic growth, increased by 2.1 percent in 2014 to its highest level since before the global economic crisis, according to government figures released this week.

Tourism and related sectors like hotels and restaurants led the growth, increasing by an estimated 10 percent from 2013. Wholesale and retail trade and transport and storage also saw high growth last year. The only two sectors to decline were financial services and government services.

Releasing the new economic report, Finance Minister Marco Archer stated, “I am pleased that we had another year of economic growth for the Cayman Islands in 2014, the highest we have achieved since 2007.”

“With this performance, average income in the Cayman Islands rose to $48,095 in 2014 from $47,170 in 2013,” the minister added.

Economists with the Economic and Statistics Office expect GDP to grow 2.1 percent again in 2015, led by tourism and construction.

Unemployment figures for 2014, released earlier this year, show overall unemployment at 4.7 percent, the lowest level since the start of the recession and down from 6.3 percent in 2013. Unemployment for Caymanians dropped to 7.9 percent, and the rate for non-Caymanians was down to 1.5 percent for the year.

Tourism led the surge in economic activity, with almost two million visitors to the Cayman Islands last year, up almost 16 percent over the year before. Air arrivals were up almost 11 percent and cruise passengers, which last year decreased by almost 9 percent, increased 17 percent in 2014.

The financial services industry had a mixed performance for the year, decreasing overall by 0.2 percent. The report states: “New company and partnership registrations grew while declines were recorded for mutual funds registration, including master funds, insurance licences, stock exchange listing, and banks and trusts.”

Government last year recorded a $93 million surplus, following a $70 million surplus in 2013. Core government debt also fell, down more than $25 million to a recent low of $534 million, or just under 20 percent of overall GDP.

Inflation slows, declines

Inflation, which measures price increases across the economy, was 1.3 percent last year, down from a 2.2 percent inflation rate in 2013.

Another report, released simultaneously with the 2014 economic report, shows the consumer price index, which government uses to measure inflation, dropped into the negative for the first time in almost five years to -0.4 percent for the first quarter of 2015.

Consumer price increases slowed during the fourth quarter of last year, and continued that trend into negative territory in the new year.

Putting the blame squarely on falling oil prices, Minister Archer said in a statement, “This is the first time since September 2010 that the CPI of the Cayman Islands showed a negative movement.”

He added, “It parallels the 0.1 percent CPI decline in the United States during the same period. The general price movements in the two countries reflect the impact of global oil price reductions.”

The consumer price index measurement combines average prices and calculates how households spend their money in Cayman, about two fifths of which go to housing and utilities, which is down about 1 percent for the quarter. Electricity, gas and other fuels decreased by more than 13 percent in the first quarter of this year.

Other decreases so far this year include restaurants and hotels, down more than 8 percent, and miscellaneous goods and services, which decreased by 2.3 percent.

Related Videos

The GDP figures of these Islands; although of vital statistical information to enable future planning; is made quite meaningless due to the amount of businesses who just do not participate. Some of them are fairly substantial economic players; the inclusion of which could show even stronger GDP growth.