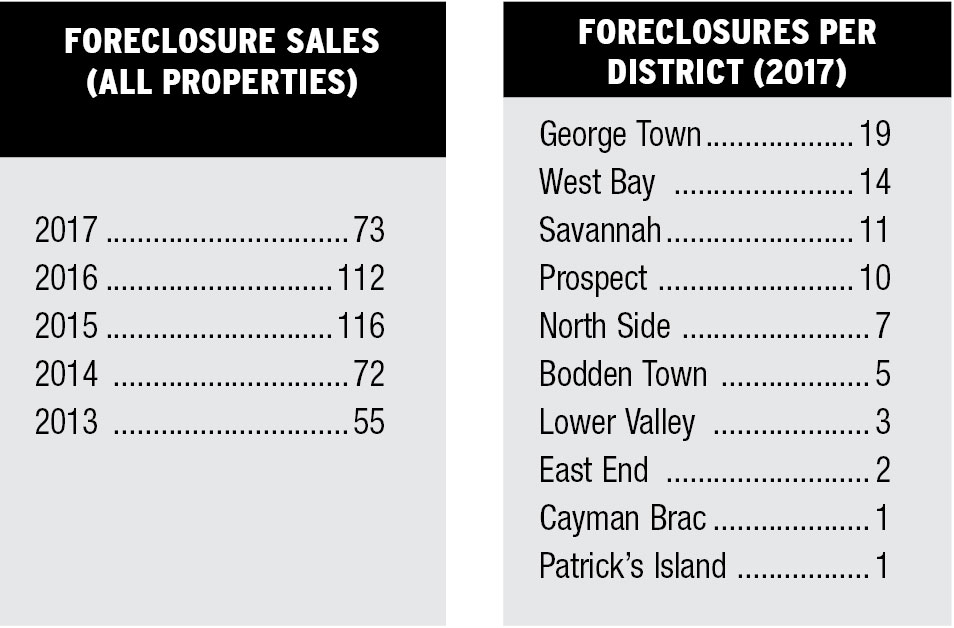

From a $1.4 million South Sound mansion to four two-bed condos that sold for $95,000 each, real estate statistics show 73 foreclosure properties were purchased in 2017.

Homes sold by banks last year spanned all areas of the Cayman Islands and all economic brackets, though the bulk of foreclosure sales involved mid-to-low cost homes in the $100,000 to $200,000 range.

Amid a high level of public commentary and emotion surrounding the issue of foreclosures in the islands, the Cayman Compass analyzed statistics from all 73 foreclosure sales last year.

The headline figure is down substantially compared with 116 properties sold by banks in 2015 and 112 in 2016. Most are homes, though some land lots and one commercial property are included in the 2017 data.

Despite recent high-profile cases putting the political and public spotlight on the issue, new foreclosures have “slowed to a trickle,” according to realtor Kim Lund.

He said many of the properties sold in 2017 had been on the market for some time and the foreclosure sales should continue to decrease in the coming years.

Sales details from the Cayman Islands Real Estate Brokers Association’s multi-listing system, analyzed by the Compass, shows the issue impacting all parts of the island.

George Town saw the most foreclosure sales in 2017, with 19. There were 14 in West Bay, 11 in Savannah and 10 in Prospect, seven in North Side and five in Bodden Town.

Despite perceptions that foreclosed homes are sold quickly and cheaply by banks, the data suggests that many of the properties had been for sale for significant periods of time.

As many as 30 properties had been on the market for more than a year. One had been listed for nearly four years and the median length of time between listing and sale was 293 days. The average amount of time a property valued at under $1 million is on the market before sale is one to three months, according to Mr. Lund.

In the majority of cases, banks sold properties slightly lower than the original list price; $18,000 was the median difference, representing an 11 percent discount in most cases.

There were some significant outliers, however. A five-bed family home in Patrick’s Island, originally listed for $768,000, eventually sold for $480,000. Four condos in Scholars Retreat, West Bay, listed between $139,000 and $200,000, sold for $95,000.

Mr. Lund said, in some cases, the price reduced steadily after time on the market. In other cases, he said, the original price was simply unrealistic.

The issue, perhaps unsurprisingly, has most greatly impacted lower and middle income homes. The majority of the sales, 26, were in the $100,000 to $200,000 bracket. There were 15 in the $200,000 to $300,000 bracket, and only one above $500,000.

“It is mostly impacting properties at the middle and lower end,” says Mr. Lund.

“There is no question that it does affect all sectors but usually those that can afford property at the higher end have the money or other resources they can draw on to avoid foreclosure.”

He said banks were typically very cautious to ensure they got fair market value for properties, with the statistics suggesting that they are often prepared to wait for a decent offer, sometimes for several years.

No one from the Cayman Islands Bankers Association responded to requests for comment for this article.

Justice Richard Williams, delivering his judgment in a foreclosure case last week, outlined the responsibilities of banks in such cases.

He said banks could and should work with homeowners where possible but warned they had a legal right to repossess the property if repayments were consistently not met.

When it comes to selling the home, he said, banks are required to sell in “good faith” and act as a “reasonable man” would in respect of his own property.

He was speaking as he delivered his judgment in the case of Gregory Watt.

A court heard last week that although Mr. Watt had invested $66,000 into the Savannah property, he had been behind on his mortgage repayments for more than four years and had failed to honor numerous arrangements agreed with the bank to catch up.

He was ordered to hand over the keys to his Savannah home by Friday last week.

Mr. Watt’s case, held in public at his request, provided a rare glimpse of how banks deal with foreclosure issues. Such proceedings are typically held in private and no data are publicly available on the level of default in most foreclosure cases.

Related Videos

I wonder if the Banks see the mistakes and bad loans they are making ? According to the statistics for the article looks like Banks are loaning to some people who are trying to start life but hanging their hats too high and the Banks just allow them to . The problem is not with buyers in the upper class loans .

I think that the Banks and the Government needs to look at the foreclosure problems and figure out how they can fix it . Because I don’t think that the Real estate market would be really pretty full of foreclosure homes in a growing Economy and the Banks would soon be out of business making a lost on every foreclosure home/property.