Emil Kalinowski

‘Money’ is being crossed out. Not lost. Not wasted. Crossed out.

The authors are aware that such words will offend the reader as absurd. True, the reader may grant that normal ‘billfold money’ does have a tiresome habit of departing too quickly. But it is certainly not dematerialising.

And yet this month marks year 12 of an astonishing, monetary phenomenon. One that has occurred just three times in the last 150 years: a global depression in money. This is a rare socioeconomic illness, one that weakens the financial and economic realms and, when it persists long enough, debases the social and political domains as well.

The plausibility of your author’s contention rests first upon you, the reader, appreciating the strangely broad continuum of money itself. In that sense money is much like light. Everyday experience is confined to a narrow band defined as ‘visible light’. But the true breadth of the spectrum – practically all of it invisible to the human eye – encompasses a universe of different wavelengths; from radio waves to gamma rays, from near ultraviolet to far infrared. Humanity’s monetary spectrum, unconstrained by the laws of physics is even broader than nature’s electromagnetic rainbow.

Wavelength and energy

In terms of breadth, there are numerous currencies. The United Nations lists 151 currencies; different ‘wavelengths’ if you will. In terms of depth, there are numerous formats; ‘energy’ if the authors were to push the analogy beyond the literary pale. It is here that the multifariousness of money is revealed.

For early societies, the preferred format was an item which was readily available, broadly acceptable and could serve as a medium of exchange. Common monetary formats included cereal, cattle and cowrie. As civilisation advanced so did monetary composition with the invention first of coin and then cash. The evolution continues to the present day with the introduction of cryptocurrencies, perhaps the most ethereal format to date.

Not that familiarity with computer science is a prerequisite to appreciate the depth of modern ‘money’. Just consider subway tokens, frequent flyer miles, grocery store coupons, massively multiplayer online role-playing manna. And the classics remain in style too; mints continue to produce gold and silver coins in America, Australia, Austria, Britain, Canada, China and South Africa.

But the format that is of overwhelming importance, the one that is filled with the most latent energy, the one that serves as the foundation for global capital markets and economic activity is credit and collateral. This is this money that is being crossed out.

Bookkeeper’s pen

Credit and collateral are the realm of the financial institution. Though central banks and national treasuries have a monopoly on notes and coins, it is the depository, commercial and investment banks that govern credit and collateral. Instead of minting nickels or printing hundreds, these institutions extend their balance sheets to farmers, manufacturers, wholesalers, retailers, explorers, researchers, insurers, pensions, investors and governments. They ‘mint’ bespoke financial products. They ‘print’ interest rate swaps, Eurodollar futures, foreign exchange forwards, and other esoteric sounding money. And they do it on a global scale.

Their proliferation of ’money’ was the great flood of liquidity that swept the post-cold war globalisation across national boundaries. The capital flows reduced transactional frictions and rounded off harsh social edges that might have been obstacles to the ever-expanding cross-border movement of people, goods and capital. But tides cannot flood indefinitely, they must ebb.

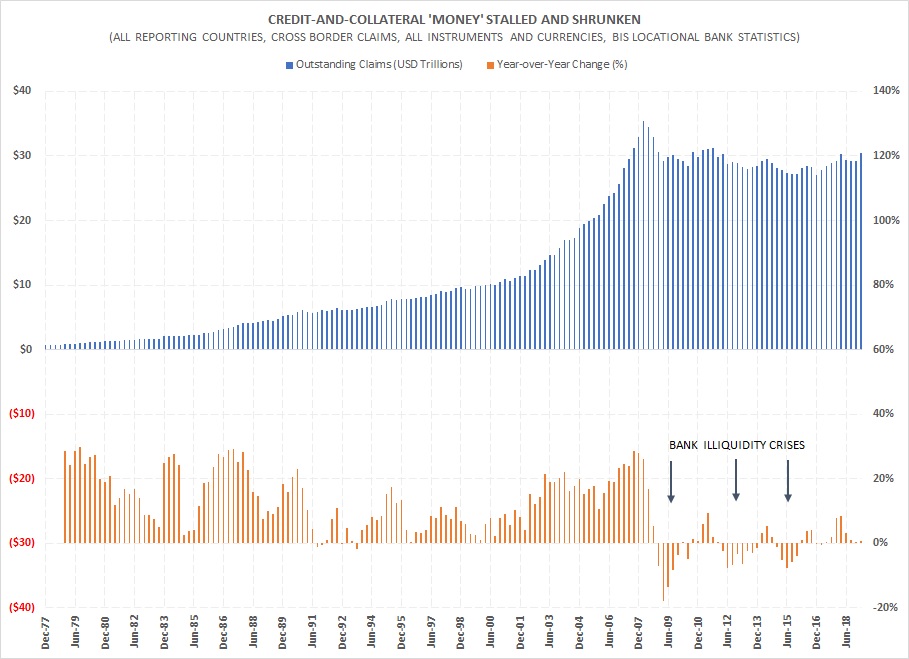

The first illiquidity crisis struck in 2007‑08. For most observers that period was about the American real estate market. But for financial institutions this was an episode in which large segments of credit and collateral were ‘demonetised’. An alphabet soup of monetary formats (e.g., MBS, CDS, CLO) were suddenly no longer money-good.

But as upsetting as 2007‑08 was, financial institutions were more disturbed by the fact that a once-in-four-generations global monetary shock occurred again. By 2011‑12, another monetary composition – sovereign debt of European countries on the Mediterranean – was being rejected.

Then it happened again. This time, from 2014 to 2016, the bank crisis did not centre on format, instead the epicentre was a collection of emerging market currencies, China most prominently.

As one type of ‘money’ after another was invalidated or discounted, non-state banks retreated – from each other, from engaging economic actors and from globalisation. Their decision to withdraw resulted in the contraction of the collective private banking balance sheet. Credit and collateral were being crossed out by the bookkeeper’s pen.

In response, central banks have both enticed and threatened their private cousins to get back to business. But these financial institutions have by now been burned thrice; for them risk far outweighs reward.

To quantify their risk perceptions, consider that in the dozen years since the first bout of illiquidity struck, the Federal Deposit Insurance Corporation (FDIC) has identified 544 bank failures in the United States. Over the same time period leading up to August 2007, the FDIC had identified only 48.

From 1934 through 2007, the total assets of commercial banks in the US (and its territories) compounded at an annual growth rate of 7.8% per year. But from 2007 to 2017 (the latest available data) the rate is 3.8%, less than half of the three-quarter-of-a-century baseline. Those few percent may not sound like a large difference but it works out to $7.5 trillion US dollars in missing bank activity. It makes the US banking system approximately one-third smaller than it should be.

The American example can be generalised globally. According to the Bank for International Settlements the total cross-border claims of banks (i.e., private bank money-creation activity) grew 3.3% over the past dozen years, in total. In the dozen years leading up to 2007/2008 that growth rate was compounding at 11.4% per year.

Which brings our story to present day: During 2018, various monetary and financial markets signalled that a fourth bank illiquidity disturbance was coalescing. More than halfway through this year, precious few economic accounts suggest anything other than gathering momentum of an approaching squall. As central banks race to accommodate conditions by lowering short-term interest rates, the private banking system continues its retreat; their bookkeepers, out of self-preservation, crossing out ‘money’.

Emil Kalinowski, CFA, is a member of the CFA Society Cayman Islands board.

Related Videos