For much of the past decade, hedge funds on average have been plagued by poor performance relative to soaring equity benchmarks, as unprecedented accommodative monetary policy globally boosted the stock markets.

It is no surprise that in a sustained bull market, the average fund manager or the average of all hedge fund strategies is likely to underperform a largely one-directional market. Given that many hedge funds invest into the same stocks as mutual funds or individual investors, superior returns must come from either selecting a more-talented fund manager or choosing a timely strategy.

Hedge funds were always meant to come into their own when market volatility increases.

In February’s market turmoil, the downside protection afforded by hedged strategies compared to long-only portfolios enabled hedge fund managers to post the strongest monthly outperformance over global equities since 2009, data provider Eurekahedge reported.

The Eurekahedge Hedge Fund Index, a proxy for the average hedge fund, was down 1.63% in February, outperforming global equity market indices like the MSCI ACWI (IMI), which lost 7.82% over the same period.

More than 90% of the hedge funds outperformed the global stock markets during the month. About one-third of funds (34.7%) generated positive returns and 43.2% of funds in the Eurekahedge database were up for the first two months of 2020.

Although February started reasonably well for the markets based on a slowing number of COVID-19 infections in China and stimulus packages announced by central banks, the second half of the month saw a shift in market sentiment.

Investors concerned about the extent of the outbreak outside China, particularly in Italy and South Korea, prompted a massive sell-off of global equities.

During the week ending 28 Feb., the US Dow Jones and S&P500 indices lost 12.36% and 11.49%, respectively, while the French CAC40 was down 8.55% and Germany’s DAX lost 8.41%.

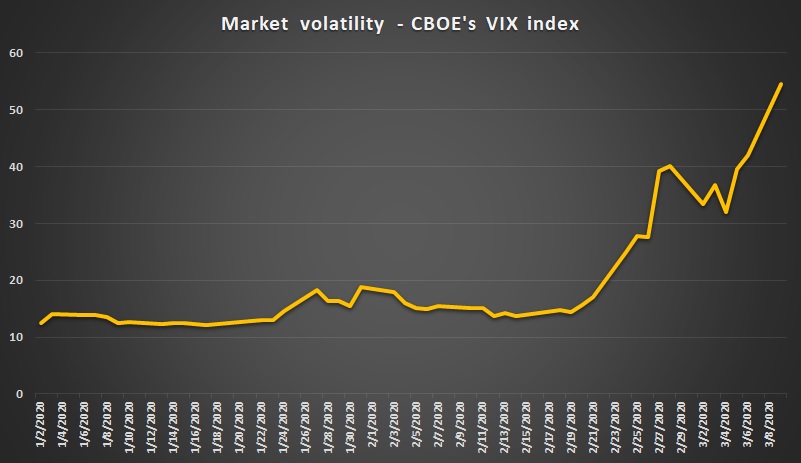

The Chicago Board Options Exchange’s VIX index, also known as the ‘fear index’, which measures the stock market’s volatility expectations based on the S&P500 index, jumped from 17 to 52 during the last week of February and spiked briefly above 60 on Monday this week – levels not seen since the 2008 financial crisis.

Funds that bet on volatility gained more than most other asset classes, including gold, during recent weeks. Managers betting on lower interest rates and rising prices for bonds, in anticipation of further monetary easing by central banks, have also seen above-average returns.

Many other funds made money shorting stocks that are heavily affected by the coronavirus outbreak, including airlines, cruise lines, entertainment companies and the oil business.

Certain multi-strategy funds, which spread risk across several asset classes to protect against volatility, performed well, whereas funds holding equities were hit harder.

On Tuesday, global markets stabilised, staying mostly flat, after the S&P500 had closed down 7.6% and the FTSE lost 7.7% on Monday in the biggest one-day fall since the last financial crisis.

Crude oil saw a 6% rebound, despite Saudi Arabia’s move to increase oil production and cut prices, which sent the price of oil down by as much as 30% the day before.

Related Videos