Crises have been the defining feature of the past two decades. First Hurricane Ivan in 2004, then the global financial crisis of 2008 and now the coronavirus pandemic are probing the resilience of the Islands in such short intervals that new challenges are emerging when the effects of previous disruptions have barely faded.

In many ways Cayman’s regular exposure to tropical hurricanes has shaped a mindset in recent years that takes disaster recovery and business continuity much more seriously.

But how useful is this preparedness and anything Cayman has learnt in this new crisis that seems to be so different from what we have faced in the past? And what can the experiences of 2004 and 2008 tell us about what comes next?

Hurricane Ivan 2004

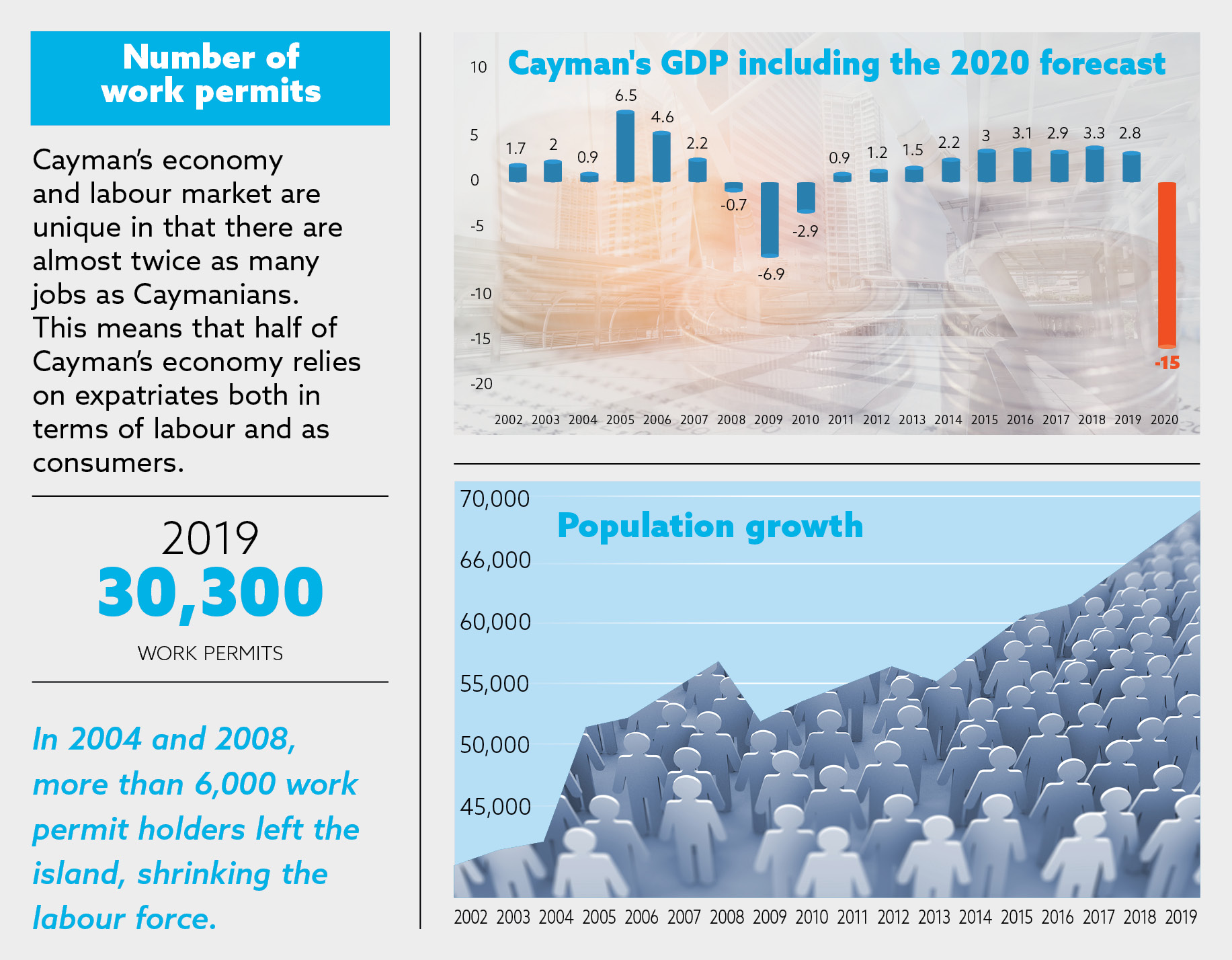

Looking back at the total economic impact of Hurricane Ivan, which passed Cayman on 11 and 12 Sept. 2004, the numbers are staggering. The United Nations Economic Commission for Latin America and the Caribbean estimated an economic cost of CI$3.4 billion, almost double the amount (183%) of Cayman’s annual economic output at the time. More than 13,500 residential properties were damaged at a cost of $1.4 billion. The physical damage to the islands, including commercial and public infrastructure, amounted to $2.4 billion. Prices rocketed and annual inflation increased to 11.1% in March 2005.

The disaster also showed a pattern that would be repeated in the financial crisis and most likely today.

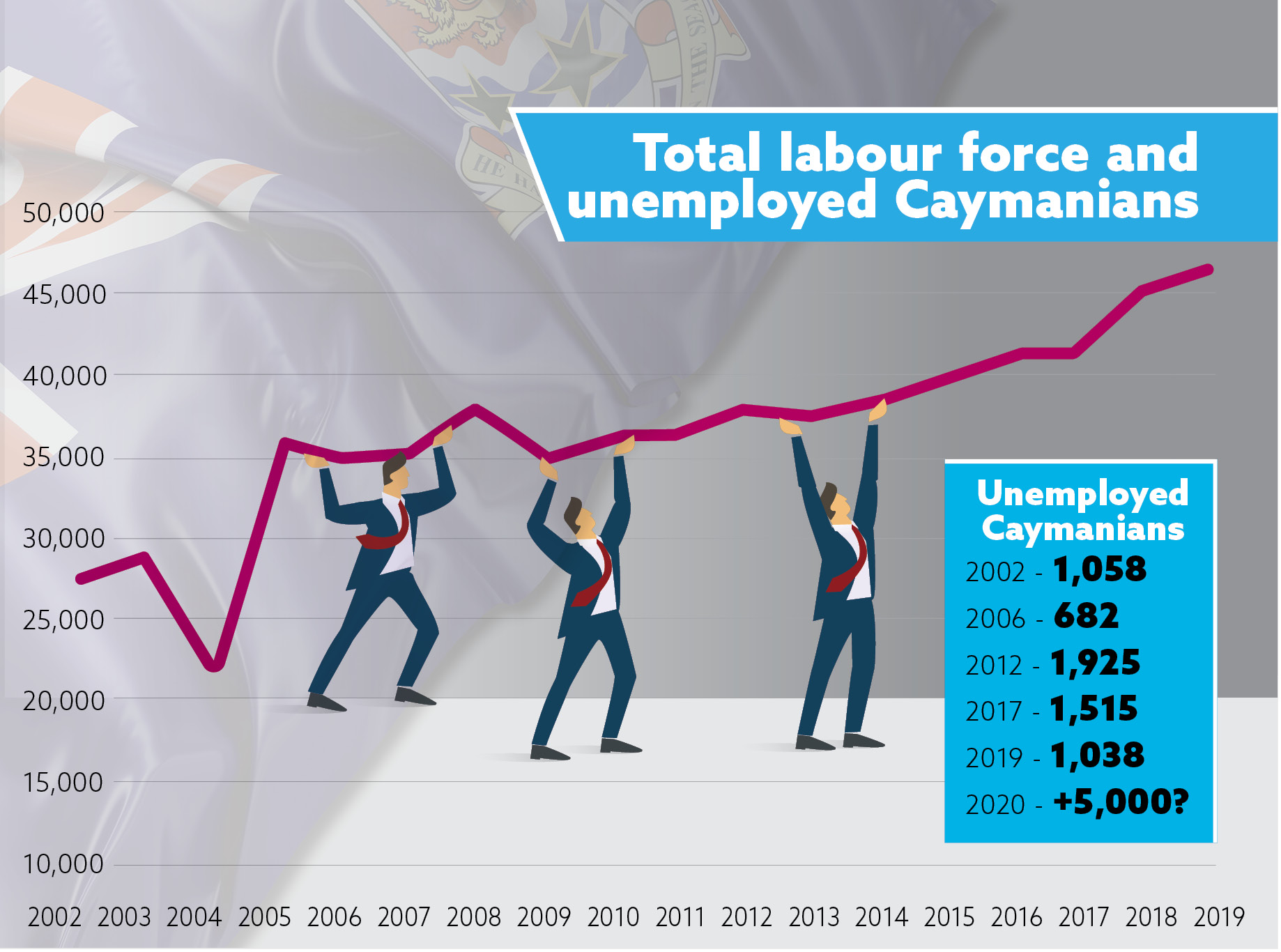

Cayman’s labour force declined rapidly, dropping by more than 21% or 6,500 workers, as out-of-work expats on work permits left the island. At the same time, the conditions were vastly different from what they are now.

Insurance was widespread and covered much, albeit not all, of the private sector and government infrastructure damage. Claim pay-outs accelerated a massive reconstruction effort, which in the space of 12 months, returned the labour force to a higher level than before Hurricane Ivan.

Although the impact of the hurricane damage on the finance and tourism sectors was estimated at CI$460 million each, Cayman’s economy still grew by 0.9% in 2004. A year later the reconstruction sparked a 6.5% jump in GDP growth.

The lack of a prolonged recession meant that the unemployment rate barely moved and stayed significantly below its previous high of 7.5% in 2001.

“Looking back, it’s interesting that, what must have been a similar devastation in our tourism sector, didn’t create a lot of unemployment,” said Steve McIntosh, head of recruitment firm CML.

The government at the time made a brave political choice to be more flexible with companies, and allow hiring from overseas, which facilitated the recovery, he added.

The timing of the crisis also helped. The financial services sector in Cayman started to take off in the early 2000s, especially in hedge fund audit and administration.

“Those two factors allowed Cayman to bounce back quickly,” McIntosh said.

Global financial crisis

The global financial crisis that began in 2008 could not have been more different. Rather than sweep across the islands like a hurricane, followed by a quick rebuilding effort, it lingered and gradually led to structural weaknesses in the economy that took years to overcome.

“As asset values tumbled, and revenues and investment fell, financial services firms bifurcated into those that needed to be in Cayman, and those that didn’t. Many of those that didn’t need to be in Cayman began to downsize and leave,” McIntosh said. “This contraction was compounded by more restrictive immigration policies combined with higher fees.”

While other jurisdictions were assiduously courting mobile financial services firms, Cayman was increasing both fees and bureaucracy. “This was a toxic combination, as well as a vicious cycle which lasted for a number of years until the global economy began to take off again,” he said.

Although it was deemed a financial crisis, the economic weakness of Cayman’s main source market, the US, also affected tourism and many other related industries.

Cayman’s labour market reacted in a predictable way. More than 6,000 unemployed work-permit holders left the island, again shrinking the labour force.

Unlike post-Ivan, however, there was no immediate turnaround. Fewer expats on work permits actually led to fewer jobs for Caymanians, with unemployment increasing from 6.6% in 2008 to 10.5% in 2012.

The economy contracted for three consecutive years, by 0.7%, 6.9% and 2.9% between 2008 and 2010.

The recession was worsened by a population decline. It took six years, until 2014, to exceed the 57,000 level of 2008. The number of work-permit holders, which had reached more than 26,000 when the financial crisis began, dropped for years to about 19,000 in 2013.

It only returned to pre-crisis levels in 2018, a full 10 years later.

McIntosh says for him the lessons from this period have nothing to do with immigration policy, but the ever-present importance to speak to firms and understand their challenges and needs.

With the recently created Ministry of Trade and Investment, Cayman is in a better position than in the past, he said. “With the right strategy and resources, this ministry will serve a vital role in our recovery from the COVID-19 crisis.”

Declining prices were one of the few positives that helped alleviate the downturn in the year following 2008. Paul Byles, director of consulting firm FTS, says we should again expect falling prices this year. This is driven partly by the significant drop in fuel prices and the anticipated over-supply of housing, which should lead to cheaper rental rates for some residents.

The continued commitment of the Dart Group to projects like Camana Bay and other ventures throughout the financial crisis was another major factor for local economic recovery.

Byles said it is encouraging that some investors such as the Dart Group have indicated they will once again continue to invest. “That will at least minimise the fallout for jobs,” he said.

In contrast to the challenges 12 years ago, the public sector is also in a much-better position and financially prepared to keep more people employed, Byles added.

The pandemic economy

In contrast to previous challenges, the coronavirus pandemic has shut down most parts of the domestic economy. Its sudden impact is reminiscent of a natural catastrophe. Yet it will endure much longer and involve much more uncertainty. Premier Alden McLaughlin likened it to a hurricane that lasts several months.

Any speculation about the length of the current crisis will need to consider that this is not just a downturn like any other. In previous recessions, the objective was to shorten the economic downturn by stimulating demand. In the pandemic economy, demand is actively suppressed with economic transactions reduced by asking businesses to close, and consumers and workers to stay at home in the interest of public health.

The effect has been faster and more widespread across industrial sectors than in any other recession.

For the first time, personal services as well as retail, transport and tourism, and not goods-producing industries, are leading the downturn. Because of the large numbers of personal service workers, such as hospitality staff, barbers, taxi drivers and anyone else interacting one-on-one with customers, the effect may be bigger and more rapid. These workers are often paid less, and their sectors are also less able to withstand economic shocks than other parts of the economy.

Some believe that most economies were intact before the lockdown. They argue that there are no structural weaknesses, as for example in the financial system in the run-up to 2008.

In the words of World Trade Organization director-general Roberto Azevedo, the pandemic has simply cut the fuel line to the engine. If only the fuel line were reconnected properly, a rapid rebound would be possible.

The counterargument to that view concedes that the financial system may be more resilient but claims that the global economy operates with few buffers.

If the first weeks of the crisis have shown anything, it is that many businesses and the self-employed operate on extremely thin margins, with little reserves and barely any room for error.

In Cayman this comes after what many would consider economic boom years. Globally, however, the economic picture was characterised by years of slow growth that never returned to pre-2008 levels.

It is also the first time that the pace of economic recovery will be dictated first and foremost by public health concerns. This increases the uncertainty and, together with the knock-on effects of lockdown measures reverberating through most sectors of the economy, makes a fast recovery, as in 2004, less likely.

Byles said, “No one knows when the current crisis will end but I believe that 12 months after COVID-19, our recovery will be tougher this time around, because there is no natural boost to domestic economic activity to help us rebound.”

The construction and real estate activity will resume but more slowly due to the changing financial circumstances and priorities of investors, he added. “The business case for some of the apartments that were being built may be weaker if we lose too many residents, so some of those projects may be placed on hold.”

Cayman’s unique economy

Cayman’s economy and labour market are unique in that there are almost twice as many jobs as Caymanians. This means that half of Cayman’s economy relies on expatriates both in terms of labour and as consumers.

The immediate effect of any recession is that the importation of labour is reversed. For Cayman’s government, the foreign unemployed become a problem that their home countries will have to deal with. In addition, it artificially reduces the unemployment rate locally.

“This certainly provides something of a cushion in terms of the unemployment rate and the fiscal burden from the increasing demand on welfare,” said McIntosh. “But it will be cold comfort to thousands of unemployed Caymanians that thousands of expats also became unemployed and had to leave the country.”

Losing foreign workers as consumers will lead to a consolidation of the businesses that provide goods and services to residents.

While these same principles will apply as in previous crises, the projections for the initial impact of the COVID-19 crisis are much more extreme than what Cayman experienced in the past.

A report commissioned by the Chamber of Commerce concluded that a two-month lockdown would lead to a 15% decline of GDP in 2020. This is led by a drop in tourism (-54%) and construction activity (-30%). Services such as wholesale and retail trade, ICT, utilities, transport and real estate would in combination fall by 19%.

“This will be a tough time for those companies because if revenue goes down by 20% across the board, that doesn’t mean 20% of companies go out of business and everyone else makes the same profit as before. It means no one in the entire sector makes any money,” McIntosh said.

Under a four-month lockdown, the economy could contract by as much as 22% this year, the report noted.

Unemployment estimates for 2020 are also much higher than the figures recorded after Hurricane Ivan or in the years following the financial crisis.

The tourism and constructions sectors alone are expected to shed more than 4,000 and 2,000 jobs, respectively. In total, more than 5,600 Caymanians and more than 5,000 non-Caymanians could lose their jobs in 2020, according to the Chamber report, which assessed the short- to medium-term impact of the COVID-19 pandemic.

To put these figures in perspective, even in 2012, when Caymanian unemployment reached its high of 10.5%, fewer than 2,000 Caymanians were unemployed.

“The only solution to this negative domino effect is to minimise the current economic fallout as much as we can. That is easier said than done but it is the only realistic strategy we have based on the nature of our economy,” said Byles, the author of the Chamber report. “Essentially if we can find a way to ‘hang in there’ to limit the jobs collapse we will have more than a fighting chance to recover. We can only do this safely and as determined by the government.”

However, he said, “I am optimistic about us recovering because the government’s early actions have put us in a position where we can now look at strategies to achieve the delicate balance needed.”

Can financial services save the economy?

Projections for the financial services industry provide one of the few bright spots of the forecasts but they still anticipate a 7% decline of the sector.

According to Cayman Finance CEO Jude Scott, “Most firms in Cayman’s financial services industry have fully embraced technology and leveraged it to their advantage, allowing them to provide ongoing seamless service to clients even during this challenging global crisis.”

He noted that through the implementation of business continuity plans the industry can be sustained indefinitely, if necessary. “That enables the Cayman Islands to ensure the health and safety of our people continues to be the highest priority, while at the same time continuing to deliver critical ongoing financial services at the highest levels to countries and clients around the world,” Scott said.

The additional knowledge and experience gained during Hurricane Ivan and the global credit crisis, Scott said, has been applied by industry members to the current COVID-19 pandemic, in conjunction with new approaches and the latest technology.

The Cayman Finance CEO said the industry is well positioned and diversified enough to support countries around the world, as they are issuing sovereign debt to provide stimulus to their economies and as they seek to move their economies into the recovery phase.

In this context, Cayman entities would help provide foreign direct investment, infrastructure investments and financing, and diversified investments.

“Now, more than ever, those things are going to become critically important to be channelled through a global tax-neutral financial hub like the Cayman Islands, as capital and investing will need to be deployed by various countries and stakeholders around the world into various countries around the world,” Scott said.

“While much of the focus now is rightly on addressing the wellbeing of people, countries will also start to put attention on having functional economies that survive in the long run. As with the 2008 crisis, access to liquidity is an important part of that equation.”

For CML’s McIntosh the financial services industry will look relatively unscathed compared to tourism, at least in the short term.

“But the macro-economic conditions will hurt financial services firms in the medium term as clients fold up and contract. However, there are so many crosswinds right now with the EU blacklisting, the Private Funds Law and public register of beneficial owners, it may be difficult to tell what impacts were caused by COVID-19,” he said.

Related Videos

The French economy is re-opening slowly from 11 May. It will be mandatory to wear a disposable or washable face mask on public transport etc. Supermarkets will sell them.

https://www.connexionfrance.com/French-news/Covid-19-French-supermarkets-to-sell-masks-for-2-3-euros

We should be doing this.

The loss of income from tourism is heart-breaking. While government employees have continued to enjoy full pay and benefits, even while mostly not working, the private sector has not been given government help and many employers must be close to bankruptcy.

Shipping back expat workers who no longer have a job causes other local problems, ignoring the human cost to these workers. For example they will no longer be paying rent on their mostly Caymanian owned homes nor spending money locally. Nor will work permit fees be collected.

I have suggested before that, if we can get clear of this virus, we should market ourselves as a safe refuge for vulnerable people from overseas.

There must be many New Yorkers, for example, who are currently scared to even walk on their streets who’d be happy to stay here for the next 6 months to a year. While the hotels and rental apartments would have to charge less than the current rates for such long term visitors, it would be a valuable boost to our economy.

Of course everyone would need to be tested before boarding a plane and put in isolation when they arrive.