Several months into the current COVID-19 pandemic, the world has witnessed the effects of unprecedented government and central bank policy responses that have sought to protect lives and support economic growth. Trillions of dollars have been spent to support unemployed workers and credit-constrained businesses, asset markets have been flushed with liquidity, and physical-distancing measures have been instituted to keep society functioning safely albeit with reduced economic throughput and economies of scale.

Several months into the current COVID-19 pandemic, the world has witnessed the effects of unprecedented government and central bank policy responses that have sought to protect lives and support economic growth. Trillions of dollars have been spent to support unemployed workers and credit-constrained businesses, asset markets have been flushed with liquidity, and physical-distancing measures have been instituted to keep society functioning safely albeit with reduced economic throughput and economies of scale.

While the timing of suitable vaccine discovery and deployment is uncertain (the joint Oxford-AstraZeneca vaccine currently shows promise) – and it will take months for vaccines to reach the planet’s billions – the economic consequences of the pandemic are becoming clearer.

In my April Market Watch article, I argued that we would not see a V-shaped economic recovery and that, absent a miracle cure, we would see rolling lockdowns as waves of the virus re-emerged. Since then, US initial jobless claims and unemployment levels continue to remain stubbornly high and the rapid initial rebound in economic growth is now starting to wane. This trend will likely continue as parts of the world once again lock down.

For example, Melbourne, parts of Catalonia in Spain, and parts of Xinjiang in China have recently entered into new lockdowns while US state governors in California and Texas have rolled back measures to reopen society. And where governments have prioritised economics over health safety, businesses and individuals are self-imposing measures to maintain physical distance.

What is becoming clear is that we are not experiencing a V-shaped economic recovery even though we are witnessing a V-shaped market recovery despite numerous risks lurking in the background (e.g., faltering trade relationships with China, uncertainty over Brexit, etc.). While the world awaits vaccine deployment, governments and central banks plan to spend more to support economic growth; the IMF forecasts that global debt-to-GDP will increase by 19 percentage points in 2020 alone. With this continued public spending, investors are asking whether higher inflation will follow.

The answer is probably no in the shorter term and potentially yes in the longer term.

Inflation in the shorter term

Aware of the large bill coming due post-pandemic, governments are beginning to identify ways to more carefully spend money in preparation for future waves of the virus. Meanwhile central banks, taking the lead from the Bank of Japan, are exploring policy options such as yield curve control (i.e., capping longer-term interest rates through episodic rather than regular bond purchases) to help curtail balance-sheet growth.

Mindful of government and central bank budget constraints, consumers are pre-emptively saving as insurance against unemployment expanding beyond the retail, hospitality and tourism sectors. It is not inconceivable that job cuts will expand to more economic sectors as companies combat profit-margin compression, which has resulted from lower spending and rising costs related to supply chain disruptions, physical-distancing measures, and reduced economies of scale. More unemployment could pose new challenges just as economies start to heal.

With lower private sector, and potentially less incremental public sector, spending in the shorter term, price increases should remain subdued over the next few years. Furthermore, new waves of the virus will almost guarantee that more people will stay at home and spend less, forcing producers to discount prices. If people have ventured out this summer while the virus has remained present, the upcoming flu season will certainly give them pause as they face challenges distinguishing between cold symptoms and those of COVID-19. Masks will increasingly become ubiquitous and responses to sneezes could evolve to “bless you…and please bless all of us too!”

Inflation in the longer term

Predicting inflation dynamics in the longer term is tricky due to many moving parts.

From a debt-management perspective, it is unclear what combination of reduced spending, tax increases, debt defaults, and artificially suppressed interest rates below rates of inflation, will keep government debt loads manageable.

With voters potentially staring at some form of wealth destruction in their rear-view mirrors coupled with rising societal pressures to eschew economic inequality, reduced government spending and personal tax increases will not be popular amongst low and middle-income voters. Instead, the world will likely see some combination of higher inflation, debt forgiveness, and higher wealth and corporate taxes to offset rising debt loads.

Thus, absent a boost in productivity growth, which has remained elusive over the last several years, higher inflation may be a palatable solution to reduce public debt.

Higher productivity growth, however, cannot be ruled out. Provided that zombie companies, supported by artificially low borrowing costs, do not lower productivity, increasing cooperation between public- and private-sector organisations along with improved adoption of remote working technology, could finally lead to improved productivity. Rising consumer confidence post pandemic, coupled with higher productivity growth could lead to consumers deploying precautionary savings, leading to significant upward price pressures. Meanwhile, central banks, having undershot inflation targets for years, may be reluctant to hike interest rates despite rising inflation. Thus, higher inflation, with or without higher productivity growth, is likely.

Protecting against inflation and wealth erosion

Investors seeking protection against higher inflation may want to reconfigure their portfolios. With current bond yields extremely low, if not negative, in most developed economies, longer-term bonds no longer offer sufficient protection in multi-asset portfolios and investors may need to explore fixed-income substitutes.

While valuations may be lofty in some areas, residential real-estate investments with high occupancy rates may offer fixed-income like characteristics and protect against higher inflation provided that investors are comfortable with less liquidity (i.e., it is harder to quickly sell real-estate assets than developed world government bonds).

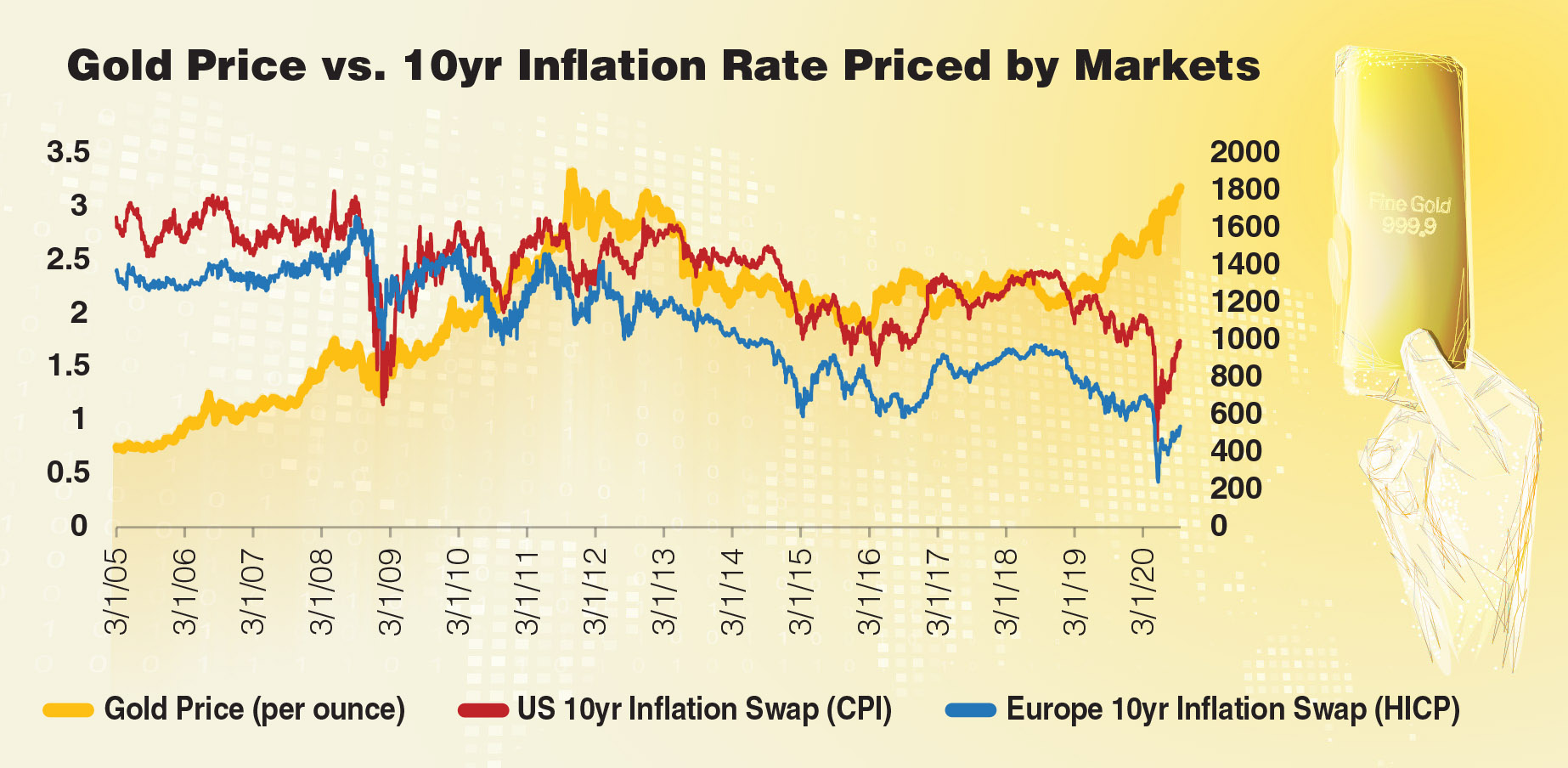

Adding gold to portfolios is another option although, at current levels, a lot of future inflation is already priced in.

Adding gold to portfolios is another option although, at current levels, a lot of future inflation is already priced in.

On the contrary, inflation-linked bonds are not pricing in high future inflation and may be good substitutes for traditional bonds. Unlike traditional bonds, inflation-linked bonds make payments that are tied to inflation indices such as the Consumer Price Index. While gold prices have risen to above US$1,800 per ounce in response to high public spending, inflation-linked instruments are still pricing in 10-year average inflation below 2% as seen in Figure 1. Finally, shares of companies selling mostly inelastic goods (i.e., goods purchased regardless of price) may fare well in an environment of higher inflation and could be suitable investments if purchased at appropriate valuations.

Navigating the complexities of protecting against higher inflation is not easy but something that should be top-of-mind for investors preparing for a post-pandemic world. Consulting a financial advisor in the current environment would be well advised.

Zafrin Nurmohamed is a Senior Portfolio Manager, Asset Management, at Butterfield.

Sources: Bloomberg, Economist, Financial Times, Forbes

Disclaimer: The views expressed are the opinions of the writer and whilst believed reliable may differ from the views of Butterfield Bank (Cayman) Limited. The Bank accepts no liability for errors or actions taken on the basis of this information.

Related Videos