Despite slower growth than in the previous quarter, the gross domestic product of the OECD area has attained its pre-pandemic level in the third quarter of this year.

Between the fourth quarter of 2019 and the last period, OECD GDP increased by 0.5%.

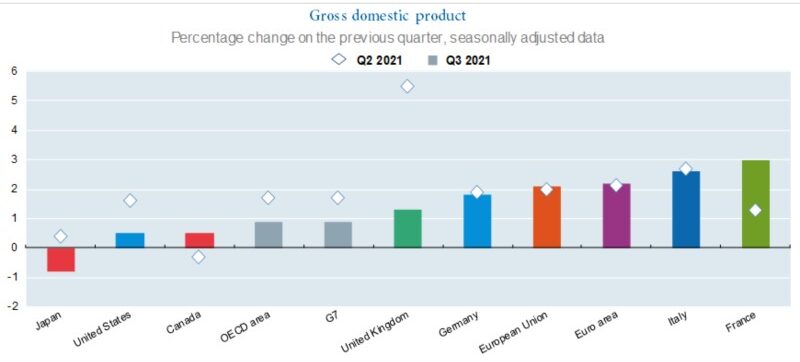

However, among the major seven (G7) countries, only the US economy exceeded its pre-pandemic size, by 1.4%.

Quarter-on-quarter growth in the OECD area also slowed to 0.9% from 1.7% in the second quarter. These growth rates were the same for the major seven (G7) economies.

In the third quarter, France recorded the strongest GDP growth of 3.0%, compared with 1.3% in the second quarter, followed by Italy (2.6%), Germany (1.8%) and the United Kingdom (1.3%).

However, the resurgence of COVID-19 cases, combined with new restrictions in Europe is putting the strong recovery from the pandemic on the continent into doubt for the fourth quarter.

However, the resurgence of COVID-19 cases, combined with new restrictions in Europe is putting the strong recovery from the pandemic on the continent into doubt for the fourth quarter.

Signs that the post-pandemic economic rebound may have reached its peak, particularly in the US, the UK, Germany and Japan, are already expressed by OECD composite leading indicators.

These indicators contain data from order books, building permits, confidence indicators, long-term interest rates, new car registrations and others to anticipate fluctuations in economic activity over the next six to nine months.

Among major emerging-market economies, CLIs suggest growth may lose momentum in China and India. China is currently considering new stimulus measures in the face of a stuttering economy and rising prices.

The indicators point to moderate economic expansion in Canada and the euro area.

Merchandise trade plateaus

In the third quarter, international merchandise trade for the G20 countries plateaued at a record high, after four quarters of sustained growth.

G20 merchandise exports and imports increased by 0.9% and 0.4%. This represented a marked slowdown compared to the first half of the year, when rising commodity prices boosted the value of traded goods.

High demand for electronics and high energy prices continued to play a role in the third quarter, whereas overstretched semiconductor supply-chains weighed on trade in vehicles and parts, the OECD reported.

In contrast, services exports and imports for the G20 during the period are estimated to have grown by around 5.1% and 5.8%, respectively.

Labour supply could become an issue

The unemployment rate in OECD countries overall fell for the fifth consecutive month to 5.8% in September. This is just half a percentage point higher than before the pandemic in February 2020.

The unemployment rate peaked in April 2020, but the subsequent decline should be interpreted with caution the OECD noted.

The unemployment rate may conceal additional slack in the labour market due to the pandemic. For instance, some non-employed people may be considered to be out of the labour force because they are not able to actively look for work or they are not available to work.

While labour force participation has rebounded rapidly in Europe, about 4 million workers have left the labour force in the US and in the UK; population change and economic inactivity means almost a million fewer people are in the workforce than there would have been without the pandemic.

Reduced migration and an increase in early retirement in some countries has exacerbated the problem to the extent that labour supply shortages are now seen as a major threat to a global economic recovery.

In the US this week, new applications for US unemployment benefits fell to their lowest weekly level in more than five decades.

Related Videos