A lot of attention has been given to ESG investing, which incorporates environmental, social and governance factors into the investment process.

The United Nations’ Principles of Responsible Investment, the largest corporate sustainability initiative, has attracted more than 3,800 signatories since 2006.

These asset owners and investment managers, who commit to include ESG elements around six principles into their investment decisions, have more than US$100 trillion in assets under management.

But how much impact is ESG really having on making companies more sustainable?

For Bruce Usher, professor at Columbia Business School, how ESG works on the investment side is well understood but the impact on environmental, social and governance issues is not yet as clear.

At the virtual Caribbean ESG Financing Summit held 17-18 Nov., Usher noted that academic research indicates ESG investing is a success story.

As asset owners are pressuring investment managers to incorporate ESG factors into their investment decisions and the managers are asking the companies they invest in to report ESG data, these companies, in turn, notice that their employees and their customers are interested in this type of data as well.

“As companies start to put this information out there, they find that their employees really want to be involved with companies that they view as sustainable,” Usher said.

Academic research suggests this increases staff loyalty and improves the ability of companies to recruit employees.

Customers, meanwhile, prefer products and services from companies that they believe are sustainable, with research data suggesting that ESG-conscious consumers are more loyal and less price sensitive.

ESG investors, on the other hand, tend to be more stable long-term capital providers.

The most important and most controversial element, Usher said, is the impact of ESG investing on performance.

“There appears to be some increasing evidence that when companies become strong on ESG, that they get better risk-adjusted returns,” he said.

A Morgan Stanley study, for instance, had shown that sustainable funds or ESG funds do not necessarily produce higher returns, but that during periods of high market volatility, they generate more stable returns than traditional funds.

As a result, the risk-adjusted returns of ESG funds appear to be higher.

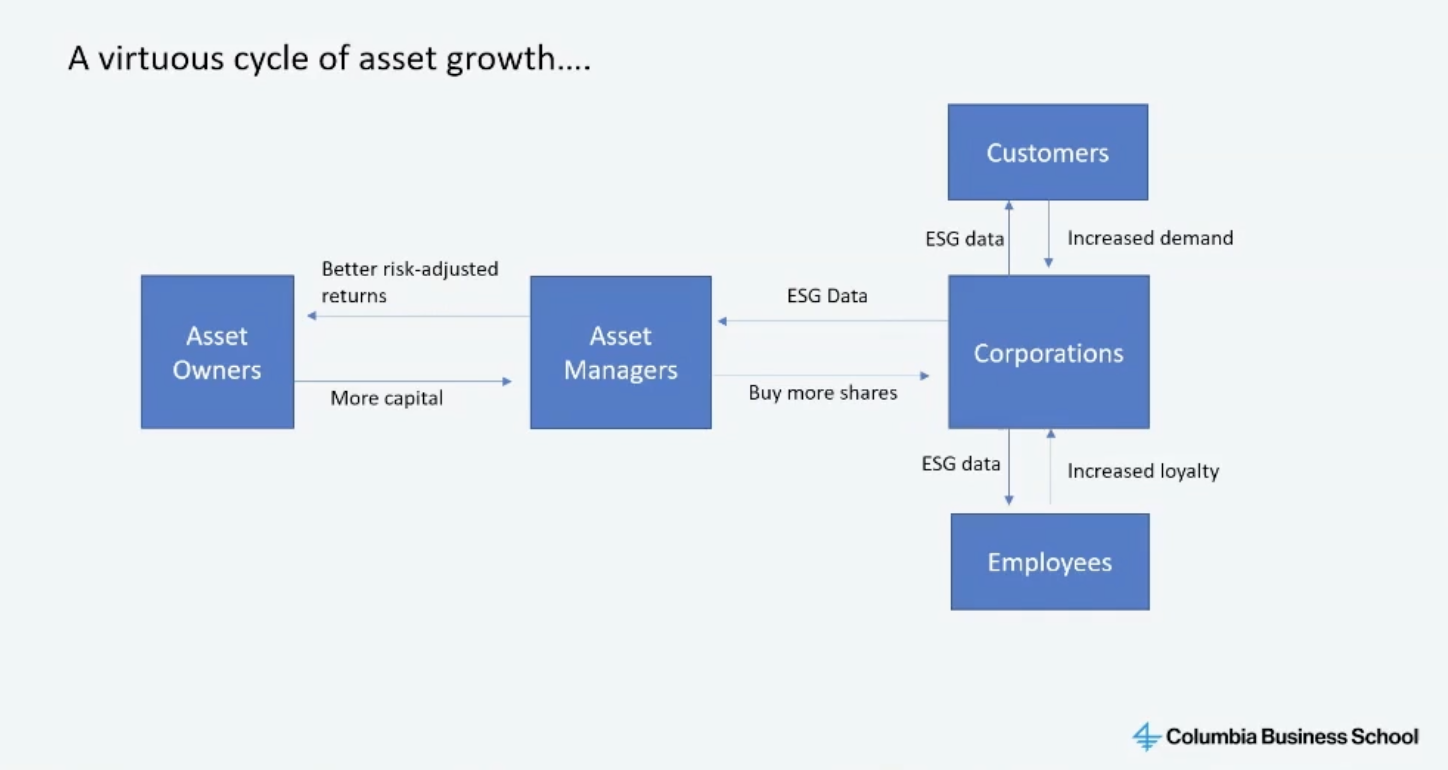

“The implication of the growth in ESG investing is that we’re getting a virtuous cycle of asset growth,” he said.

Investors force companies to report ESG data, which creates higher returns and more capital inflows. In addition, companies that are strong on ESG develop a competitive advantage in terms of attracting and retaining staff, customers and investors.

Investors force companies to report ESG data, which creates higher returns and more capital inflows. In addition, companies that are strong on ESG develop a competitive advantage in terms of attracting and retaining staff, customers and investors.

In many cases, companies that can demonstrate their strength in terms of ESG factors tend to be good at management in general, he said. “And so ESG becomes almost a proxy for management quality.”

Ray Klien, group head, investment banking at Republic Bank agreed, noting that when an organisation signs up to the Principles of Responsible Investing, the required data-collection exercise forces an organisation to make data more usable.

“So as a byproduct of this whole exercise, I think we’re uncovering potential ways to optimise our business that are outside of sustainability.”

But there are also challenges.

The lack of definitions and standardised metrics around ESG make it difficult to compare one business to another. It also opens the door for greenwashing, which poses a reputational risk, not only for individual companies but the entire ESG investment framework.

ESG investing raises awareness and brings attention to the issues but “it’s unclear how much impact ESG has on environmental, social and governance factors”, Usher said, and the expectations around the potential impact may be too high.

“One of the things I say to my students is to be good investors, it’s not easy. And changing the world for the better, that’s not easy, either. So putting these two things together, which is kind of what ESG is, is [very difficult].”

Focussing on the positive

Bert van der Vaart, co-founder and co-CEO of SEAF, said in the past five or six years the global impact private equity manager has been focussing increasingly on making a positive impact, rather than use ESG criteria to manage risks.

SEAF, which invests in small- and medium-sized enterprises, works like others with extensive questionnaires, gender equality scorecards and benchmarks and talks with the companies it wants to invest in about the issues.

But these companies need to do more than just avoid the red flags and risks associated with ESG criteria. ESG factors need to be built into their business and must be part of their growth story.

When investing in agricultural technology, it needs to involve companies that clearly add to food security or deal with climate adaptation. When investing in technology deals, the focus is on the inclusive element, Van der Vaart said.

“If they’re not embedded, we don’t feel very comfortable, because it’s difficult to get an entrepreneur to do something that he or she is not really focussed on. It’s not even fair for them to distort what their business model is.”

Finding the embedded nature of ESG involves setting up metrics in specific areas.

In terms of the reporting, whether through scorecards or qualitative reports, van der Vaart said, “We try to make sure that the investee understands why that’s good for their business, as well as why this is information that the investors want to see.”

Related Videos