At approximately 8pm Eastern Time on Tuesday, 7 April, US President Donald Trump posted on Truth Social announcing a “double sided ceasefire” with Iran. Less than two hours earlier, he had threatened to wipe out an entire civilisation.

At approximately 8pm Eastern Time on Tuesday, 7 April, US President Donald Trump posted on Truth Social announcing a “double sided ceasefire” with Iran. Less than two hours earlier, he had threatened to wipe out an entire civilisation.

S&P 500 futures soared more than 2.5% in after-hours trading. Oil plunged 15% one of its steepest single-day falls in years.

If you had sold out of the market that morning, quite understandably, given the rhetoric, you missed all of it. Every cent of it.

That is not an accident. That is how markets work.

The fear is always rational – the exit rarely is

Picture a common scenario: Markets have been rattled for weeks by geopolitical headlines. Trump is posting about ground invasions and nuclear infrastructure. You have a $100,000 portfolio and it is falling. Every instinct tells you to protect what you have move to cash and wait for things to calm down.

This is a deeply human response. But the data tells a ruthless story.

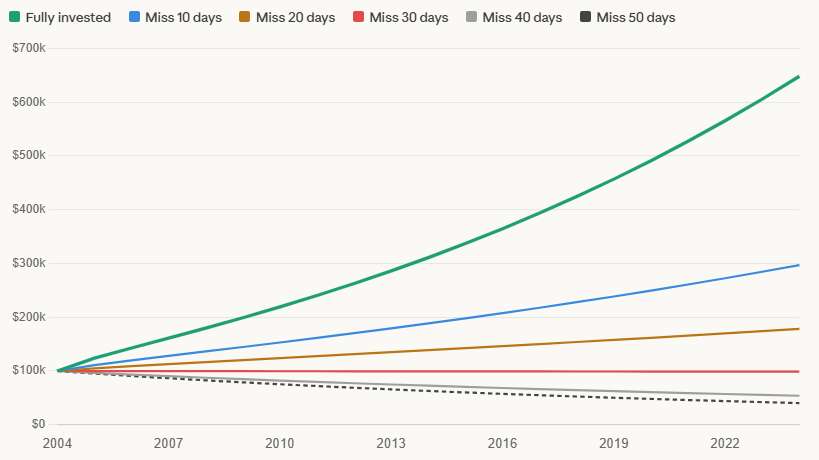

Over the past 20 years, that US$100,000 invested in the S&P 500 and left alone would have grown to roughly US$648,000. Miss just 10 of the best trading days across those two decades – 10 days out of approximately 5,000 – and you end up with US$297,000 instead. Miss 30 of the best days and your portfolio barely breaks even in real terms, finishing at around US$99,000.

You sat through 20 years of anxiety, held through every crash and recovery, and made almost nothing because you were out of the market on the wrong 30 days.

The bounce follows the crash

Here is what makes this so punishing. The best days in the market almost always occur directly alongside the worst days. This is not folklore, it is one of the most well-documented phenomena in financial research.

Morningstar examined S&P 500 data from 1990 to 2026 and found that the median gap between one of the 10 worst trading days and one of the 10 best trading days was just seven calendar days. One week.

The COVID-19 crash of March 2020 is the starkest example: Three of the 30 best days and five of the 30 worst days all landed within eight trading sessions of each other. Six of the seven best days that year occurred within a week of a worst day.

The pattern repeats across every crisis.

The Global Financial Crisis of 2008 produced some of the largest single-day gains in market history sandwiched between catastrophic falls, days apart.

The mechanism is always the same, fear-driven selling creates a dislocation, prices overshoot to the downside, and then the market snaps back, often violently and often overnight, before most investors have had a chance to reconsider their decision to exit.

Which brings us to the second truth the data reveals.

Most market gains happen when it is closed

This one surprises people. Over 95% of all trading volume occurs during market hours. Yet over the past 30 years, nearly all of the S&P 500’s cumulative gains have been earned overnight in the hours between the closing bell and the next morning’s open. Intraday returns across three decades amount to barely 12% in total. The overnight component accounts for close to 1,900%.

The nighttime ceasefire announcement is a textbook illustration. The market was weak all day on fears of escalation. The deal was struck just before 8pm. By the time trading resumed, the move was already largely made in the overnight futures market, while most investors were watching the news from their sofas.

This matters enormously for the typical investor. Most clients are not professional traders monitoring a Bloomberg terminal throughout the day. They have careers, families and businesses. They want their money to work for them, not to require them to work for it. The data suggests this is entirely achievable, but only if they stay invested.

The moment they step out, they risk missing the gains that are most likely to arrive without warning, outside of trading hours, triggered by a tweet or a phone call between heads of state at 7.45pm in the evening.

Trump isn’t the only source of volatility

It would be tempting to treat the current environment as uniquely unpredictable. In some respects, it is. Markets are now genuinely reactive to social media posts in ways they never were before, and even seasoned Republican allies have acknowledged that second-guessing this president’s intentions is an exercise in futility.

But those who have watched Trump operate across two administrations will recognise a pattern. The aggressive opening position, the threatened ground invasion of Greenland, the sweeping tariffs on Canada and China, the Venezuela posturing, and now the Iran brinkmanship is a negotiating tactic.

Tough talk and maximum leverage are core to the Trump playbook, and the resolution, when it comes, tends to arrive faster than the markets expect. The investor who sold on the tariff announcement missed the rebound. The investor who sold on the Iran escalation missed Tuesday nights rally.

The honest message to any investor sitting on a decision right now is this: The world will always produce reasons to wait. There will always be a more comfortable moment to get back in. That moment, historically, arrives after the recovery has already happened.

Listen to the data

Stay invested. It is the most boring advice in finance and the most consistently vindicated by evidence. Not because the market always goes up in the short term – it does not – but because the cost of being out on the wrong days is catastrophic and largely invisible until it is too late.

The market rewarded those who held through the 2008 financial crisis, the 2020 pandemic crash, and every episode of geopolitical panic in between. In each case, the investors who locked in their losses and waited for calm missed the very days that drove the subsequent recovery.

The ceasefire may hold. It may not. Talks resume in Islamabad this week and the gap between Washington’s and Tehran’s stated positions remains wide. Markets may well give back some of Wednesday’s gains before the week is out. That is fine. It is noise within a longer signal.

The signal says: Time in the market beats timing the market. It said it in 2009. It said it in 2020. And on the night of 7 April, as S&P 500 futures surged while most people relaxed on their couch, it said it again.

Robert Whelan, a chartered accountant, is the portfolio manager at NCB Capital Markets (Cayman) Ltd.

Related Videos