The latest corporate tax statistics from more than 160 countries highlight the continued risk of profit shifting by multinationals and underlined the need for international tax reform, according to the Organisation for Economic Cooperation and Development.

The OECD, which attempts to establish an effective minimum global corporate tax rate of 15%, said its annual corporate taxation report and the included country-by-country reporting data from close to 7,000 corporations was a major boost to tax transparency.

It said the latest country-by-country reporting data, from 2018, showed that in zero-corporate-tax jurisdictions the median value of revenues per employee is US$2 million, compared with just $300,000 elsewhere.

Zero-tax jurisdictions also have a higher share of related party revenues of 35%, whereas the average share of related party revenues in high-, middle- and low-income jurisdictions is around 15%.

“While these effects could reflect some commercial considerations, they are also likely to indicate the existence of BEPS [base erosion and profit shifting],” the OECD said.

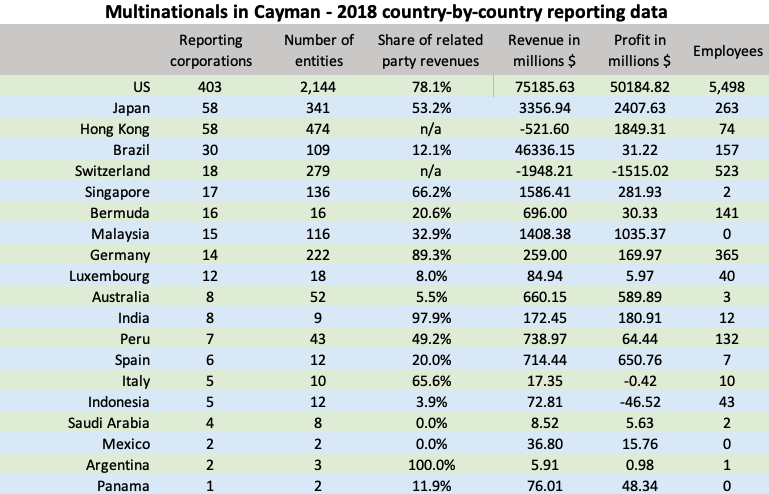

Data from Cayman shows mainly US activity

Not many countries are reporting the country-by-country data they receive from the Cayman Islands, and those that do present it only in aggregated form to keep the companies involved anonymous.

Available OECD data shows mainly the activities of 403 US corporations, which had 2,144 subsidiaries in the islands. In 2018, they collectively generated revenues of $75.2 billion, most of which, 78.1%, came from related-party transactions. This resulted in a profit before tax of $50.2 billion. The income tax paid or accrued for the year comes to $458 million.

In 2019, 400 US corporations reported a Cayman Islands-based revenue of $72 billion and a pre-tax profit of $60.37 billion.

Accumulated earnings of US corporations in Cayman dropped by more than half between 2018 and 2019 from $191 billion to $81.3 billion.

US corporations reported 5,498 employees worked for their Cayman affiliates in 2018. That number increased to 6,055 a year later.

Given that the entire financial services sector, including business support services, employs only about 6,000 to 7,000 people in the islands, the US corporations’ reported employment figures suggest that most of the multinationals’ staff is employed outside of Cayman.

Other countries with notable multinational activity of more than a billion dollars in revenue in Cayman are Japan, Hong Kong, Brazil, Singapore and Malaysia.

Tax reform delayed

International corporate tax reform plans by the OECD have hit a snag in recent months. The so-called Pillar One and Pillar Two proposals were due to come into effect by next year, but some of the details are still under discussion.

In the European Union, Hungary was vetoing the introduction of a 15% minimum corporation tax, the so-called Pillar Two, arguing that it would make its companies less competitive, but finally joined in October.

In the United States, the proposed Pillar One rules, which would introduce tax on a portion of the profits of the largest tech companies in countries where they do significant business, but may not have a physical presence, are facing strong opposition from the Republican party.

G20 leaders at their meeting in Bali, Indonesia, earlier this month called on the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS) “to finalise Pillar One, including remaining issues and by signing the Multilateral Convention in the first half of 2023, and to complete the negotiations of the Subject to Tax Rule (STTR) under Pillar Two that would allow the development of a Multilateral Instrument for its implementation”.

Corporate income tax rates stable

The OECD said corporate income tax remains an important source of revenue for most countries, especially for developing and emerging market economies.

On average, the corporate income tax accounts for a higher share of total taxes in Africa (18.8%), Asia and Pacific (18.2%), and Latin America and the Caribbean (15.8%) than in OECD countries (9.6%).

The report found that after decades of corporate tax rate cuts, rates have stabilised this year, with some narrowing of tax bases, as countries attempt to strike a balance between raising revenue and incentivising investments.

Much of the stabilisation is likely the result of the fiscal constraints faced by governments after the COVID-19 pandemic.

The average statutory tax rate for all jurisdictions covered in the dataset was 20% in 2021 and 2022, compared with 28% in 2000.

There is some evidence that governments have used corporate tax regimes to boost economic recovery, by incentivising investment, especially in research and development.

Related Videos