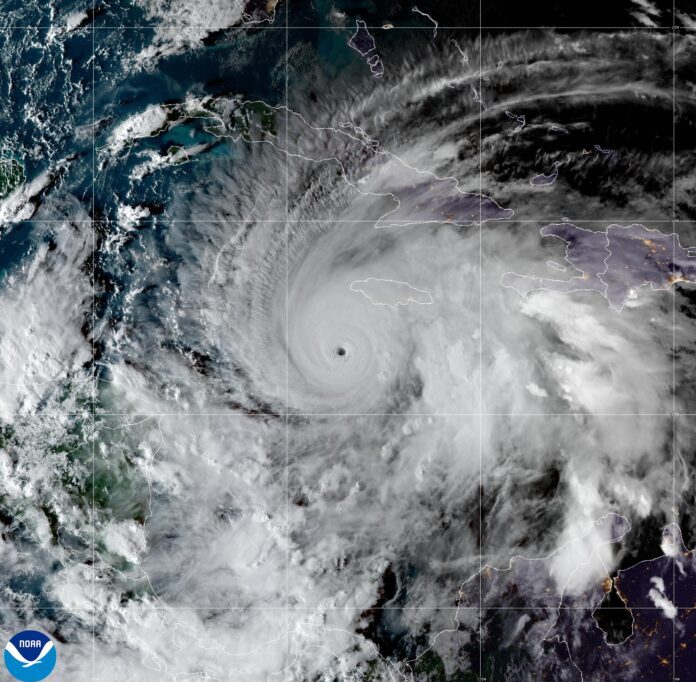

Hurricane Melissa has wrought billions of dollars’ worth of havoc across Jamaica, Cuba, Haiti and the Bahamas. And with the damage to Bermuda still unknown, it’s too soon to fully count the cost of the world’s strongest hurricane this year. Yet it’s already raising questions in the insurance industry.

‘Could have been worse’

This will be scant consolation to the hundreds of thousands of people impacted across the Caribbean, but Hurricane Melissa has, so far, been less destructive than expected. Michael Gayle, the CEO of Cayman’s government-backed insurance company CINICO, warns against making damage assessments this soon. Yet he believes the damage will be less than originally feared.

“Based on the magnitude of the storm and the path it was on, it could have been worse. I’m seeing photographs from Saint Elizabeth and the surrounding areas that were directly affected. If that same impact had occurred in Kingston, where there is a population of around a million people and far more built-up construction, the outcome would have been considerably worse.”

A UK-based reinsurance executive, who asked not to be named because of his company’s press policy, said “we are hearing numbers of around $10 billion worth of damage”.

Premium impact

Globally, property reinsurance costs are falling, following a relatively calm year for natural disasters in 2025. And even Hurricane Melissa may not have that much impact on premiums.

“The insurance penetration in Cuba and Haiti is pretty low, so damage there will not result in big claims on reinsurers,” said the UK-based reinsurance executive. “Cuba has strong sanctions against it by the US, so many brokers and insurance companies simply cannot trade there,” continued the source.

Jamaica has more extensive insurance coverage but if early damage assessments are correct, then Melissa-related claims would be readily absorbed by the international market. A loss of $10 billon would “not materially move the global reinsurance market”, said Gayle.

The indirect impact may be greater, though. “The concern, however, is what could have happened. Reinsurers react to risk potential as much as to actual outcomes. We are now seeing late-season Category 5 storms making landfall in the region.”

The force and late arrival of Melissa may make reinsurers increase premiums or even refuse to cover parts of the Caribbean.

Coverage concerns

“The broader concern is that the Caribbean may eventually face a situation where hurricane risk becomes uninsurable in conventional markets,” says Gayle. “Some [reinsurers] may decide to withdraw capacity.”

Both the rising cost of insurance and the threat of Cayman becoming uninsurable, was raised as a potential threat at September’s Property Update Forum 2025, organised by the Royal Institution of Chartered Surveyors.

“CINICO is building relationships now to ensure there is a mechanism for government-backed coverage if that day comes,” said Gayle.

Does Cayman need a ‘cat’ bond?

One factor working in Jamaica’s favour is its comprehensive insurance protection.

In 2024, the Jamaican government issued a natural catastrophe bond worth US$150 million. This works like a typical issuance, in the sense that international investors buy the bond and Jamaica must repay the principle plus interest, which in this case is reported to be around 7% per year. However, if Jamaica is hit by a hurricane that meets the parameters set by the bond, then it triggers a payout.

Unlike conventional insurance, the payout isn’t linked to the cost of damage to insured items. Rather, there are set specifications regarding the path and severity of the hurricane. The stronger and more direct the hit, the bigger the payout.

Hurricane Beryl, a Category 4 storm that passed to the south of Jamaica in 2024, caused extensive economic damage, yet didn’t trigger a payout from the natural catastrophe bond. But Melissa, which was Category 5 and passed directly over the island, is expected to pay the maximum amount of US$150 million.

One advantage of this type of cover is that the payout can be disbursed quickly as it doesn’t need adjudicators to evaluate a claim. Cayman does not have active natural catastrophe bond cover at present.

Cayman’s coverage

An important layer of protection for the Islands comes from the Caribbean Catastrophe Risk Insurance Facility, which was created in the wake of Hurricane Ivan and is headquartered in the Cayman Islands. A segregated portfolio company, the facility provides parametric cover – which pays out if specific meteorological conditions are met – to 19 Caribbean countries and several in Central America, including government-linked utilities.

“When Hurricane Beryl passed, the cat bond did not trigger, but CCRIF paid around US$26 million to Jamaica, and that payment was received within about two weeks,” said Gayle, who also sits on the facility’s board.

Another line of hurricane defence comes from the policies that Caymanians take out themselves. Anyone using a mortgage to buy a house in Cayman must have conventional property insurance.

But new options are also entering the market. Recently, parametric insurance, which traditionally was only designed for governments and institutions, is being offered to Caymanians. Both Hyperion and CINICO are selling parametric insurance in Cayman. Again, the principle is the same, if certain meteorological parameters are met, then the insurance company will pay out.

Related Videos