By Robert Whelan

The US economy has rarely felt so divided. On one track, the ‘Magnificent Seven’ companies – Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla – continue to power the S&P 500 to record highs. On the other, Main Street is showing signs of strain, as consumer earnings and spending patterns tell a story of fatigue.

Recent corporate results from major retailers and restaurants reveal a clear theme: consumers are trading down. Even McDonald’s, Chipotle and Starbucks have admitted that lower-income and younger customers are pulling back spending. The top 10% of households now account for roughly half of all consumer spending, underscoring how prosperity in the US has become increasingly top-heavy. This is the K-shaped economy, a market bifurcated between corporate giants building the future and everyday Americans tightening their belts.

The US markets are also showing this divergence in performance. While mega-cap tech companies power stock indices to record highs, consumer-focused names struggle. However, it is important to recognise that today’s market leaders are not just riding hype.

Magnificent performance

The Magnificent Seven are some of the most cash-generative businesses in history and they are using that strength to build the infrastructure for the next wave of AI technology. They are integrating artificial intelligence to make existing business lines stronger, while using it as a launchpad for new ones.

Meta is embedding AI to strengthen advertising efficiency and developing its Meta AI glasses to bridge digital and physical experiences. Alphabet and Amazon are integrating AI into search and their cloud offerings while experimenting with agentic AI, digital agents that can shop and plan autonomously. Tesla is racing toward fully autonomous systems, while Microsoft is boosting enterprise productivity through copilot.

Their strategy is clear: defend core profit engines while investing in the AI infrastructure layer that will power the next decade. While previous bubbles were fuelled by debt, current capital expenditure AI spending is fuelled by actual operating cash flows. However, not everyone is convinced. The sheer scale of AI spending, tens of billions in capital expenditure without a clear pathway to return on investment is starting to worry some investors.

Is AI the new arms race?

The AI boom is not just economic – it is geopolitical. Nvidia’s Jensen Huang recently warned that China could win the AI race, pointing to its cheaper energy, lower regulation and state-driven industrial policies. The US, meanwhile, is spending aggressively on semiconductor manufacturing and AI infrastructure, which looks to closely resemble the Sputnik moment of the Cold War.

Even the leadership of ChatGPT maker, OpenAI, has suggested that government financing may soon be needed to sustain the cost of compute and power required for frontier models. AI development has become a matter of national strategy, not just corporate ambition. That raises an uncomfortable question: are we seeing a new form of AI industrial policy bubble, where nations compete to outspend one another in an arms race of silicon?

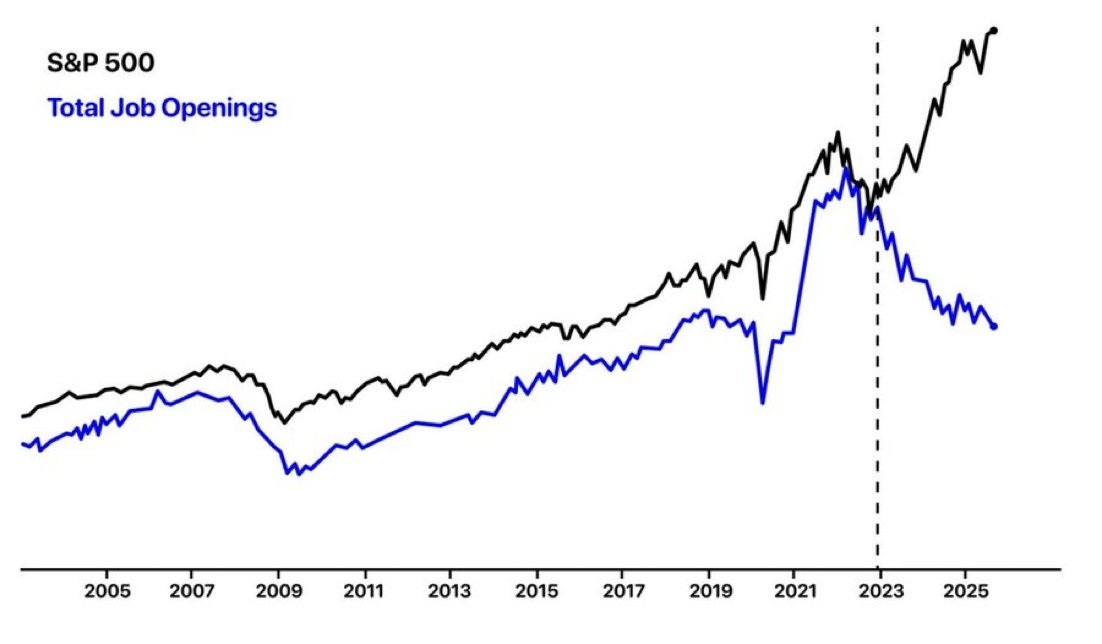

While corporate America builds toward an AI-driven future, the reality on the ground looks less futuristic. The labour market is cooling and job cuts are climbing. Corporate cost cutting, AI automation and federal layoffs are being touted as the reasons for cuts. For the top 10% of households these shifts translate into productivity gains and investment income (through business ownership and investment portfolios) and for the bottom half, they mean job insecurity and shrinking purchasing power.

Divided market

This divide makes it increasingly difficult for the Federal Reserve to set policy. Rate cuts could support the struggling lower-income consumer, but they could also reignite speculative excess in AI and tech spending. Inflation, meanwhile, is not fully extinguished. The Fed is caught between helping Main Street and not over-stimulating Wall Street.

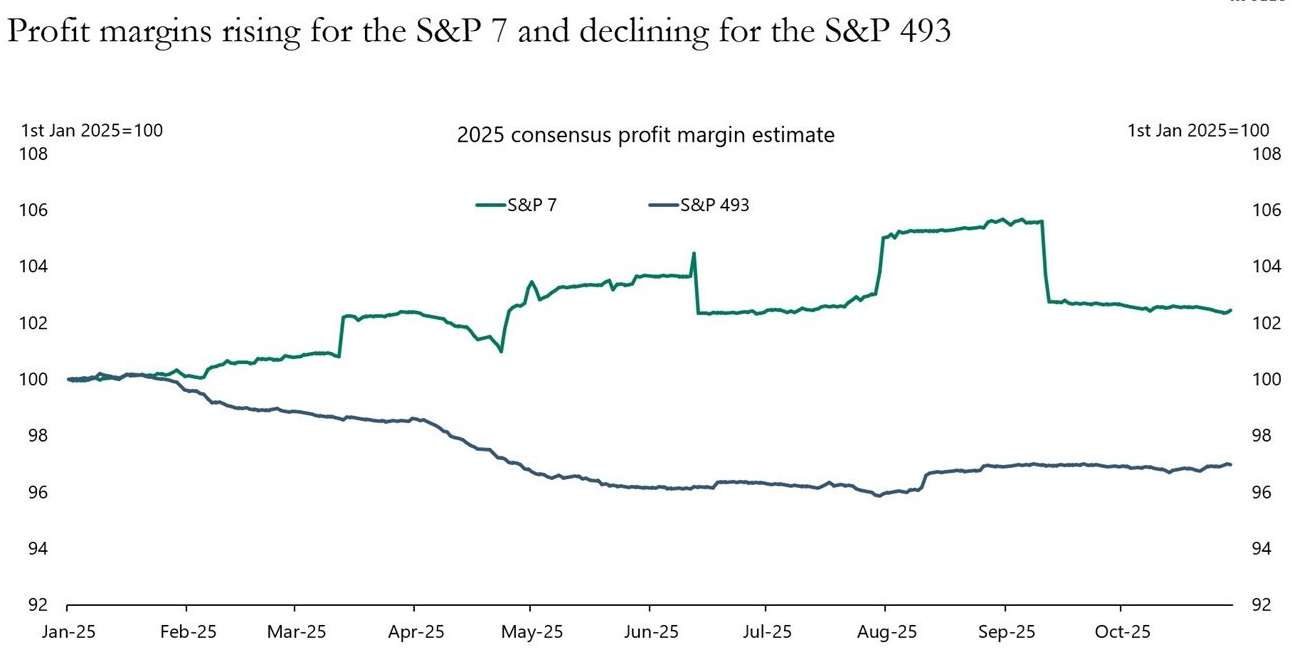

The market’s concentration only amplifies this challenge. The top seven companies now represent roughly one-third of the S&P 500’s market capitalisation, a level not seen in decades. That makes the index look healthier than it really is. Beneath the surface, many smaller companies, particularly in consumer sectors, are lagging.

Investors hoping to play safe peripheral themes such as industrials or utilities tied to AI infrastructure buildouts without a care for who is the AI winner, should be cautious. These sectors have been touted as beneficiaries of AI-driven energy and construction demand, but history shows how misleading that can be. The railroad era offers a useful analogy. The builders of the railways, today’s equivalents might be Oracle or semiconductor equipment firms, faced fierce competition and commoditised returns.

The real winners were the train operators, those who monetised the infrastructure through services, data, and scale: Alphabet, Amazon, and Microsoft. Similarly, investors should run a mile from the neoclouds and AI-linked energy names that are effectively leveraged bets on continued AI euphoria. If the AI story unwinds, these will be the first to blow up.

How to invest

Despite these risks, markets are entering what is seasonally the strongest six-month stretch of the year. The coming quarters will also see several potentially supportive developments: the end of quantitative tightening, easing financial conditions, and the rollout of the ‘big, beautiful bill’, which should provide a modest fiscal boost to consumers and industrial activity. These factors could offer short-term relief for risk assets, but they do not resolve the structural bifurcation in the economy. If anything, easier conditions could push investors further into the same over-crowded trades.

So how should investors position in a market that is both over-concentrated and fundamentally uneven? The first step is to stay with the structural winners. The Magnificent Seven still deserve core exposure. They are not speculative; they are profitable, dominant, and shaping the next phase of economic growth. But balance that exposure with sectors that can grow defensively, such as financials and healthcare, which remain under-owned and provide diversification against lofty tech valuations.

Avoid consumer staples and discretionary stocks, which face continued headwinds as household budgets tighten and credit conditions remain tough. Be wary of leveraged AI plays; neocloud, data-centre energy and AI hardware suppliers will be hit hardest if capital expenditure slows. And crucially, stay diversified internationally, because the AI story will have global winners and concentration risk in US mega-caps is becoming somewhat excessive.

The US is running on two speeds. Wall Street is racing ahead, driven by technological optimism and global capital flows, while Main Street is slowing under the weight of inflation, automation, and inequality.

For investors, the goal is not to pick sides but to navigate both realities. Embrace innovation, but do not ignore fragility. Stay diversified, avoid leverage, and remember that even in a railway boom, not every railway builder gets rich. In a K-shaped economy, balance is not just prudent, it is essential.

Robert Whelan, a chartered accountant, is the portfolio manager at NCB Capital Markets (Cayman) Ltd.

Related Videos