CFA, MBA

Chief Investment Officer

Better-than-expected job growth put an end to the equity market’s winning streak last week.

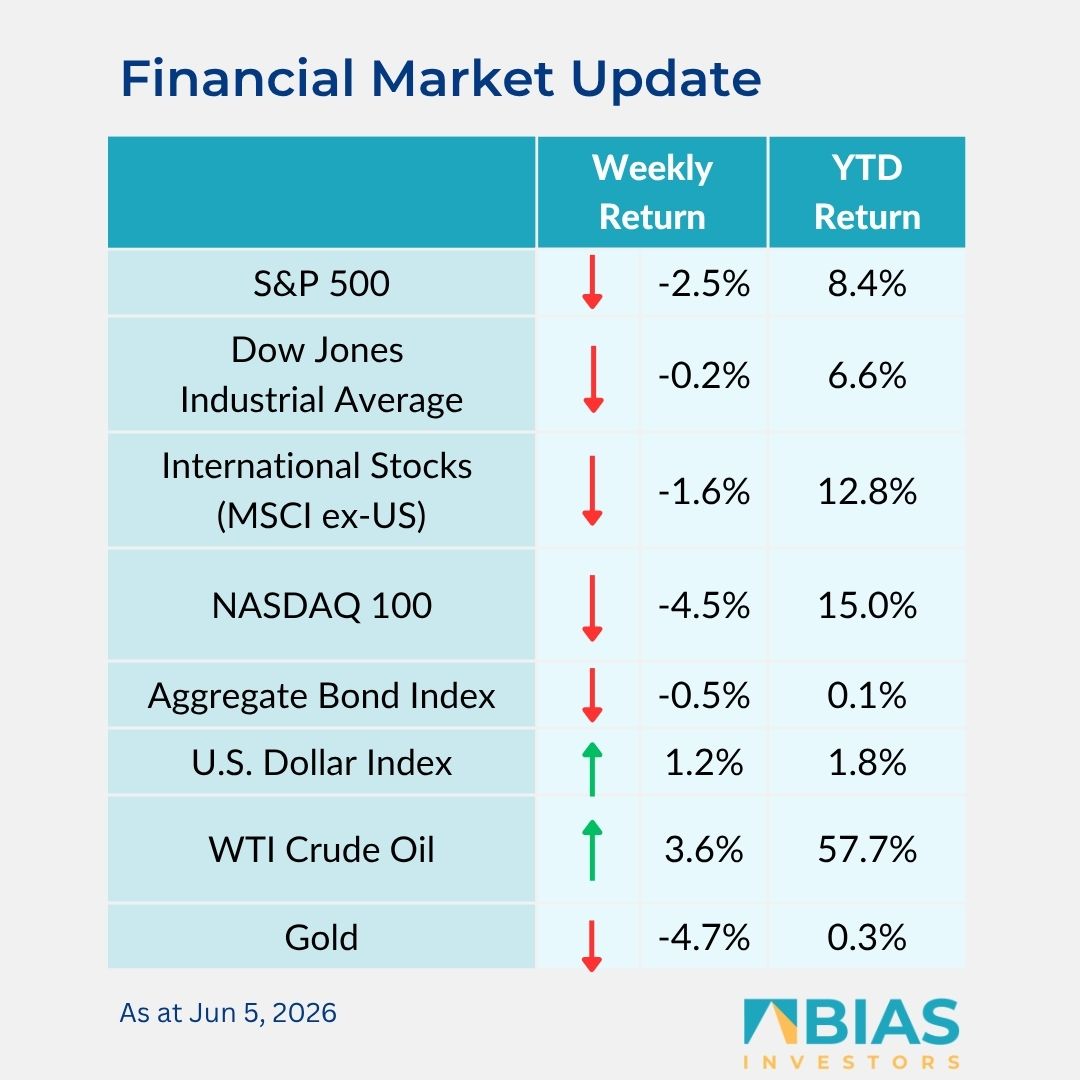

For the week, the S&P 500 Index was -2.5%, the Dow Jones Industrials -0.2%, and the NASDAQ -4.5%. The energy, healthcare, and real estate sectors led the S&P 500 Index for the week, while the consumer discretionary, technology, and communications services sectors lagged.

The 10-year US Treasury note yield was 4.546% at Friday’s close versus 4.439% the previous week.

The May Employment Situation report showed a net gain of 172,000 jobs versus an expectation of 96,000 jobs. April jobs were revised up by 64,000 to 179,000 from 115,000, and March jobs were revised up by 29,000 to 214,000 from 185,000.

The May unemployment rate was unchanged at 4.3%. This strength in the labour market increases the likelihood the Federal Reserve can remain patient on any monetary policy changes and possibly increase rates later this year if both labour market strength and inflation persist. This helped trigger the Friday sell-off in the equity market.

We should get a clearer sense of monetary policy direction when the Federal Reserve publishes its updated Summary of Economic Projections at the 17 June FOMC meeting.

Current CME Fed funds futures show the potential for a 0.25% increase at the October FOMC meeting.

The first=-quarter earnings should close out with a year-over-year gain of 28.8% and revenue growth of 11.8%. This week two companies are scheduled to report results.

Second-quarter earnings are expected to grow by 21.7% and quarterly revenue growth is expected at 12%. Full-year 2026 earnings are expected to grow by 22.8% with revenue growth of 10.8%.

In our ‘Dissecting headlines’ section, we look at factors of labour market stability.

Dissecting headlines: Labour market analysis

Strength in the labour market may seem confusing as headline concerns of tariff uncertainty and AI-induced layoffs would point to much weaker job creation.

That felt like the case in February when the initial employment report saw a net loss of 92,000 jobs and was later revised lower to a net loss of 156,000 jobs.

Starting in March, the labour market improved and the past three months have seen strong job growth of 214,000 in March (revised up from an initial 178,000), 179,000 in April (revised up from 115,000), and now 172,000 jobs in May.

The monthly jobs data is always ‘net jobs’, meaning the net of job losses and new hires. The environment has been described as “low hire, low fire”, so the impact of new job growth appears stronger in a low job-loss scenario. Layoffs have been relatively lower, workers quitting jobs has declined, and older workers are not retiring at the same rate.

At the same time, we are seeing steady hiring in several sectors to include healthcare, where there is a structural need for workers due to ageing population.

May also saw an increase in leisure and hospitality, and anecdotal evidence from Federal Reserve surveys point to both a resilient consumer and anticipated hiring ahead of the FIFA World Cup.

Local government hiring was also a source of strength in May and can be attributable to a post-pandemic shortage of municipal worker positions now being filled and population growth in the southern states requiring more local government workers.

A last element may be ‘unretirement’, Americans older than the age of 55 either delaying retirement or returning to work for economic reasons, as well as longer life expectancy and sense of purpose.

This is a post-pandemic trend for some workers that may have taken early retirement or forced out of work during the pandemic period coming back into the labour market.

These factors have combined to create a labour market that has shown resiliency the past few months.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos