Siddhant Jain Jaiswal

Facing existential crisis, it is only natural that human perspective will change for better or for worse.

Although the pandemic is first and foremost an existential public health threat, it also likely represents the dawn of a new economic world order and a reshaping of the global economy.

Today’s new environment offers an opportunity for companies, governments and civil society groups to think critically about what their role might be in creating a more resilient future. The investment industry is not immune to this either.

One critical way of thinking on how to create resilience is ESG investing. ESG stands for Environmental, Social and Governance-related parameters used to assess how companies are interacting with all their stakeholders and society in general as part of their business processes. The term ESG was first used in a December 2004 report titled, “Who Cares Wins.” The focal message in the report was that, ultimately, successful investment depends on a vibrant economy, which depends on a healthy civil society, which is ultimately dependent on a sustainable planet.

Even though ESG does not have a set framework in place, the following three primary considerations need to be considered by a company to achieve a sustainable planet:

- Environmental framework. This will pertain to tackling issues on air, land, water and the ecosystems. These issues can be tackled through better utilisation of resources, adhering to carbon credits, and executing environmental reporting or disclosures.

- Social framework. This considers the impact that companies can have on society. A company can promote and be part of social activities such as managing employee relations, having diversity and inclusiveness in the workplace, adhering to health and safety, and protecting human rights.

- Governance framework. This focusses on how a company is run. It addresses areas such as corporate risk management, board accountability, protecting shareholders, and reporting and disclosing Information.

ESG investing seeks positive returns, not at the expense of the planet or good behaviour, but because of good governance, care for the environment and concern for society. The philosophy argues that focussing on those will create demand for a company’s products and thus improve long-term success. ESG investing has sometimes been used interchangeably with sustainable and responsible investing – an umbrella term which emphasises financial returns as a secondary consideration after the investors’ moral values have been accounted for in their decision-making. But because so many of the definitions are elastic and change over time, I recommend focussing on the intentions of ESG investing rather than getting hung up on specific labels.

Whilst the financial metrics have traditionally been the major criteria for choosing investing opportunities, the consciousness about integrity and ethics of companies and the impact of their policies on the social and environmental ecosystem have begun to change that norm.

Living in a rapidly changing world, and thanks to technology, investors now have greater access to information. Various sources and methods are now being used by both value-motivated and values-motivated investors in evaluating the impact to the environment, society and governance across companies.

One such source is the S&P 500 ESG Index, which is designed to measure the performance of companies meeting the ESG principles using an ESG scoring methodology. This score is expected to have an impact on a company’s growth, profitability, capital efficiency and risk exposure in the investment process.

Some of the score criteria revolve around excluding companies that either directly or indirectly are invested in tobacco or controversial weapons or are performing poorly on the United Nations Global Compact score, which promotes the principles of human rights, labour and anti-corruption.

In contrast, to be included in the S&P 500 index, a company should be US-based, have a market capitalisation of at least US$5 billion, be highly liquid, have a public float of at least 50% of its shares outstanding, and its most recent quarter’s earnings and the sum of its trailing four consecutive quarters’ earnings must be positive.

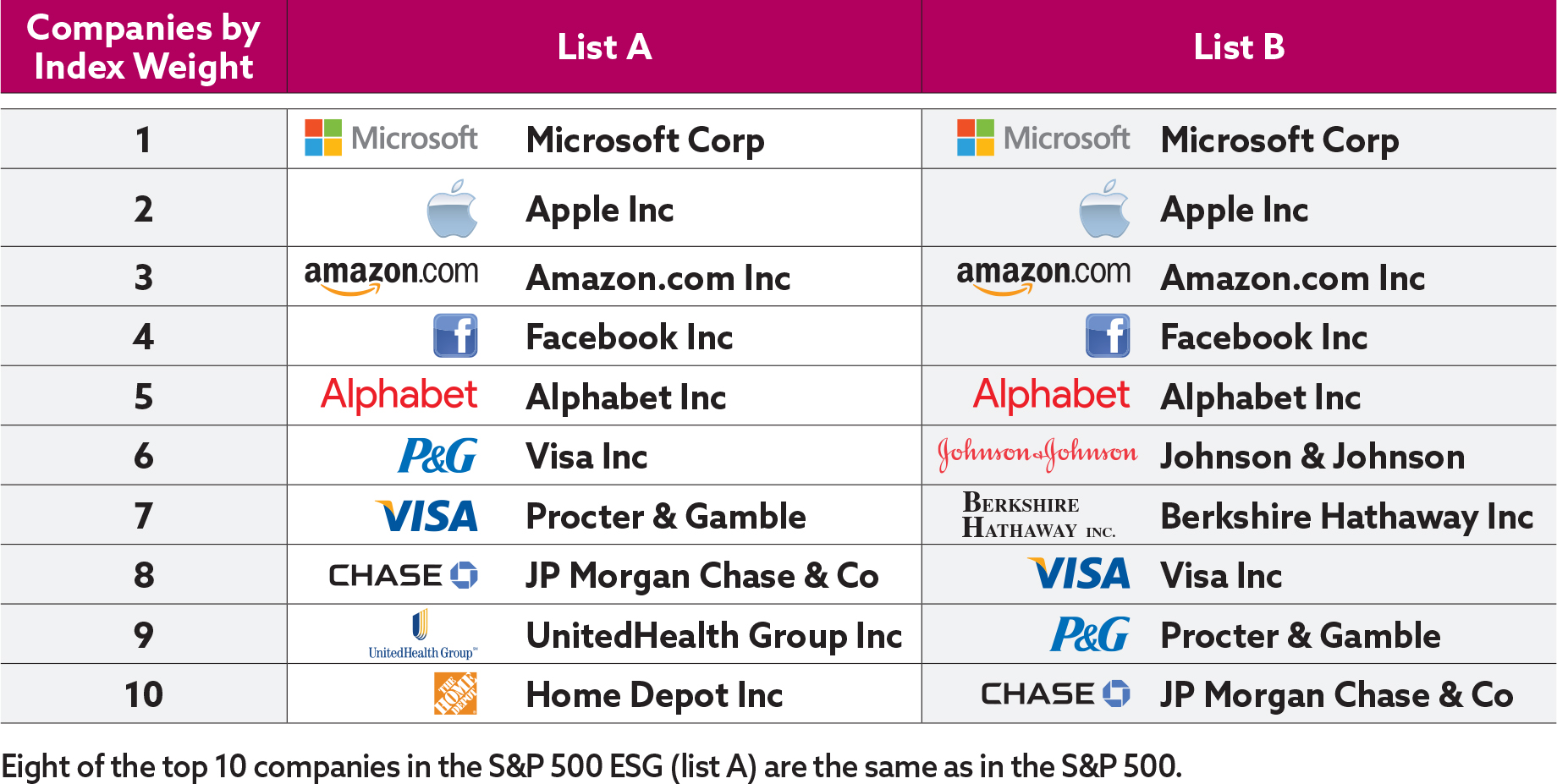

Let us take a look at the two lists A and B in the table. These represent the S&P 500 and S&P 500 ESG indices. By just glancing through these lists, can you identify which one of them is the ESG index?

You can forgive yourself if you had difficulty choosing the correct list. The correct list is A.

Eight of the top 10 companies in the ESG index are the same as those in the S&P 500 index. As of 30 June 2020, the S&P 500 comprises 500 companies, representing an adjusted market capitalisation of more than $25 trillion. Of these total companies, only 310 form part of the ESG Index, representing an adjusted capitalisation close to $19.5 trillion. A whopping $6 trillion, representing 25% of the S&P 500 market capitalisation is excluded from the ESG Index. This goes to show that, just because a company is performing well on its financial parameters, it does not mean it is doing well on its non-financial parameters as well. This is why focussing on the non-traditional risks is equally important.

Given the rigorous compliance and due diligence requirements for a company to work towards a strong ESG score, there was a lingering misperception that ESG considerations adversely affect financial performance. In recent years, some investors have felt so irritated by the pious tone of the ESG sector they have joked that the ESG abbreviation should stand for “eye-roll, sneer and groan”. Such derision, though, is looking hollow now. In terms of performance, for January-June 2020, the S&P 500 ESG index beat the S&P 500 index by 1.7%. This is impressive given that the objective of the ESG index is not to outperform the S&P 500 benchmark.

An ESG lens teases out all sorts of risks that are not necessarily apparent in conventional financial analysis. A high ESG score may be a good signal of good executive teams, which may translate into being better long-term custodians of investor capital and stronger long-term returns. This screening may be the reason that the S&P ESG 500 index has outperformed its parent index in the recent sell-off.

Companies obviously want to survive the current crisis but increasingly their customers and their employees are asking them not only whether they can survive, but if they can also become more resilient to future shocks and more respectful of the planet that they operate on. ESG is an increasing force in the investment industry and one that many investors treat extremely seriously. Real money is at stake. ESG is a theme that is becoming not just a luxury, but indeed a necessity, in the present-day scenario and cannot be ignored.

Please note: This article is not suggesting that ESG investing is right for each investor. You should consider the above information not as a de facto recommendation, but as an idea for further consideration. As always, consult your financial professional before making any investment decision.

Siddhant Jain Jaiswal is a member of the CFA Society of the Cayman Islands.

Related Videos