For two years the government has addressed a critical evaluation of Cayman’s anti-money laundering regime with a raft of regulatory and legislative changes. Yet, last week, the Financial Action Task Force added Cayman to its watchlist of countries in need of increased monitoring.

The global standard-setter in the space believes Cayman’s financial regulators had not imposed enough fines on both financial institutions for AML breaches and on service providers and their clients for failing to provide accurate and up-to-date beneficial ownership information.

The move does not directly impact doing business with or through the Cayman Islands. But being placed on the FATF’s so-called grey list is a blow to Cayman’s reputation as a financial centre.

One might be forgiven for assuming that equating Cayman with the likes of Zimbabwe, Yemen or Pakistan, who are also on the list, would provoke an angry reaction locally.

Instead, the government hailed its efforts in implementing almost all of the recommendations made in a mutual evaluation report released by the FATF’s Caribbean body, CFATF, in March 2019.

The government noted that it had completed 60 of the 63 actions recommended in the report.

Premier Alden McLaughlin said the three remaining actions were all about the effectiveness of the legal framework, in terms of compliance and enforcement in detecting and deterring financial crime.

Industry association Cayman Finance said it appreciates the efforts of the government so far and will continue to support it in addressing the few remaining issues so that Cayman can be removed from increased monitoring at the earliest opportunity.

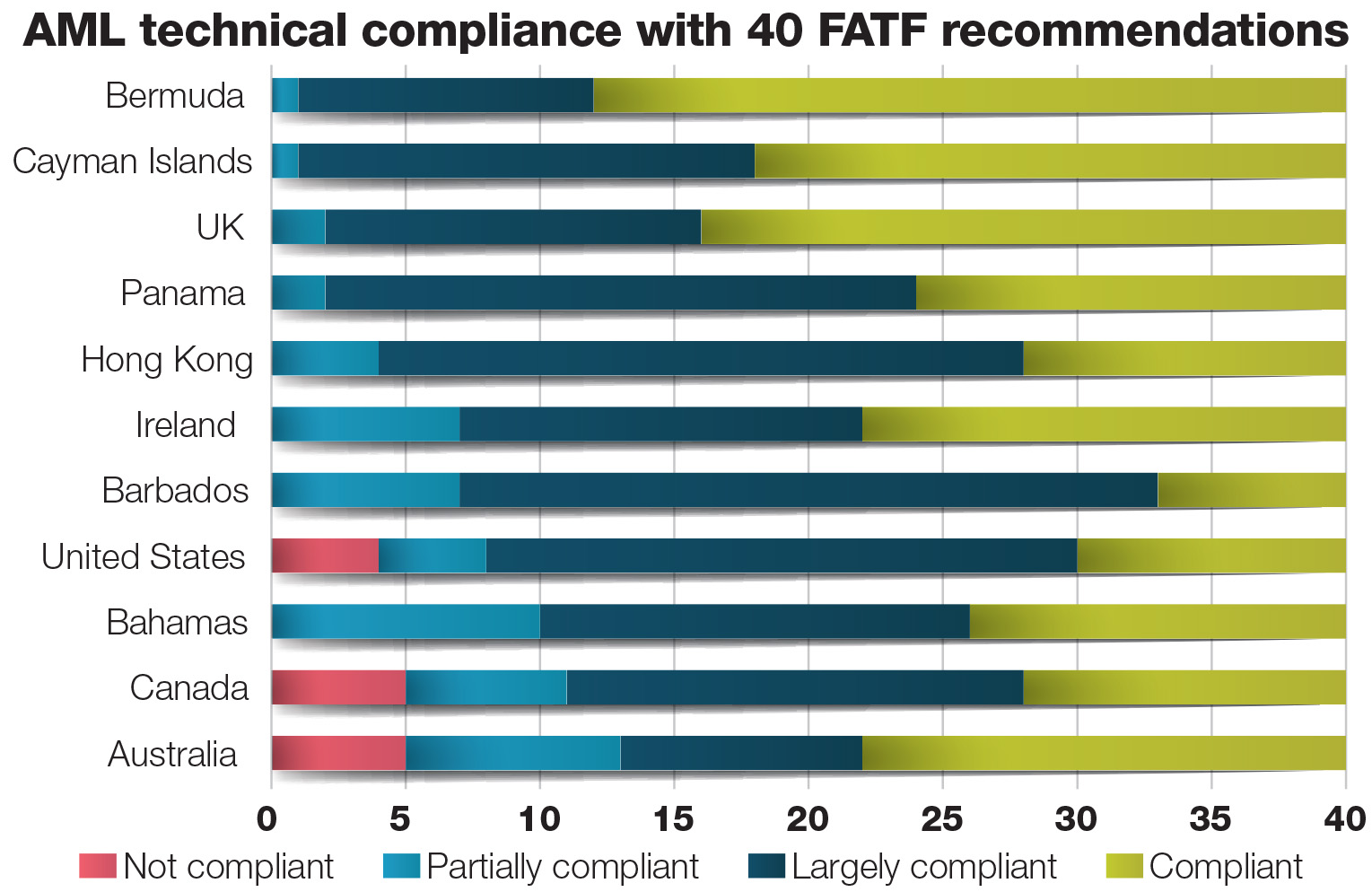

Technical compliance

Attorney General Samuel Bulgin, who is chairman of the Cayman Islands Anti-Money Laundering Steering Group, even spoke of the “excellent outcome” with regard to Cayman’s technical compliance with global AML rules.

Cayman was now compliant or largely compliant with 39 of the 40 FATF recommended standards, he said, following the introduction of almost 20 pieces of legislation during the last two years.

This was confirmed by a CFATF follow-up report and technical re-rating of Cayman’s AML regime in February this year.

Two years ago, Cayman was only partially compliant with 13 technical FTAF criteria. After Cayman’s re-rating that number has dropped to one.

The CFATF report concluded that “Overall, Cayman Islands has made good progress in addressing the technical compliance deficiencies identified in its [mutual evaluation report in March 2019] and has been re-rated on 16 Recommendations.”

The only FATF rule that Cayman is only partially compliant with relates to virtual assets and is mainly due to the Virtual Asset Service Providers Act not having taken full effect yet.

The law was passed and already amended again last year to meet the international standard. Virtual asset service providers had to register with the regulator, the Cayman Islands Monetary Authority, by 31 Jan. 2021, the date at which the enforcement provisions of the law came into effect. However, other prudential supervisory aspects and licensing provisions of the law will only come into force in June 2021.

A look at a consolidated table of the assessment ratings of FATF members on the organisation’s website still shows Cayman’s results from two years ago. Responding to a question by the Cayman Compass, the FATF said it has yet to update the table.

Once the re-rating is taken into account, it turns out that the Cayman Islands is among the top five-rated jurisdictions with the highest technical compliance with FATF standards, ahead of the UK and well ahead of the US and other financial centres.

Paul Byles, whose consulting firm FTS regularly organises AML training events on island, said satisfying 60 of the 63 FATF recommended actions and being compliant or largely compliant with 39 of the 40 FATF recommendations is very good.

Paul Byles, whose consulting firm FTS regularly organises AML training events on island, said satisfying 60 of the 63 FATF recommended actions and being compliant or largely compliant with 39 of the 40 FATF recommendations is very good.

“The only regret is that the significant progress we have made over the past two decades in particular is not reported more widely by international media,” he said.

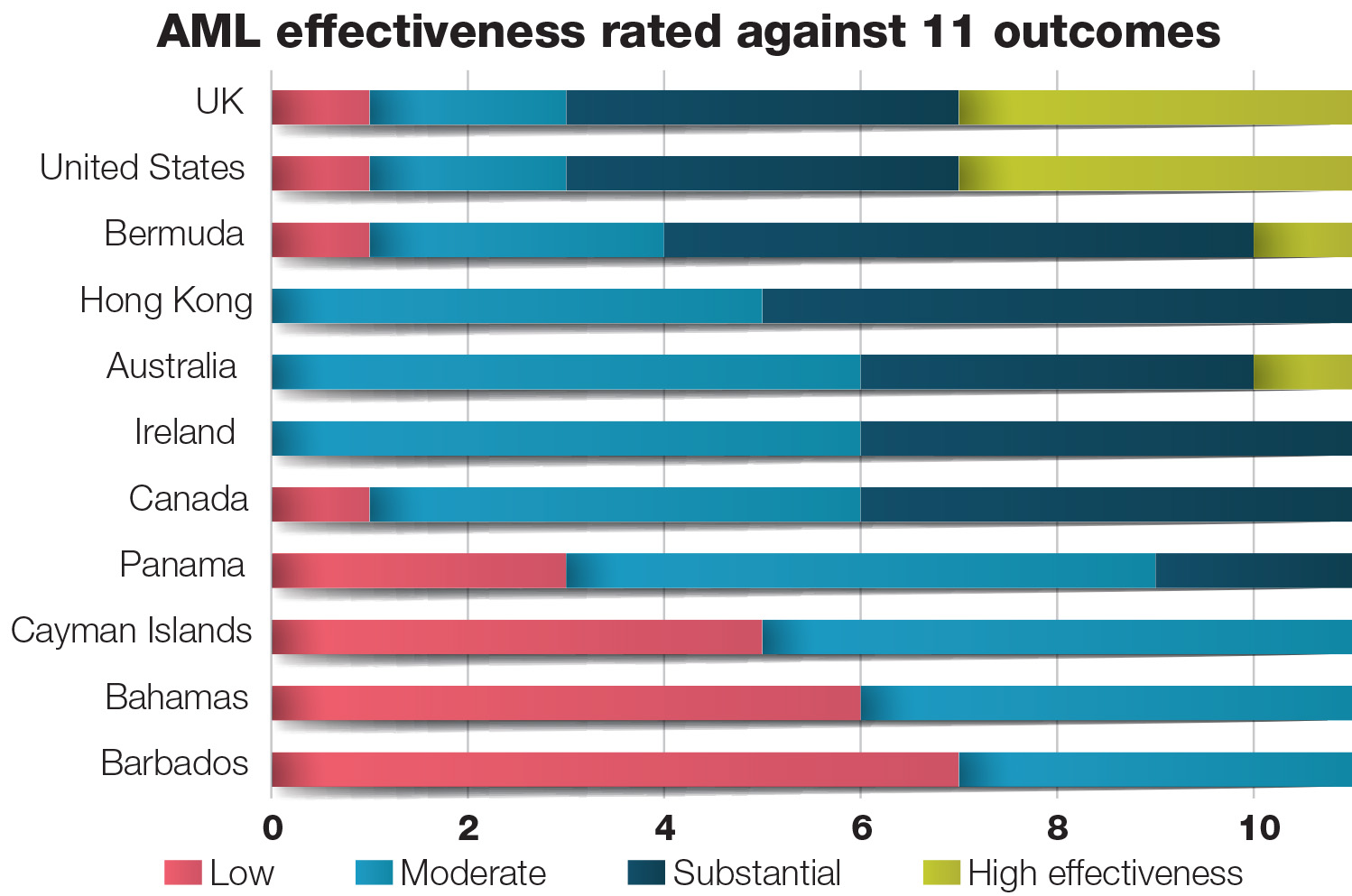

Practical effectiveness

The reason the Cayman Islands was still listed for increased monitoring is the perceived lack of practical effectiveness of the framework in certain areas.

Two years ago, Cayman’s AML framework was rated as having low or only moderate impact in relation to all 11 FATF effectiveness criteria.

To what extent this has changed is not entirely clear, because the latest CFATF report did not address any progress Cayman “may have made to improve its effectiveness”.

The CFATF wrote, the “Cayman Islands will remain in enhanced follow-up on the basis that it had a low or moderate level of effectiveness for 7 or more of the 11 effectiveness outcomes”.

The practical effectiveness of Cayman’s regime was rated by the Joint Group and the FATF Plenary based on the way Cayman responded to the 63 recommendations made by the mutual evaluation report. The results have not been made public.

However, given that only three recommendations have yet to be fully implemented and these inform only three effectiveness criteria, it raises the question whether the FATF is applying a different standard to the Cayman Islands.

The AML regimes in most countries are seen as only moderately effective, according to the FATF’s own criteria.

Across 104 countries and 11 effectiveness outcomes, fewer than 1.7% of ratings were deemed highly effective and only 21% were believed to have substantial effectiveness.

The remainder, more than 77%, were having either a moderate or low impact.

The FATF argues, however, that Cayman as a major financial centre should be held to a higher standard, in line with its larger anti-money laundering risks.

Despite their lower technical compliance in terms of laws and regulations, the UK, the US, or Switzerland, for example, are considered to have AML frameworks that are effective in more areas than Cayman’s.

James Kennedy, partner at law firm KSG said, “Whilst I disagree that the greylisting was necessary, of course the island has to take steps to show why this listing should be removed.”

The firm, which has a risk solutions arm that provides AML services, said in a press release the listing signals to others across the globe that transactions and business relationships with a customer, financial institution or company in Cayman may present a heightened risk of money laundering and terrorist financing.

Kennedy said inclusion on the watchlist does not mean each Cayman entity is high risk, but he anticipates heightened scrutiny for Cayman entities from regulator CIMA as a result.

Being subjected to increased monitoring also means that the Cayman Islands has identified the main strategic deficiencies and has given a commitment to address them within a certain time frame, said Byles. “I am sure the country will fully address the few remaining items within the next 12 months or so.”

Action plan

In its reasoning for the greylisting, the FATF specifically pointed to three of the 11 immediate outcomes as not being effective enough.

Government has agreed to an action plan that will focus on applying fines and enforcement actions for AML breaches and the failure to file accurate beneficial ownership information, as well as bringing more prosecutions for all forms of money laundering violations.

McLaughlin said that recent work by Cayman’s agencies substantiated the progress that has already been made in these areas.

This included the Registrar of Companies now imposing $5,000 fines against companies for not filing accurate beneficial ownership information.

The newly-founded Cayman Islands Bureau of Financial Investigations, meanwhile, has – since its inception in March of 2020 – secured court orders to freeze US$200 million for money laundering-related offences.

Enforcement has long been known to be the Achilles heel of Cayman’s AML regime. For a long time, financial supervisor CIMA could pull the licence of a regulated entity and declare directors not fit and proper, but the authority did not have the power to issue fines.

This has been remedied in the past two years, but the first financial penalties have only recently been handed down.

In November 2020, CIMA issued a $100,000 fine against Cainvest Bank and Trust for breaches of the Anti-Money Laundering Regulations.

The authority also fined Western International Trust Company $482,717.50 for AML offences in December 2020 and closed down Hinduja Bank & Trust Ltd for a range of failings include AML breaches.

However, it appears this was too little too late for the global standard-setter.

Related Videos

Excellent article.