In Cayman, we don’t get a vote at the Federal Reserve’s policy meetings, but we definitely feel the consequences.

In Cayman, we don’t get a vote at the Federal Reserve’s policy meetings, but we definitely feel the consequences.

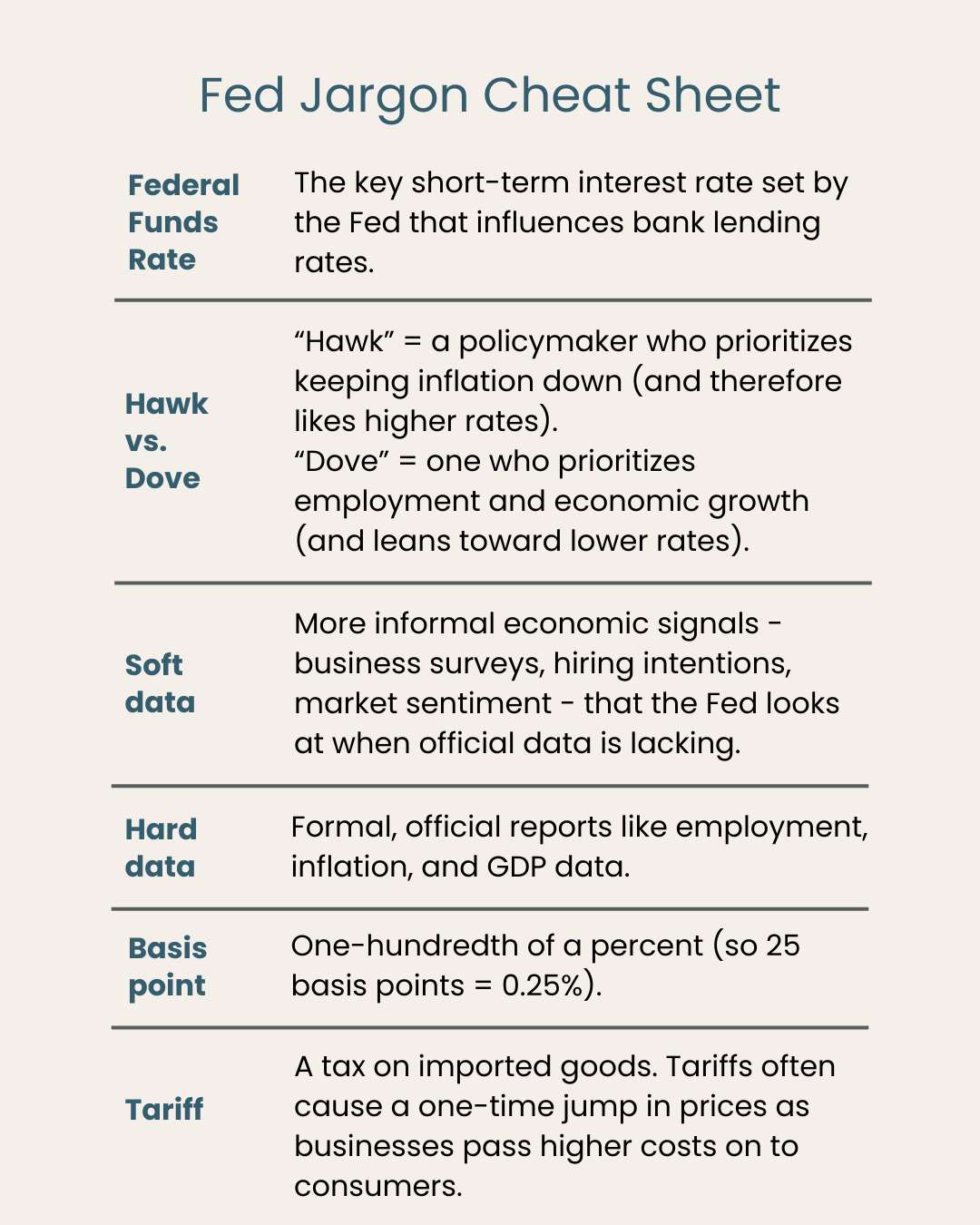

When the US Federal Reserve raises or cuts interest rates, the effects ripple far beyond Washington. Because the Cayman Islands dollar is pegged to the US dollar at a fixed rate, Cayman effectively imports US monetary policy. Local banks adjust their base lending rates – the foundation for mortgages, car loans, business financing and credit – based on what the Fed decides.

Interest rates sit at the centre of almost every financial choice. They influence the cost of borrowing, the return on savings, investment decisions and even the pace of economic growth. The Fed’s job is to balance two goals: keep inflation low and stable, while supporting maximum employment in the US. Lower rates stimulate growth but can fuel inflation; higher rates cool inflation but risk slowing the economy. It’s a constant, delicate balancing act.

The Fed’s upcoming 9 to 10 Dec. meeting is the final rate decision of the year and the one everyone is watching. What happens in Washington will influence our borrowing costs, our savings rates and the financial tone heading into 2026.

Why this December meeting is unusually foggy

The Fed usually begins each meeting with a full set of fresh data on jobs, wages, inflation and consumer spending. This time, the picture is incomplete. The recent US government shutdown delayed several key economic releases and the Bureau of Labor Statistics has confirmed that November’s jobs report will not be available until after the meeting. Policymakers will be working with information that is already months old.

Without timely ‘hard data’, the Fed must rely more heavily on ‘soft data.’ This includes business surveys, job-posting trends, wage trackers and consumer sentiment. These indicators offer useful signals, but they are not as precise, especially when two major policy developments are distorting the measures the Fed usually relies on.

Immigration policy is affecting the labour-supply backdrop. Recent estimates show that the United States’ foreign-born population has declined in 2025. Reduced immigration inflows and increased outflows mean that fewer new workers are entering the labour force. When the labour force grows more slowly, the economy needs fewer new jobs each month to keep the unemployment rate steady. Job growth that once looked weak may now be appropriate for a smaller labour force. With no fresh data, the Fed is trying to interpret this shift with limited clarity.

Another factor clouding the inflation policy is the US tariff policy. Tariffs introduced in 2025 have increased the cost of imported goods. Early evidence shows that some of these higher costs are beginning to reach consumers. It is expected that a tariff would result in a one-time jump in prices, something interest rate policy has very little impact on. Many businesses have absorbed the initial impact, which has limited the effect on consumers. As inventories turn over, more of the tariff costs are expected to show up in official inflation readings.

On top of these complications, the Fed itself is divided. Some policymakers – often called ‘hawks’ – want to keep policy tighter in order to guard against lingering inflation risks. Others – known as ‘doves’ – believe that the cooling labour market signals the need for modest easing. With the committee split and the data clouded, the December discussion is shaping up to be one of the most difficult of the year.

Markets, however, appear more convinced of their view. In mid-November, traders placed the odds of a December rate cut at about 40%. By late November, those odds climbed as high as 87%. This rapid shift shows how quickly expectations have changed, even if the Fed appears more cautious internally.

What the latest official data tells us and what it does not

The most recent complete set of official data covers September. It points to what many economists describe as “linear cooling.” In simple terms, the United States labour market is slowing in a steady and controlled way. Payrolls grew modestly, earlier months were revised lower, job gains were uneven across industries and wage growth softened. The unemployment rate moved slightly higher, but not in an alarming way.

Under normal conditions, this information would give the Fed a reasonably clear sense of direction. Today, it is not enough. With immigration shifts affecting labour supply, tariff changes influencing prices and no update from the November jobs report, the Fed is relying on a backward-looking snapshot to make a forward-looking decision.

What this means for Cayman households and businesses

Because of the KYD–USD peg, Cayman feels the effects of Fed decisions soon after they are made.

If the Fed cuts rates, then local borrowing rates typically fall soon after. This lowers the Cayman Prime Rate tied to mortgages, car loans and business financing. Anyone with a variable-rate loan will see monthly payments decline slightly, similar to the easing that we’ve seen over the last few months.

If the Fed holds steady, then borrowing costs stay where they are and households and businesses get no additional relief.

For savers, rate cuts result in lower returns. Money market funds, savings accounts and term deposits move in tandem with short-term US interest rates. When the Fed cuts, deposit rates usually decline shortly after.

So, the policy outcome matters differently depending on whether you’re a borrower or a saver. Many households are both, which makes the picture even more nuanced.

My take: the Fed will need to stay flexible

This meeting comes at a moment when the data is incomplete and the economic signals are mixed. The Fed must balance a weaker labour market with the potential for tariff-related price increases, all while interpreting trends that may look different once updated figures arrive.

For Cayman, the outcome will shape both borrowing costs and savings returns. As more reliable economic data becomes available later this month, the Fed will have a firmer foundation to guide its next steps and we will have a clearer view of what that means for financial conditions here at home.

Whether you’re managing a household budget, running a business, or planning your next financial step, the Fed’s December decision will help shape Cayman’s financial landscape for 2026.

Jessica Jablonowski, CFA is the Managing Director and Investment Advisor at Radix Financial Cayman, LLC.

Disclaimer: The views and opinions expressed in this article are my own and do not necessarily reflect those of Radix Financial Cayman. This article is for informational purposes only and should not be taken as financial advice. Radix accepts no liability for any actions taken based on the information presented here.

Related Videos