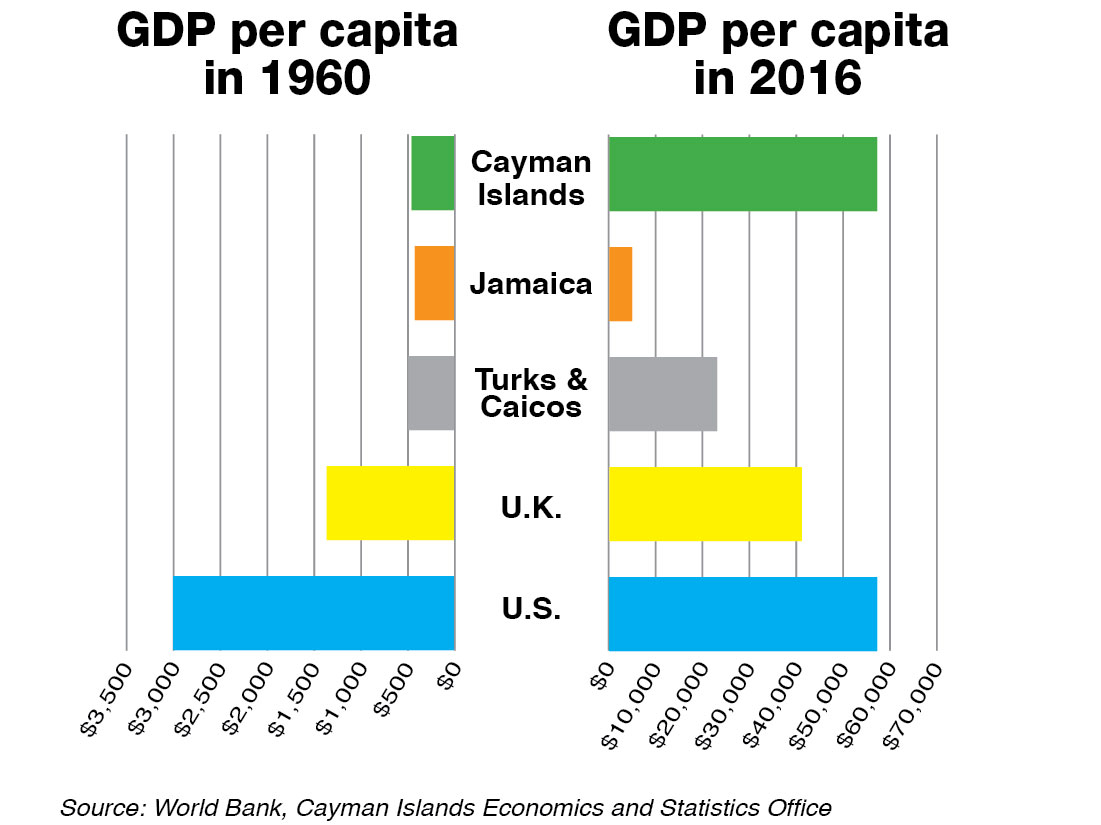

In 1960, the Cayman Islands could not have been further removed from its status today as a small but prominent global financial center. At the time, the Cayman economy still largely relied on seamen’s remittances, fishing, agriculture, shipbuilding and hand crafts. Airline services were limited and the tourism sector in its infancy.

Estimates vary but the economic output per person at the time was about US$450, more than Jamaica (US$430), about equal to the Turks and Caicos Islands but one-third the relative economic strength of the United Kingdom and one-seventh that of the United States.

More than a half-century later, the picture has changed dramatically. Cayman’s economic power, on a per person basis, now matches the U.S. and considerably exceeds that of the former motherland, the U.K., let alone that of other Caribbean nations and territories.

RELATED EDITORIAL: Paying homage to Cayman’s essential ‘invisible’ giant

The rise of financial services, which first led to the establishment of a large banking and trust sector, then the development of captive insurance and finally the growth of the hedge funds industry, shipping and aircraft registration as well as structured finance, is synonymous with the rise of Cayman’s economic prowess. It is known as the “Cayman Miracle.”

Yet, locally the attitude toward the industry is somewhat ambivalent.

Jobs, government revenue

Several years ago, an informal survey undertaken by Cayman Finance, the association representing Cayman’s financial services, showed the public believed (incorrectly) that tourism generated more economic activity for the country than financial services did and that at the same time (again, incorrectly) government spent more to support the financial industry than the tourism sector.

It is, thus, no surprise that when Minister of Financial Services Tara Rivers gave her budget address last year, she, in order to justify the spending of her ministry, chose to emphasize the seemingly obvious.

“The financial services industry is the primary driver of our economy. It is a primary contributor to GDP, the best way to measure our economy,” she said.

The finance industry, together with the related accounting and legal services sectors, contributed more than half (about 52 percent) of Cayman’s gross domestic product of $2.6 billion in 2015, according to the Economics and Statistics Office.

This did not include any indirect impact the industry has, for example, through clients and other interested parties attending meetings or conferences locally.

The notion that the financial services sector must still emphasize its size may in part be due to the proportionately smaller footprint of financial services in the labor market, compared to the sector’s economic impact. Still, a total of 7,669 people in Cayman work in financial services, accounting for more than 18.3 percent of employment, Ms. Rivers said, citing ESO statistics.

Crucially, far more than half of these jobs, 62 percent, are held by Caymanians. This is considerably higher than the 47 percent share of Caymanians in the labor force as a whole, as indicated by the latest available Labour Force Survey from the first quarter of 2017.

For government, the industry is an indispensable source of revenue with nearly half of all government funding (42 percent) coming from financial services contributions. This does not include items like stamp duties paid by individual businesses or people in the industry, which would bring the figures even higher.

Minister Rivers noted, this is the same revenue that is needed to pay for government services.

“There is absolutely no doubt that the financial services industry is critical to the socioeconomic welfare of the Cayman Islands,” she said. “It is critical for our ability to fund schools, to fund education, to fund healthcare, to fund social services, to fund road infrastructure, environmental conservation, etc.”

For Jude Scott, the CEO of Cayman Finance, the discrepancy between the perception of the industry locally and its importance for the economy, jobs and government revenue is in part due to statistical issues.

Current statistics are based on international categories which do not represent information in the same way financial services would be defined in Cayman.

“For example, when you look at financial services in the ESO statistics, it does not include the contributions of law firms and accounting firms, because they are included in the professional services category along with doctors, architects, etc.,” Mr. Scott said.

Once these categories are aggregated, it becomes clear that the industry is a substantial employer, especially for Caymanians.

Financial services vs. tourism

Mr. Scott says there are several other reasons why the vital role of the industry for the economy, the labor market and government revenue is not well understood by the general public.

“One reason is if you are using intellect to add value, it is not something so physical and tangible. In tourism, you have tourists coming off an airplane, eating in restaurants and in hotels. That gives us a sense of the industry. If you look at the construction industry, you physically see something being built,” Mr. Scott said. “One of the things that we recognize, because of the nature of the work that we do, it is important for us to create a visualization around it.”

Another reason the work the industry is doing is not so obvious, he added, is that much of the work is done with counterparties around the world: “That is not directly impacting the person on the street.”

Financial services in Cayman are also made up of multiple, often independent industries like investment funds, asset management, banking, insurance, reinsurance, capital markets and fiduciary services.

Cayman Finance itself now represents 15 industry associations and has set as one of its goals bringing them together “so you see it and feel it as one industry.”

There has also been, from the political perspective, a disproportionate focus on tourism.

“I am obviously a big advocate for tourism, in particular stay-over tourism, which adds tremendous value to the jurisdiction,” said Mr. Scott, who was previously chairman of Cayman Airways and sat on the ministerial council for tourism and development.

But he noted that government has released a lot more information in support of expenditures on tourism than in support of the financial industry.

“That sends an inaccurate signal to the community to the importance in relative terms,” he said.

This prompted Cayman Finance to conduct its own analysis, which, based on aggregated Economics and Statistics Office data, found that the industry employs 4,000 Caymanians and contributes more than $300 million a year to government revenues.

Based on the limited information, the association pulled together different elements that contribute to supporting the tourism and financial services industry, such as regulation, legislation, policy development, marketing and business development.

“We were able to show government that they spend twice as much on tourism as they do on financial services. And for every dollar they spend on financial services, they roughly receive around $18 from financial services. Comparably with tourism, they receive less than $2 in revenue,” Mr. Scott said.

The invisible giant

As part of the value equation, the industry is also a large purchaser of services in the jurisdiction. An analysis by Dart and the developers of Cricket Square showed that financial services tenants occupied 90 percent of the office space at Camana Bay and 80 percent at Cricket Square.

This strong impact on local developers and property companies remains largely unattributed to the financial sector, Mr. Scott said.

“When you see a new commercial office building going up at Camana Bay or Cricket Square or similar locations, we would count that as construction GDP. The worker who is there has a construction job. [But] the demand for that is created by the financial services industry. If we did not have the industry, we would not need the building, we would not have the job,” he said.

Other indirect effects, on professional support services such as marketing and public relations, various forms of retail, or restaurants are difficult to determine but likely to be very significant.

In fact, the financial services industry is so entangled into the local economy that its success and support of the heightened lifestyle locally can easily be taken for granted and belies the fragility of Cayman’s development during the past five decades.

For an industry that represents more than half of the economy, for example, an 8 percent decline, as discussed recently as the potential fallout from an EU tax blacklisting, would translate into a 4 percent decline for the economy as a whole. In other words, a significant downturn in the financial services sector would almost certainly plunge the entire country into an economic recession.

However, regulatory pressures are nothing new and Cayman’s financial industry always had to continuously innovate, not only to respond effectively to the evolution of the international regulatory regime, but also to changing client demands. Texas A&M University law professor Andrew Morriss, an expert in regulatory competition, said it was this ability, underpinned by Cayman’s social and constitutional stability, which sustained collaborative policymaking, that was responsible for its success.

Together with Tony Freyer, Mr. Morriss is the co-author of the paper, “Creating Cayman as an Offshore Financial Center: Structure & Strategy since 1960.”

He agrees that the tourism sector, with tourists on the street, cruise ships in the port and hotels along Seven Mile Beach, is simply much more visible than the financial services industry.

Government’s fiscal support of tourism is also often directed into general infrastructure projects, such as airports, roads and cruise ship facilities, that are much more noticeable to the general public than government ministers heading for talks to London or the crafting of new legislation.

Mr. Morriss also noted that the same applies to the media coverage of both industries, which in the case of tourism will be more tangible in terms of tourists coming to the island, new airline connections and development projects than financial statistics or regulatory initiatives.

No ‘Cayman Miracle’?

Given the different trajectories of Caribbean countries since the 1950s, an interesting question arises, “Where would Cayman be today without the financial services industry?”

Mr. Scott believes Cayman could have been successful “in any number of industries that use high service industry skills combined with smart people coming together and creating innovation.” The question, he said, is how soon those industries might have developed.

Cayman has always been a very entrepreneurial jurisdiction and through its history developed a sense of being a global citizen. As a jurisdiction, Cayman positioned itself early on to take advantage of multiple paths, Mr. Scott said. First, seafarers had to compete in this space, then it was local industries through turtle, coconut or rope exports.

“So, in terms of business perspective, quality of service and business opportunities that can be pursued, it is looked at from a global perspective. It is not limited to what we see in the region.

“In our case, what ended up being our path was financial services. The original building block of that was the banking industry. From the banking industry, we built the captive insurance industry, the trust and private client business, the capital markets business, hedge funds. We are now building out the governance offering for the jurisdiction using similar types of qualities and innovation.”

Mr. Morriss believes, without financial services, Cayman would look a lot like the Turks and Caicos Islands.

“Both were about at the same level of development around 1970, and the big difference is that Cayman’s financial industry took off and Turks’ didn’t, leaving it with tourism,” he said.

While he acknowledged the qualities that made Cayman successful in financial services, he said the problem is determining where Cayman would have had a competitive advantage: “Cayman does not have a big labor force, cheap labor, low transportation costs, a naturally advantageous position geographically for being a transit point, cheap utilities, a great natural harbor, etc. Besides tourism, it’s hard to see what else could have developed – especially in the 1970s to 1990s.”

During his research, Mr. Morriss unearthed documents in the British Archives from the 1960s and early 1970s from the Foreign and Commonwealth Office which asked what the overseas territories that were turning into financial centers could do besides offshore finance.

He said, “To some extent, the response was ‘not much other than tourism’ and that’s part of what led the FCO to be able to win against the U.K. Treasury complaints about leakages in tax and sterling that the development of offshore financial centers in overseas territories and Crown dependencies were causing.”

Future challenges, opportunities

Now that Cayman has pursued the financial services path, its position is continuously threatened, be it through regulatory initiatives elsewhere or changing services and client needs. But Mr. Scott said he does not lose sleep over that.

“Because when I look at financial services and the offerings that we have from Cayman, we have been very specific at what we developed. When we really define those at the core level, we are providing a very efficient, trusted, neutral platform for legitimate parties who have capital and financing to connect with parties who need capital and financing around the world,” he said.

“So as long as the world needs capital and financing, someone, somewhere has to provide the service.”

Cayman’s qualities, in terms of global outlook and quality of service, have allowed the jurisdiction to remain innovative.

Mr. Scott believes that globally, technology is going to play a huge role in redefining financial services transactions. As a result, services are not constrained by geography anymore and can be provided from anywhere in the world.

“To have a high impact now, you have to have upscaled, been innovative and cutting edge. Again, this works well with the skill sets that we have in Cayman,” he said.

“When we look at capital and financing being needed in the world more now than ever, we have continued to evolve our product offering, our global standards, transparency and cooperation to make sure that we are meeting the needs of the world and upholding the standards,” Mr. Scott said.

“We provide a very valuable role and there will continue to be a place for us.”

Related Videos

It must be pointed out that Gross Domestic Product (GDP) is an asinine measure of economic activity. It provides a macro snapshot of the countries output, but says nothing about the micro income of a citizen.

The OECD defines GDP as “an aggregate measure of production equal to the sum of the gross values added of all resident and institutional units engaged in production (plus any taxes, and minus any subsidies, on products not included in the value of their outputs.

GDP does not account for variances in incomes of various demographic groups. Furthermore, many environmentalists argue that GDP is a poor measure of social progress because it does not take into account harm to the environment.

Imagine if you will, the British Virgin Islands in the aftermath of Hurricane Irma in September 2017, an island on which Sir Richard Branson is resident, and ask yourself how the territory’s GDP was affected? Ask also how funding for disaster recovery skewed by the amazingly high GDP.

Nicholas Robson

The Climate War Room