Legislators voted unanimously last week to allow workers to access $10,000, as well as 25% of the funds in excess of that amount, from their pension accounts. Amendments to the Pension Law also open up the possibility of a six-month pension holiday for employees and employers.

Legislators voted unanimously last week to allow workers to access $10,000, as well as 25% of the funds in excess of that amount, from their pension accounts. Amendments to the Pension Law also open up the possibility of a six-month pension holiday for employees and employers.

However, there is concern that taking money from pension funds is not the best solution to counter people’s loss of income.

According to Premier Alden McLaughlin, the move was needed to help businesses and employees during the coronavirus health and economic crisis.

Those who have just lost their jobs and who are desperate to pay for their home and basic necessities tend to welcome the ability to access their retirement savings.

While there is agreement that some form of support is needed for those who are suffering financially as a result of the lockdown to suppress the spread of coronavirus, not everyone is convinced that pension savings should be the source of those funds.

Billy Adam, a former National Pensions Board member, says COVID-19 is a national, rather than a personal, issue that government should address in an non-discriminatory and fair manner.

Instead, he said, “Government is unfairly taking advantage of our vulnerable people in a time of great need by requiring some to decimate their personal pension funds.”

He said it was grossly unfair and discriminatory for government to wrongly put pressure on some people, usually the most disadvantaged and unrepresented, to sacrifice their retirement income replacement funds, when government is at the same time paying funds from general revenue to assist certain other categories of workers.

Both groups of people will pay future taxes to repay government, but those who lose their pension funds will either have to make higher future pension contributions, work beyond the normal retirement age, or require government assistance in their old age after retirement, Adam said.

Current pension contributions of 10% of salaries, half of which is paid by the employer, are in many cases already considered too low to provide sufficient retirement income. Because, on average, people live much longer in retirement than in the past and investment returns are sometimes not as high as expected, the danger of old-age poverty is increasing, not only in Cayman but worldwide.

Government is fully aware of this. During the debate on the Pension Law amendment, McLaughlin warned savers, “If you do not need it, do not take it.” He said there was going be life after COVID-19. “People are going to live and get to retirement again and, indeed, they will need something to rely on when they get there,” he said.

The pension withdrawal will also affect the pension plans and other plan members. The fact that the fixed costs of operating a pension plan, such as rent and salaries, remain, while the funds under management decline, means that the relative cost to run a fund will increase for everyone.

“With less funds in the plan, the cost of the plan to each member will increase, thus disadvantaging every member,” said Paul Schreiner, chairman of the board of trustees of the Chamber Pension Plan.

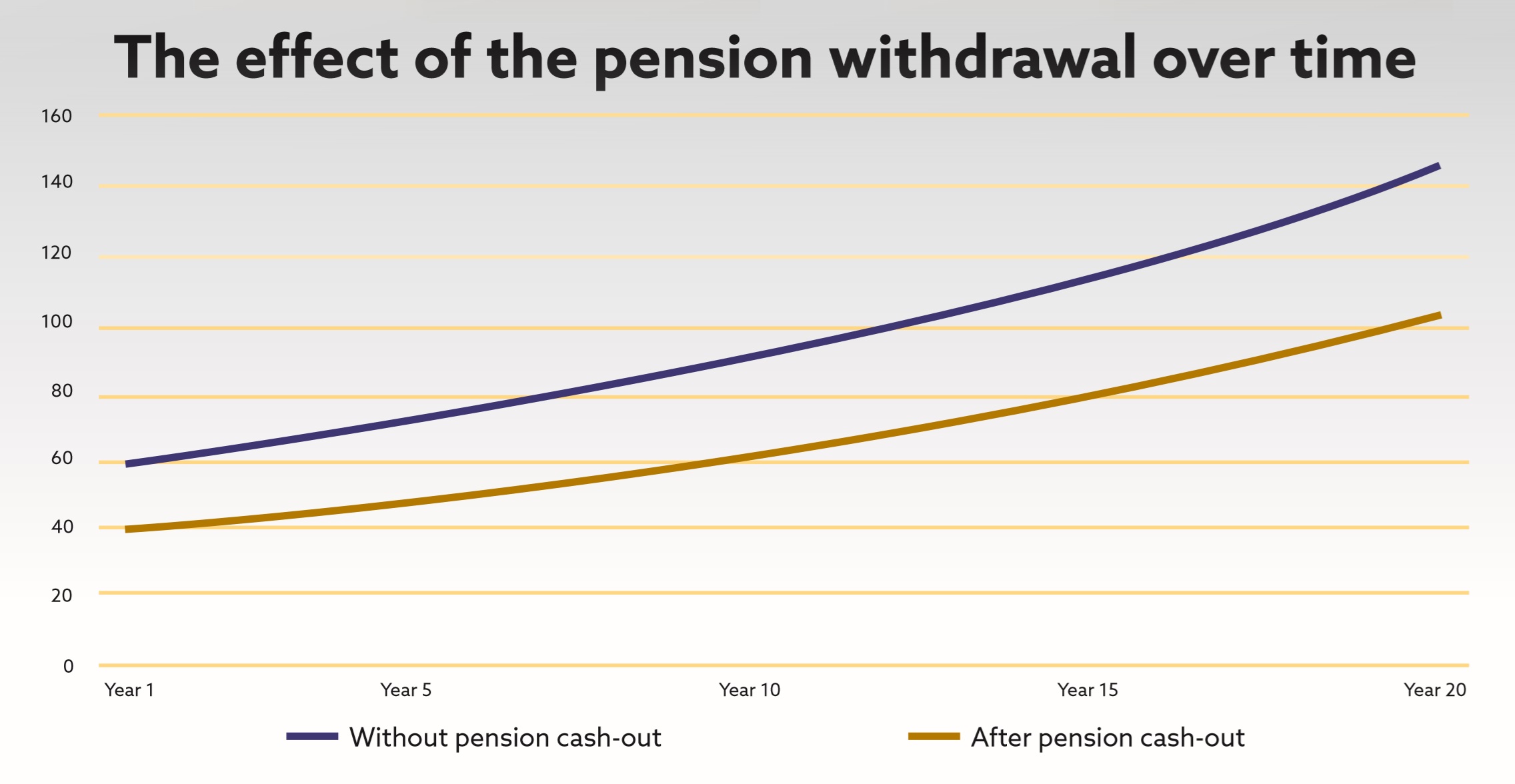

In addition, anyone who withdraws a portion of the retirement savings is inevitably going to hurt their retirement funds. The effect of compound interest on savings over the years is so high that it is almost impossible to recover the funds that were cashed out and any related future investment gains.

“Their retirement payouts will be significantly lower and will never recover,” Schreiner said.

The timing also could not be worse for any retirement savings withdrawal shortly after a massive financial market decline. Global stock markets, which crashed by 30% or more in February, have started to claw their way back since mid-March.

“This is definitely a bad time to cash out your pensions,” Schreiner said. “Members will be selling at a point which is considerably lower. Selling low is always a bad idea.”

The Chamber Pension Plan administrators hope that members only take out funds if they lost their jobs and need the funds for rent, groceries and other necessities, Schreiner added. “The plan believes taking the funds out for any other reason is a terrible decision.”

However, there is the concern that many savers will take advantage of the pension cash-out, even if they are not in financial difficulty. This would spread the negative effect of the pension withdrawal much more broadly across all savers.

The Chamber plan administrators believe lawmakers should have limited the ability to apply for and receive money from pension funds only to those who have lost their jobs.

Schreiner said the pension cash-out will put members at a huge retirement disadvantage. Ultimately, it would cost government more money if retirees have to apply for social services as a result of the withdrawal.

Related Videos

This is a well written article and speaks directly to the point that taking money early from a pension or other retirement plan is not in anyone’s best interest. As stated in the article, “The pension withdrawal will also affect the pension plans and other plan members. The fact that the fixed costs of operating a pension plan, such as rent and salaries, remain, while the funds under management decline, means that the relative cost to run a fund will increase for everyone.

“With less funds in the plan, the cost of the plan to each member will increase, thus disadvantaging every member,” said Paul Schreiner, chairman of the board of trustees of the Chamber Pension Plan.”

Everyone is hurt by this and those that are at the low end of the savings scale are those that are most hurt. It will cost more to support these people when they get older and not able to provide for themselves.

One major step that I have not seen taken in Cayman is to substantially reduce import duties and tariffs on all essential items such as food, drink (except alcohol, power drinks, etc.) medicine, fuel used for generating electricity, fuel for delivery and other vehicles, personal necessity items, and so forth. This will have a greater effect on the cost of goods people have to buy and substantially reduce the outflow of cash for the middle and lower income levels. Cayman has a budget surplus so the impact will be minimal until the economy kicks in again. When the Cayman economy kicks into gear again the duties and tariffs can be gradually raised back to normal levels.

If you really have the Caymanian people’s best interest at heart, the government should find ways to increase the cost of living for non-Caymanians who have multiple homes in various world regions. They have the incomes to better weather this storm without major impact to their “retirement” savings. People can live a comfortable life with $5 million plus in the bank or investments. It is the Caymanian who has not been as fortunate with only a few thousand or hundred thousand in savings that is being hurt by wiping out their retirement savings during this pandemic.