Coronavirus delivered a major blow to economies, businesses and livelihoods around the world, whilst also resulting in one of the shortest global recessions. In the US, the 2020 recession was one of the worst since the Great Depression. A month into the pandemic, it was already worse than the 2008 recession in its initial viciousness.

Coronavirus delivered a major blow to economies, businesses and livelihoods around the world, whilst also resulting in one of the shortest global recessions. In the US, the 2020 recession was one of the worst since the Great Depression. A month into the pandemic, it was already worse than the 2008 recession in its initial viciousness.

By November 2020, however, global stock markets had recovered, and job numbers were recovering across developed markets. As of today, the US and most other major economies are already progressing toward the mid-cycle phase of expansion as businesses reopen in the midst of aggressive vaccine rollouts.

For context, the National Bureau of Economic Research (NBER), an American private nonprofit research organisation, committed to undertaking and disseminating unbiased economic research – also popularly known as the Business Cycle Dating Committee – has determined that a peak in monthly economic activity occurred in the US economy in February 2020. That peak marked the end of the expansion that had begun in June 2009 and was followed by the beginning of the COVID-19-induced recession. NBER has defined 11 cycles from 1945 to 2009, with each cycle lasting on average five-and-a-half years.

A good understanding of the business cycle is of paramount importance to investors as this usually helps to inform what strategies to pursue, traditionally choosing between growth (defensive) and value (cyclical) stocks. Using the US economy as a proxy of how global economic conditions changed so rapidly, it contracted 5% in the first quarter of 2020, then contracted a record 31.4% in the second quarter. The economy did bounce back and grew 33.4% in the third quarter of the same year. In the fourth quarter, the economy grew by just 4%. According to the World Bank, the US economy is expected to grow by 6.8% in 2021, whilst the global economy is expected to grow by 5.6% – the fastest post-recession pace in 80 years. This is largely due to strong rebounds from other major economies.

Historically, growth and value stocks have taken turns leading and lagging one another along the business cycles as market and economic conditions continuously change. The speed at which these conditions have changed since February 2020 has been unprecedented. This has created swings in market performance between growth and value stocks, leaving the question as to how investors should position themselves going forward unanswered, i.e., growth, value or rather a quality, hybrid approach?

Since March 2020, markets were largely driven by more defensive growth sectors, such as the large technology companies, until positive news of COVID-19 vaccines broke out in the second week of November 2020. That is when markets switched from growth stocks to value (cyclical) stocks, which are more exposed to the economic recovery. This dynamic continued through to the end of May 2021, after which value stocks lagged again in June 2021 as growth stocks rebound. These swings have created challenges for investors as to how to position their portfolios going forward. A good understanding and perfect timing of the business cycle will be instrumental at this juncture.

Since March 2020, markets were largely driven by more defensive growth sectors, such as the large technology companies, until positive news of COVID-19 vaccines broke out in the second week of November 2020. That is when markets switched from growth stocks to value (cyclical) stocks, which are more exposed to the economic recovery. This dynamic continued through to the end of May 2021, after which value stocks lagged again in June 2021 as growth stocks rebound. These swings have created challenges for investors as to how to position their portfolios going forward. A good understanding and perfect timing of the business cycle will be instrumental at this juncture.

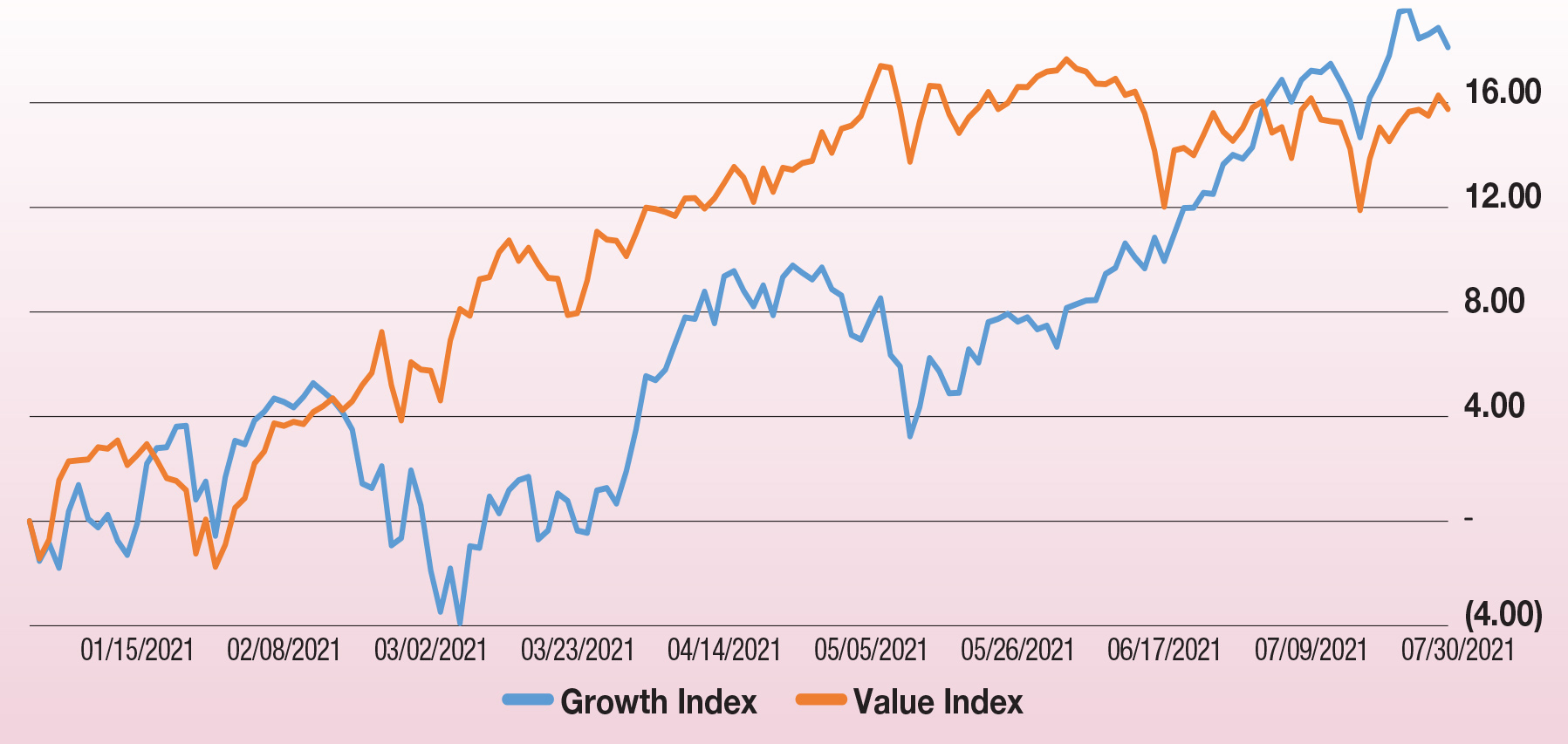

From the start of the year through to end of May, investor fervour for value was pronounced, with the S&P 500 Value index outpacing the S&P 500 Growth index. This performance of value versus growth reflected the rise in US Treasury yields during the same period. A significant reversal occurred, however, during the last six weeks of the quarter. This was concurrent with the decline in Treasury yields as the Growth index regained the lead. The above graph illustrates the performance between the two indices.

Most investors characterise Warren Buffett, the American business magnate, investor, and philanthropist, as a value investor based on his investment philosophy of only investing in companies that he fully understands and expects their share prices to recover, and those with usually low price-to-earnings or market-to-book ratios. As an extension, value stocks are often stocks of cyclical industries, which may do well early in an economic recovery but are typically more likely to lag in a sustained bull market. Growth stocks have the potential to perform better when interest rates are falling and company earnings are rising.

With the continued swings between value and growth stocks, beating the market may be hard to achieve for long-term investors, as the tilts may continue to offset overall performance. While the cheaper energy and financial stocks may still be attractive based on value, it is important to understand the business cycle to avoid a potential trap. On the other hand, valuations for growth stocks seems overstretched in general based on multiples.

Investors may want to consider a hybrid of the two approaches, i.e., the quality investing approach. This approach allows investors to, in theory, gain throughout economic cycles in which the general market situations favour either the growth or value investing style, smoothing any returns over time. Essentially, this strategy does not try to time the market cycles. It focusses on clearly defined fundamental criteria that seeks to identify companies with outstanding quality characteristics, including management credibility and balance sheet stability. Historically, quality outperforms more as the cycle progresses and tends to outperform the broader market overall. As the initial V-shaped recovery fades in momentum, along with the cycle maturing, quality may be the next winner.

Overall, the decision to invest in growth, value or quality stocks is ultimately one to be considered uniquely for each investor. It should be based on an individual investor’s preference, as well as their personal risk tolerance, investment goals and time horizon. As demonstrated in this article, over shorter periods, the performance of either growth or value stocks will largely depend on where the economic cycle is at that particular point in time.

Sources: National Bureau of Economic Research, Worldbank.org, Bloomberg

Richard Maparura, CFA, Senior Portfolio Manager, Asset Management, Butterfield Bank (Cayman) Limited

Disclaimer: The views expressed are the opinions of the writer and whilst believed reliable may differ from the views of Butterfield Bank (Cayman) Limited. The Bank accepts no liability for errors or actions taken on the basis of this information.

Related Videos

Pardon but growth stocks are not a defensive strategy but a cyclical one, as they boom with expansion and drop with contraction. Value stocks are a defensive strategy as they typically do okay in an expansion but hold up better at the end of an expansion or contraction as they are also buttressed by higher dividends.