Government plans to take on US$400 million of new debt have sparked debate and controversy in the past month.

Finance Minister Chris Saunders argues he is simply seeking to take advantage of favourable interest rates, to solidify Cayman’s long-term financial position and fund infrastructure projects, while continuing to support those in need amid COVID’s impact.

The Opposition has accused him of saddling the country with significant, unnecessary debt to fund budget giveaways and avoid making difficult political decisions.

The debt package government is contemplating – a $400 million 30-year bullet bond – could potentially replace currently-existing bank loans and available loan facilities.

Government borrowing is not inherently bad, says Caribbean economist Marla Dukharan. But she cautions it is a decision that should not be taken lightly in these “uncertain times” and advises Cayman not to fall into the “debt trap” that has plagued many countries in the region.

This week, Saunders defended the plans in a statement and video message.

The finance minister said the consideration of a $400 million 30-year bullet bond was just one option to restructure government’s debt and would offer more flexibility to address Cayman’s growing welfare costs.

He said the potential bond issue was no departure from government’s previously-expressed intention to refinance public debt and fund capital projects.

“Nothing more. It has absolutely nothing to do with borrowing to fund the government’s day-to-day expenses or the creation of a welfare state as claimed,” he said.

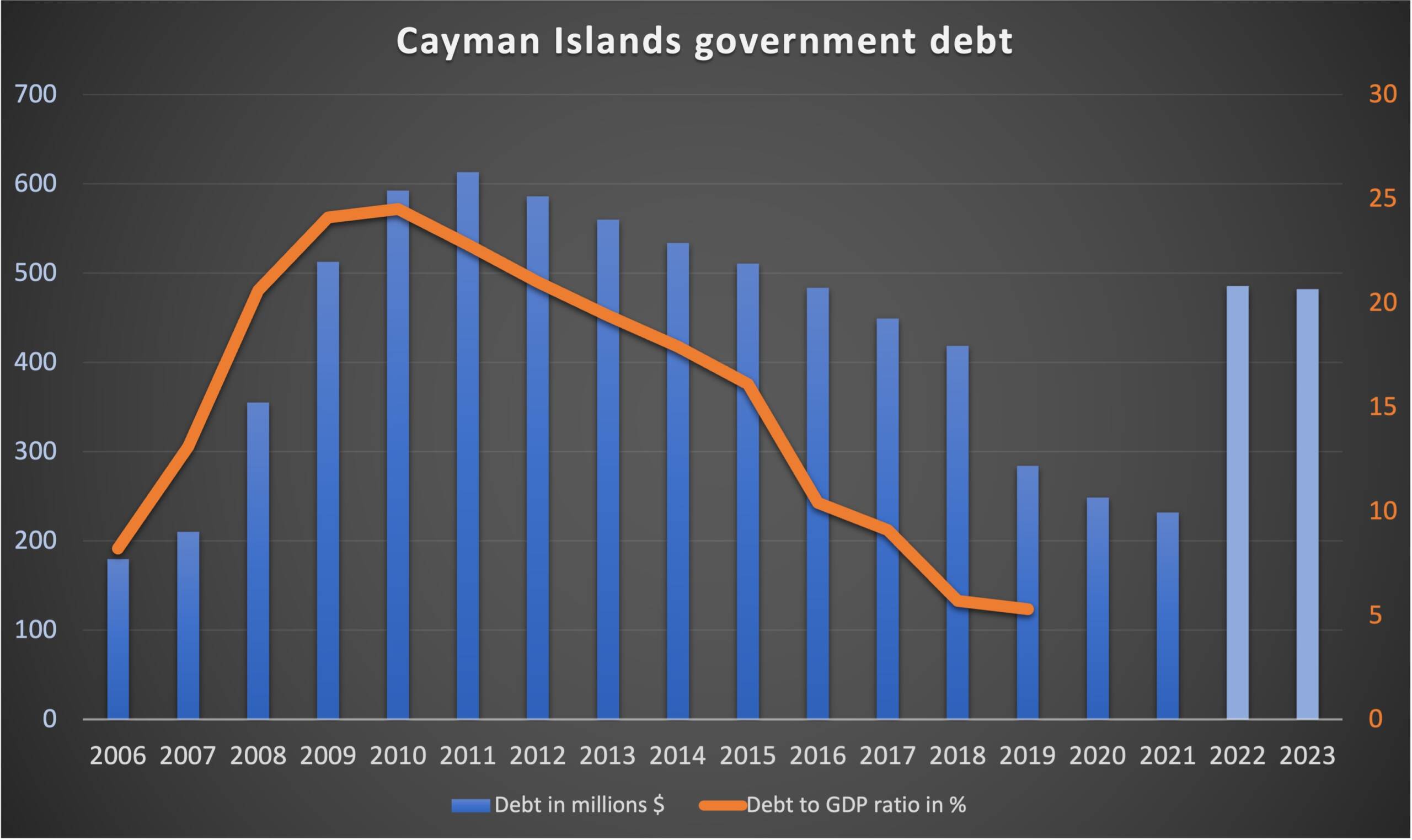

When adopting the two-year budget in December, the PACT government announced it would raise up to $350 million in new debt over the budget period. Government’s total debt is set to rise from $232 million in 2021, held in loans from several local banks, to about $485 million in 2022 and 2023.

Debt-funded infrastructure and services

The finance minister said the borrowed funds would pay for “vital infrastructure projects” such as the completion of the long-term mental health facility, the East-West Arterial and other new roads, a new undersea data cable and school construction projects.

Funds would also be used to finance “equity injections” for “vital public services” like the Health Services Authority or Cayman Airways.

Equity injection is an accounting term for the government-funding of public entities that are unable to pay for all their expenditures from their own revenues.

Saunders said $28million of new debt was also earmarked to help prop up the National Housing Development Trust and the Cayman Islands Development Bank to support Caymanian homeownership.

This could include the government underwriting loans above 30 years to young borrowers, at affordable repayment terms, until they can access funding from traditional banks.

Reverse mortgage scheme

In addition, the finance minister raised a new idea that was not previously mentioned in the budget.

Claiming the former government had done nothing to address rising social welfare costs, he said he intends to address the problem with a reverse mortgage scheme.

This would provide funding to enable elderly homeowners “to use the equity in their homes to support themselves now in their time of need”.

The explicit aim was to reduce social assistance pay-outs to the elderly.

“It is not fair or sustainable for the government to be assisting the elderly when they are equity-rich but cash poor. Letting our seniors access their cash when they need it now, means they can live in dignity without being a strain on the public purse,” Saunders said.

In response to Opposition criticism of plans to raise new debt, the finance minister said, “many public servants would like to know which of their services the opposition values the least and that we should cut”.

‘No restraint’

In an interview with the Cayman Compass, the Leader of the Opposition Roy McTaggart acknowledged that, had the Progressives stayed in power, some of government’s capital projects would potentially have had to be funded by debt.

But the former finance minister said, “I certainly wouldn’t be borrowing to the level that they are borrowing.”

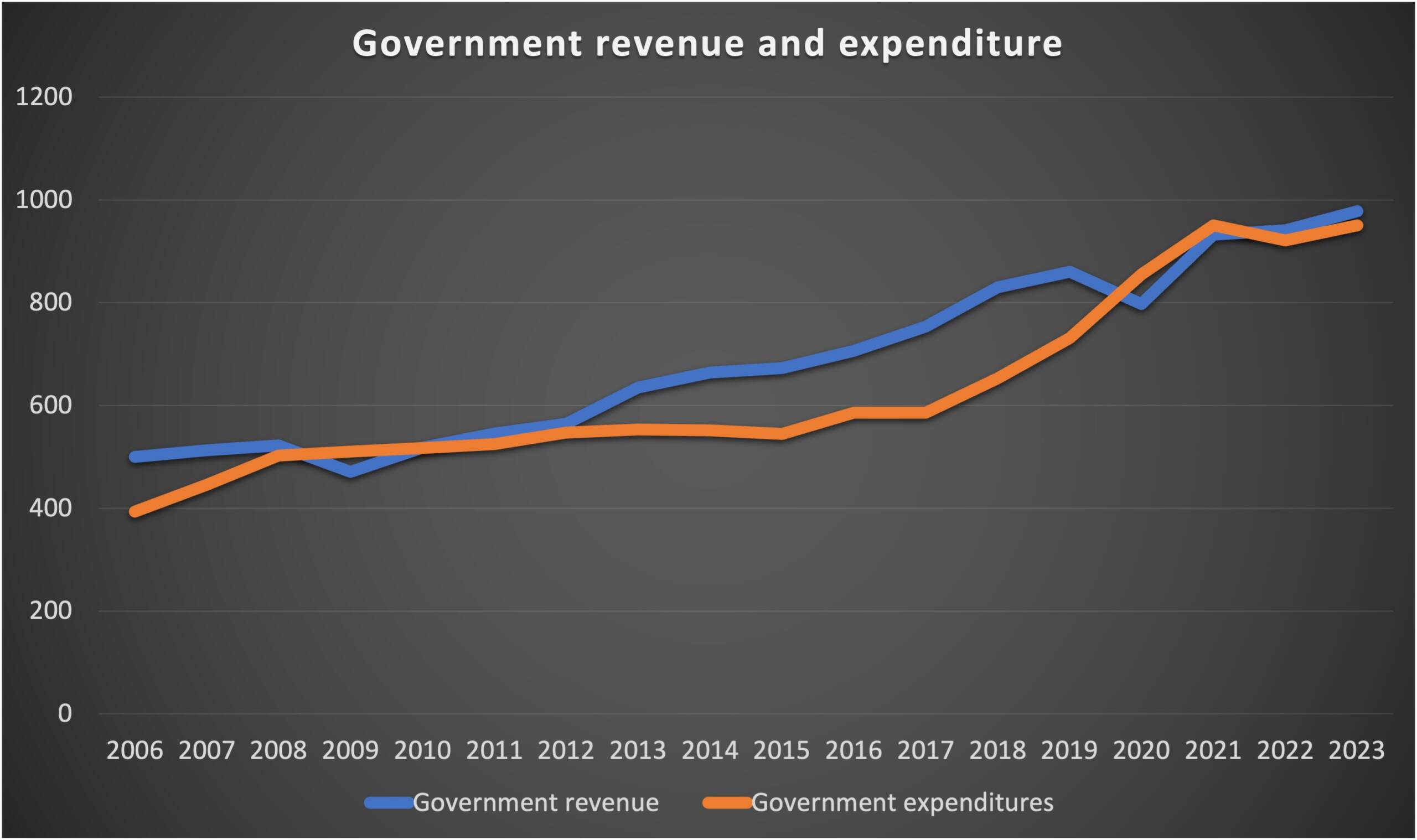

In recent terms, government was able to fund 100% of capital expenditures from revenue, because of large budget surpluses. “The [PACT government] have now gone from that to funding 100% of it by debt,” he said.

McTaggart claimed that, under the new government, there is no restraint in spending and no tightening of purse strings, despite the pandemic and its impact on the economy.

“You look at what each ministry, each minister is getting out of this budget. Everybody’s getting whatever they want.”

The Opposition leader said the timing of the spending was also crucial and could be critical to smooth out spending patterns so that government can afford what it pays for, rather than resort to borrowing.

McTaggart believes that government also has cash reserves available and an emergency line of credit that is largely untouched.

He said, there are “substantial sums available to the government without having to resort to such long-term borrowing”.

Government’s cash reserves

According to government’s financial position in December, government had about $304 million in cash and term deposits in 2021. This was down from $448 million in 2020.

For 2022, government projects to have about $404 million in cash and term deposits, presumably as a result of additional debt, with lower cash reserves of $312 million in 2023.

Under the Public Finance Management Act, unrestricted cash reserves should at their lowest point in the year be sufficient to fund 90 days of government’s estimated operating expenditure.

In the budget, government expects that its reserves should last for 137.9 days of operating expenditure in 2022 and just 95.9 days in 2023.

Should Cayman borrow now?

Economist Marla Dukharan told the Compass that “Cayman can afford to borrow now if it truly needs to in these perilous and uncertain times.”

But whether such borrowing makes sense at this time, she added, depends on whether the borrowing is truly needed, what the borrowed funds are spent on, and on the terms and conditions of the borrowing.

“These are very uncertain times and raising debt should not be taken lightly, even when your debt-to-GDP ratio is below 10% – because GDP can shrink quickly, and that ratio can become 30% in short order,” she said.

The economist from Trinidad, who is based in Barbados, has, in the past, praised Cayman as the best-run economy in the Caribbean region, because it employed a counter-cyclical fiscal policy.

“Simply put – in times of plenty, you save, and in lean times you draw on those reserves to spend, in order to maintain a smooth, stable level of spending over time,” she explained.

Dukharan is not against borrowing per se. In fact, she has argued that, up to a certain level, government debt can make a positive contribution to economic growth. The big caveat is that the money must be spent wisely.

She said, “A country in Cayman’s position could benefit in the long term from borrowing if it did not have the funds to finance those important and necessary expenditure items, and once the terms and conditions of the borrowing make sense relative to the project it is financing.”

Dukharan raised the question as to whether government can fund projects from reserves and if the return on the projects would justify any borrowing.

In light of the projects mentioned by the finance minister, that is the big ‘if’.

Dukharan said these are important questions for government to consider before taking a decision to borrow, at any time and on any terms.

“The last thing we would want to see is Cayman fall into the debt trap that most of the Caribbean is already in,” she said.

“On the other hand, if there are opportunities for justified, bankable projects that will support long-term growth and socio-economic development, now may be the right time to consider them.”

Refinancing

Saunders said government is now investigating refinancing options to take advantage of the low interest rate environment. This will include, among other things, a bond offering “to ensure we are paying less interest every year and to invest in our Islands’ long-term future”.

He accused the Opposition leader of hypocrisy for criticising the debt plans, saying that when McTaggart was finance minister in September 2020 he secured “a US$403 million line of credit at a rate of 3.25% that expires in June of this year.”

At the time, in the midst of the COVID pandemic and the economic fallout resulting from it, McTaggart said the credit line would give whoever is occupying Cabinet in 2021 the authority to borrow money, “if it becomes necessary”.

However, the line of credit has not been drawn down, except for US$19 million that was required under the terms of the agreement.

Government must decide whether to draw down another US$357 million tranche under the facility and convert it into a 15-year loan by 30 June.

McTaggart believes government has not shown the need to borrow that much money now – and for such a long time – if it did, indeed, opt for a 30-year bond issue instead.

He asserts that government could still borrow three or four years from now. Even if interest rates were going to be a bit higher, government would still be able to access market rates as and when it needs to.

“I just have not seen them demonstrate the need to have to go to that extent of borrowing, and certainly not for that length of time,” he said.

Saunders, in turn, argues that the $403 million bond issue could simply replace, at preferential terms, the already arranged $403 million loan facility that, if not drawn down, will no longer be available after the summer.

He said it would be prudent for government to look for ways to save government money, for instance by securing lower interest rates for its debt.

He noted that in September of last year, the Isle of Man, which has a similar credit rating as the Cayman Islands, secured a 30-year £400 million bond at a rate of 1.625%.

Although the Isle of Man borrowed in a different currency, the finance minister believes it is it still a credible indicator of current market conditions.

Whether Cayman would be able to achieve a similar interest rate should indeed be investigated.

However, currently, 30-year US Treasuries trade at 2.1%, well above the coupon paid by the Isle of Man. Any potential Cayman bond issue would be priced as a spread above the equivalent US Treasury, in other words higher than 2.1%.

Bermuda, which has a slightly lower credit rating and more debt than Cayman, issued two US$675 million bonds in mid-2020. Bermuda’s 10-year bond pays 2.375% interest and the 30-year bond has a 3.375% coupon. At the time, that was 195 basis points, or 1.95 percentage points, above the price of 30-year US Treasuries.

Repayment terms

The minister said the Isle of Man bond issue was “half the rate the previous Government agreed” for its credit facility.

However, a bullet bond and a bank loan are subject to entirely different repayment terms and total costs.

A bullet bond typically attracts additional fees above and beyond the fees it would cost to arrange a bank loan. Repaying existing loans with the proceeds of a bond issue may also incur additional prepayment penalty fees. This will have to be factored in, if the intention is to repay existing bank loans with the proceeds of a bond issue.

Crucially, even if the interest rate is lower, the repayment terms of a bullet bond may potentially make it more expensive than a bank loan.

That is because the interest on a bullet bond is paid on the entire face value of the bond issue each year for the life of the bond. In other words, a $400 million, 30-year bullet bond pays annual interest on the entire $400 million, 30 times.

In contrast, a bank loan would be paid down gradually, with interest being applied to a balance that diminishes over time.

If government were to convert its $403 million loan facility into a permanent loan, it would have to pay US$1,833,333 plus interest every month for 15 years.

This raises the question as to how a 30-year bullet bond would be repaid. Would government establish a dedicated fund and add money each year so that, three decades from now, the entire value of the bond can be repaid? Or would government simply leave it to whoever is in charge then to refinance the debt?

The Isle of Man government, for instance, said it would put about £260 million of its £400 million bond issue straight into reserves.

The Opposition leader said he would not use a bond issue to raise debt, even if the bond was smaller and of a shorter duration. He argues that revenue should be the first and main source of spending. And if debt is unavoidable, he would borrow from local banks.

“My preference would be to keep that money here in the economy, rather than paying it every year to overseas or foreign investors.”

Saunders said whichever type of debt government selects, the matter would be debated in Parliament.

Related Videos

Michael, I’ve been talking about the strategic value of this (including with Martha) since very soon after the pandemic began.

Would be very happy to talk to you about this as a Caymanian with decades of experience of and in our economy as well as internationally.

This is not a political issue, it is one of strategic long term nation building. I also agree with the pros and cons Marla noted. I hope people read beyond the top line of the issue to those details.

“If you put the federal government in charge of the Sahara Desert, in 5 years there would be a shortage of sand.” Milton Friedman, 1980

Bullets are often fatal.

Generally speaking we should be proud of our government.

However it’s a fact that no government anywhere in the world can produce anything. All they can do is spend money given to them by taxpayers or borrowed.

The money that is borrowed must be paid back with interest. Thus in the future either more money must be taken from taxpayers or even more money borrowed, creating a never ending spiral of debt.