Equity markets saw their worst week since the pandemic on fear over escalation of a global trade war.

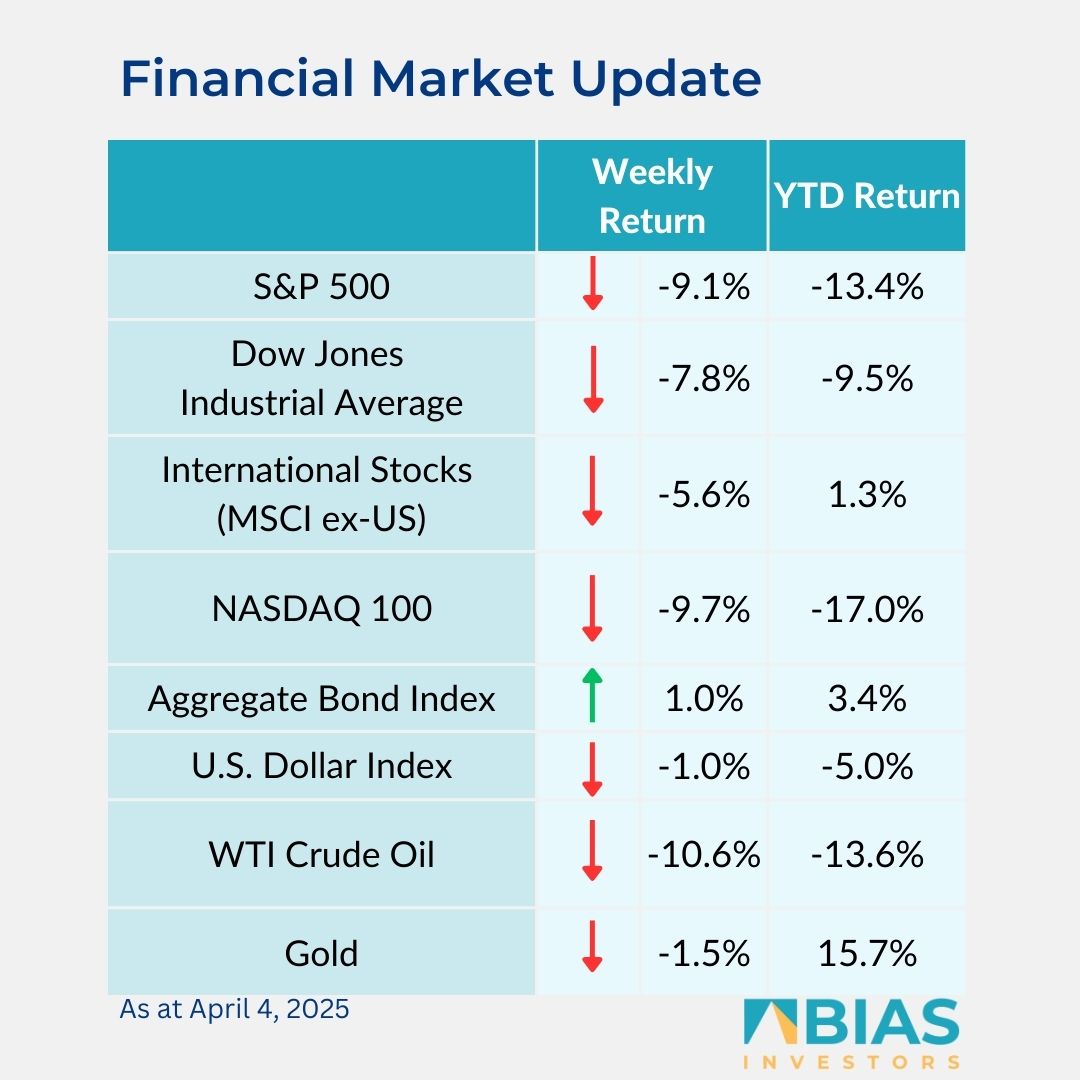

For the week, the S&P 500 Index was -9.1%, the Dow Jones Industrials -7.8%, and the NASDAQ -9.7%. All 11 sectors in the S&P 500 Index had a negative return.

The least negative were the consumer staples, utility, and real estate sectors, while the largest declines were in the energy, technology, and financial sectors. The 10-year U.S. Treasury note yield decreased to 4.013% at Friday’s close versus 4.259% the previous week.

Investor concerns over what the tariffs could do to economic growth have caused a sell-off in stocks globally. Equities tend to decline in periods of uncertainty.

As the situation evolves and some clarity returns to outlooks, equities should stabilise. Multiple nations have reached out to the US regarding trade negotiations and as those show signs of progress so should stock prices.

In other economic headlines, the March Employment Situation report showed 228,000 net new jobs created versus an expectation of 140,000. February jobs were revised down to 117,000 from previous report of 151,000.

The March unemployment rate rose to 4.2% from 4.1% in February. This week’s calendar brings reports on inflation with the March Consumer Price Index (CPI) scheduled for Thursday and Producer Price Index (PPI) on Friday. Current CME Fed funds futures indicate there could be up to 1% in reductions to the Fed funds rate by December.

Nine companies in the S&P 500 Index are scheduled to report first quarter earnings this week. First quarter 2025 earnings growth is currently forecast at 7.0% y/y with 4.2% revenue growth. Full-year 2025 earnings are expected to grow by 11.3% with revenue growth of 5.4%.

In our ‘Dissecting headlines’ section, we look at news on tariffs.

Dissecting headlines: Tariff update

The US introduced a new baseline 10% on goods from all countries and selectively higher tariffs on countries with higher current tariffs on US goods or high trade deficits.

Among large trading partners, the tariff rate is 34% on China, 20% on the European Union, 24% on Japan, and 25% on South Korea.

China responded by announcing increased tariffs on US goods. The European Union is meeting to propose a strategy. Some smaller countries highly reliant on the US as an export market, to include Vietnam and Taiwan, have reached out to negotiate lowering tariffs.

While nothing is imminent in terms of changing policy, we should see movement among many of the countries to negotiate a solution to the announced tariffs.

The concern surrounding tariff policies we see playing out in the stock market is the impact to economy and if tariffs will cause a recession.

Tariffs charged on imported goods would be inflationary if those tariffs were passed along to consumers in higher prices.

Consumer spending in all forms, both goods and services, accounts for roughly two-thirds of US Gross Domestic Product (GDP). Business and government spending make up the remainder of GDP with about equal shares.

Businesses may be reluctant to spend money when the economic outlooks are uncertain. When growth weakens, the government often enacts stimulus measures to stem economic declines and incentivise growth.

The current policy to reduce government spending may limit some spending, but stimulus likely happens if the consumer weakens meaningfully. Some potential offsets we see are a decline in energy prices and lower interest rates.

There has been much debate if the tariffs are intended to be a negotiating tactic or if they are meant to be permanent. They likely wind up being negotiated country-by-country with the goal of creating the fairest trade terms for the US. The stand-off with China is likely to take longer to see a resolution.

Ultimately, earnings growth in companies is the key factor to stock prices. The potential impact of tariffs on earnings will be the most important outcome of the upcoming earnings reporting period.

![]()

BIAS Investors

24 Howard Street

Corporate Plaza Suites #81

Godfrey Nixon Way

George Town, Grand Cayman

Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos