Friday’s speech from Fed chair Jerome Powell rallied the S&P 500 Index to a gain for the week as expectation for a September interest rate cut rose.

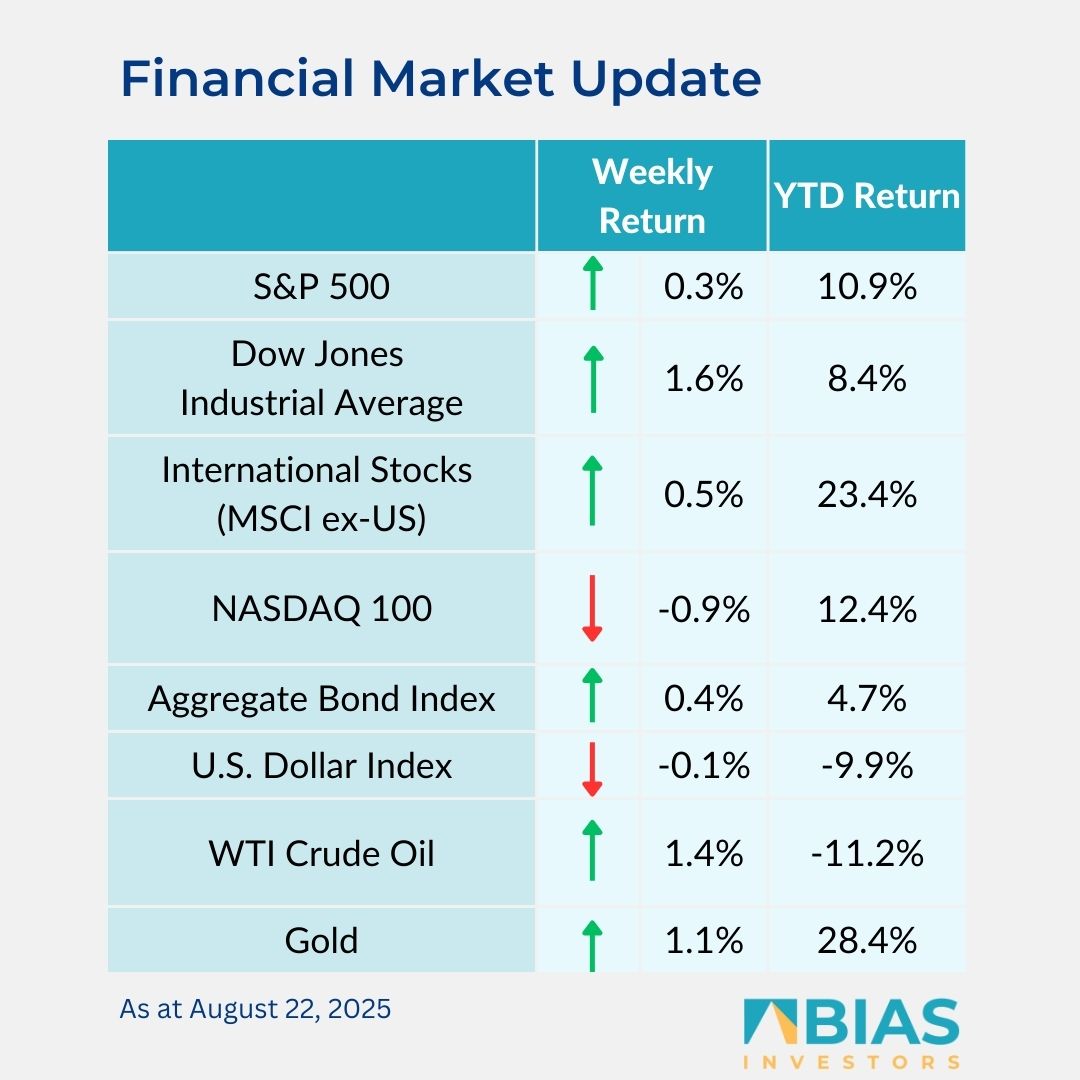

For the week, the S&P 500 Index was +0.3%, the Dow Jones Industrials +1.6%, and the NASDAQ -0.9%. The energy, real estate, and financial sectors led the S&P 500 Index for the week, while the technology, communication services, and consumer staples sectors lagged.

The 10-year US Treasury note yield decreased to 4.257% at Friday’s close versus 4.321% the previous week.

At the Federal Reserve Economic Policy Symposium, Fed chair Jerome Powell said that with monetary policy still in restrictive territory, the baseline outlook and shifting balance of risks may warrant adjusting the policy stance.

The market widely regarded this commentary as an indication of an interest rate cut at the September Federal Open Market Committee (FOMC) meeting.

Current CME Fed funds futures are projecting two 0.25% rate cuts for 2025, starting at the September meeting. One 0.25% cut is also projected for the first quarter of 2026.

Key events on the economic calendar this week include Consumer Confidence for August scheduled for Tuesday, and the Personal Consumption Expenditures (PCE) Price Index scheduled for Friday.

More than 95% of companies in the S&P 500 Index have reported earnings for the second-quarter earnings period. This week, eight companies in the S&P 500 Index are scheduled to report earnings.

With these few reports remaining, S&P 500 Index earnings growth expectations for the quarter are 11.8%, up from 4.8% at the start of the reporting period, and revenue growth is expected at 6.3%, up from 4.2%. Full-year 2025 earnings are expected to grow by 10.3% with revenue growth of 5.8%.

In our ‘Dissecting headlines’ section, we look at the potential shift in Federal Reserve sentiment.

Dissecting headlines: Hawks and doves

‘Hawkish’ and ‘dovish’ are often used to describe the disposition of the Federal Reserve or its officials.

‘Hawkish’ describes an action or disposition to raise interest rates. Increasing rates is meant to curb inflation. This can increase the cost of borrowing and can tighten economic conditions.

‘Dovish’ conversely describes the action or disposition to decrease interest rates. This is meant to stimulate economic growth and employment through less restrictive conditions.

For most of the year, the data-driven policy stance at the Fed has leaned neutral to ‘hawkish’, with the premise that the widespread tariff actions would lead to an acceleration in inflation.

Recent break in sentiment from Fed governors Michelle Bowman and Christopher Waller, who are more concerned about employment stability than inflation, led to two dissenting votes at the July FOMC policy meeting.

This is a rare occurrence as a two-vote dissent last occurred in 1993.

One role of the Fed chair is often seen as working to create consensus among the voting members of the FOMC.

Jerome Powell has sided with the ‘tariffs are inflationary’ premise, so far this year, but his comments at the Jackson Hole Symposium last week took on a more ‘dovish’ tone, and appear to be setting the stage for at least an initial 0.25% reduction in the Fed funds rate at the September meeting.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos