CFA, MBA

Equities declined for a third consecutive week.

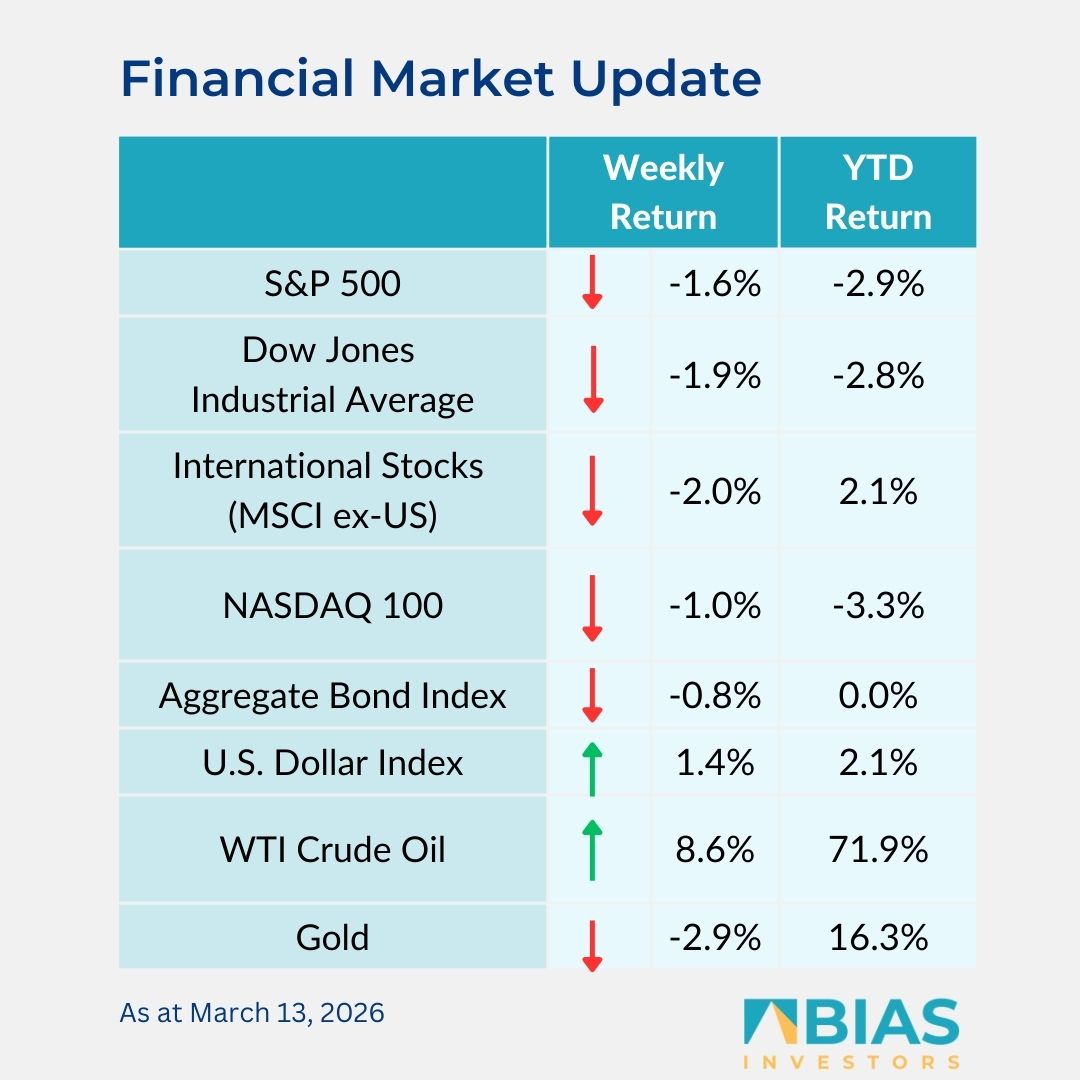

For the week, the S&P 500 Index was -1.6%, the Dow Jones Industrials -1.9%, and the NASDAQ -1.0%. The energy, utilities, and consumer staples sectors led the S&P 500 Index for the week, while the financials, industrials, and consumer discretionary sectors lagged.

The 10-year US Treasury note yield was 4.284% at Friday’s close versus 4.146% the previous week.

The ongoing conflict with Iran has pushed energy prices higher across the world. In the US, the average price of regular unleaded gasoline is $3.675 per gallon.

This is 7.7% higher than a week ago and 25.4% higher than a month ago. Diesel fuel is higher at $4.942 per gallon, up 9.6% from a week ago and up 35% from a month ago.

The concern about energy-induced inflation has pushed out investor expectations for a Federal Reserve interest rate cut.

At the Federal Open Market Committee (FOMC) policy meeting this week, the FOMC is widely expected to keep short-term interest rates in the 3.5% to 3.75% range.

There will also be an update to the Fed’s Summary of Economic Projections including what the FOMC views at an appropriate interest rate policy path for the remainder of 2026.

The projection from the December meeting showed a single 0.25% interest rate reduction for 2026, and that is reflected in the CME Fed funds futures for October.

This week, 10 companies in the S&P 500 Index are scheduled to report quarterly earnings. First quarter earnings are expected to grow by 11.6% and quarterly revenue growth is expected at 9.4%. Full-year 2026 earnings are expected to grow by 15.3% with revenue growth of 8%.

In our ‘Dissecting headlines’ section, we look at actions intended to lower energy prices.

Dissecting headlines: Oil reserve releases

The conflict in Iran has severely curtailed the flow of oil coming from the Persian Gulf, which accounts for 20% of the world’s oil production.

The International Energy Agency (IEA), an intergovernmental organisation representing 32 member countries to include the United States, Japan, Germany, South Korea and most European nations, confirmed plans for a coordinated 400 million-barrel release from government and industry strategic reserves.

The 400 million barrels would help bridge the supply disruption from the Persian Gulf for about 2-3 months. IEA member countries hold over 1.2 billion barrels of petroleum reserves.

As part of the IEA release, the US plans to release 172 million barrels from its Strategic Petroleum Reserve over the next 120 days.

The Trump administration indicated it plans to replenish the reserve with about 200 million barrels within the next year, exceeding the amount withdrawn. The US Strategic Petroleum Reserve currently holds about 415 million barrels of oil.

In addition to the release of reserves, the US, European Union, and other interested nations, are in discussions to protect shipping through the Persian Gulf.

The EU currently secures shipping in the Red Sea to make sure commercial shipping can move through the Suez Canal.

As the conflict enters its third week, the markets likely remain volatile in the near-term.

![]()

BIAS Investors (Cayman) Ltd.

Grand Pavilion (Hibiscus Way)

802 West Bay Road

Grand Cayman, Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos