Large investors have slashed their allocations to equities to the lowest level since the 2008 financial crisis and hold more cash than in the last two decades.

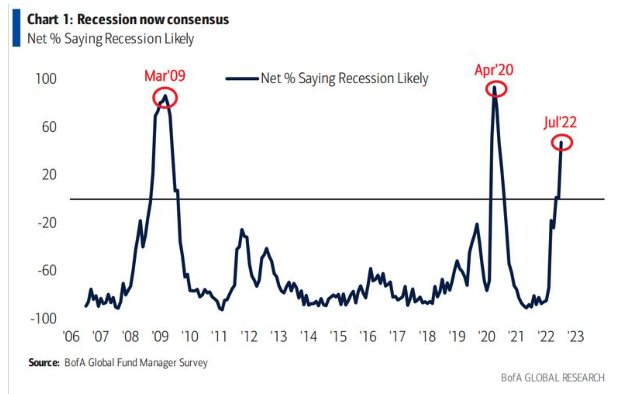

Meanwhile, recession fears are at the highest since May 2020 at the start of the COVID pandemic and global growth expectations are at an all-time low, according to a Bank of America survey of 259 investment managers with combined assets of $722 billion.

Michael Hartnett, the bank’s chief strategist, wrote in a research note that investor sentiment had reached a “dire level” of pessimism.

Although investors believe that US inflation may be peaking and, in fact, are betting on lower inflation next year, a worsening of the energy crisis in Europe and the risk of a potential recession continues to dampen sentiment.

The study carried out in the week through 15 July, followed the worst performance of global equity markets in the first half of a year for more than five decades.

During that period, the FTSE All-World Index lost close to 21% and the S&P 500 finished the first six months down 20.6% – the steepest first-half decline since 1970. The Nasdaq dropped 29.4% and Russell 2000 lost 23.9%.

During that period, the FTSE All-World Index lost close to 21% and the S&P 500 finished the first six months down 20.6% – the steepest first-half decline since 1970. The Nasdaq dropped 29.4% and Russell 2000 lost 23.9%.

More than half of the professional investors (58%) said their risk-taking is below average, a level that is higher than during the global financial crisis, as investment managers are particularly concerned with high inflation, lower corporate profit growth expectations and quickly rising interest rates.

Bank of America’s own Bear/Bull indicator is at zero, the most bearish it can be.

Yet, that may a sign a contrarian rally in the stock market could come next. “Sentiment says stocks/credit rally in coming weeks,” BofA analysts said.

But a longer-term recovery would require inflation to come down, no adverse credit events and a half to Federal Reserve interest rate rises by the end of the year.

With a recession more likely than ever, this risk may not be fully priced into the equity markets as yet.

The survey showed regionally investors are most bearish on Europe and Japan, while they shun bank, tech and consumer stocks.

The favoured trades are betting on a stronger US dollar, as well as rising oil and commodity prices and increased exposure to staples, utilities and healthcare.

Related Videos