A new study published last week provides a glimpse of the presence some of the largest U.S. corporations have in the Cayman Islands and other offshore financial jurisdictions.

At least 366 of the Fortune 500 companies have subsidiaries in “tax havens” as of the end of 2016, according to a report by the U.S. Public Interest Research Group and the Institute on Taxation and Economic Policy – two left-leaning think tanks in Washington D.C. that call for higher taxes on corporations.

The most popular jurisdiction among Fortune 500 companies is the Netherlands, with more than half of them setting up a subsidiary there. About 57 percent of the 366 companies set up one or more subsidiaries in Bermuda or the Cayman Islands, states the report, “Offshore Shell Games 2017.”

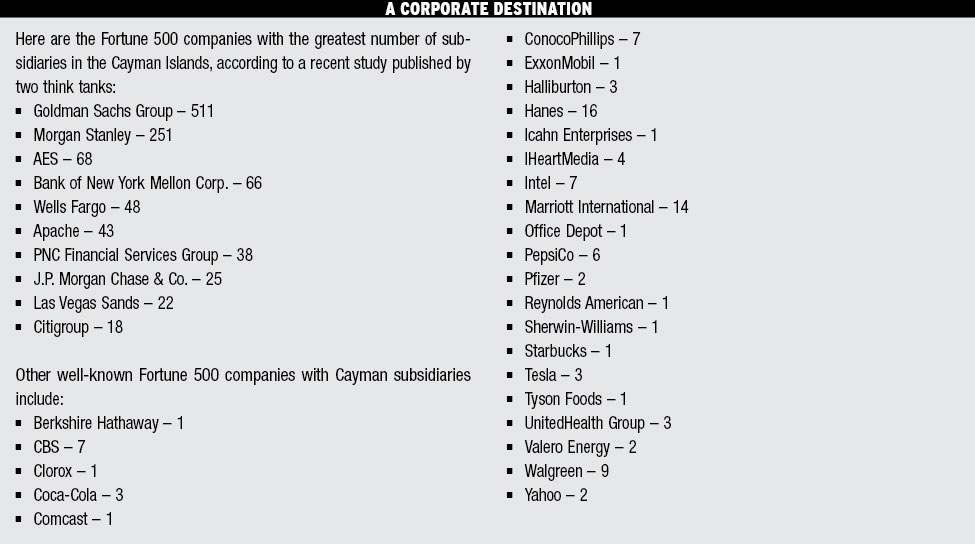

The Fortune 500 firm with the largest presence in Cayman is Goldman Sachs, which had 511 subsidiaries registered here at the end of 2016, according to the report.

Other corporations with companies registered in Cayman include Pepsi, Marriott, and Pfizer. Multinationals report roughly US$46 billion in profits here, the report states.

The think tanks define a “tax haven” as a jurisdiction with low or zero taxes, laws that encourage financial secrecy, and a “general lack of transparency in legislative, legal or administrative practices.” The report put Cayman under this definition – a classification that Cayman Finance strongly disputed in a press release on Monday, and one that Cayman attorney Anthony Travers called a “confused pseudo analysis of a highly complicated subject.”

The think tanks estimated that the U.S. multinational corporations hold some US$2.6 trillion offshore, costing the U.S. federal government some US$100 billion in tax revenue per year. The organizations compiled their data and estimates by analyzing U.S. Securities and Exchange Commission filings, Federal Reserve statistics and other studies.

To solve that alleged shortfall, the think tanks recommended that the federal government taxes the foreign profits of U.S. corporations. Currently, foreign profits are only taxed once they are repatriated to the U.S.

“The most comprehensive solution to ending tax haven abuse would be to stop permitting U.S. multinational corporations to indefinitely defer paying U.S. taxes on profits they attribute to their foreign subsidiaries,” the report states. “In other words, companies should pay taxes on their foreign income at the same rate and time that they pay them on their domestic income.”

Such a proposal is contained in U.S. President Donald Trump’s plan to change the country’s federal tax system.

“To prevent companies from shifting profits to tax havens, the framework includes rules to protect the U.S. tax base by taxing at a reduced rate and on a global basis the foreign profits of U.S. multinational corporations,” the proposal reads.

Mr. Trump is also proposing a one-time repatriation tax rate for multinationals, rumored to be around 10 percent, according to a Bloomberg article earlier this month.

In response to the report, Cayman Finance issued a statement on Monday affirming that the territory is a valuable contributor to the global economy. “Cayman is a premier global financial hub, efficiently connecting law abiding users and providers of investment capital and financing around the world,” said Cayman Finance CEO Jude Scott. “Cayman is an excellent extender of value for the U.S., U.K. and other major economies, helping to pool global investment capital and financing for major initiatives like infrastructure development.”

Mr. Scott also disputed the study’s characterization that Cayman encourages financial secrecy, pointing to a raft of transparency agreements the territory is committed to.

“Cayman is a transparent jurisdiction due to our combination of a verified beneficial ownership regime, the adoption of more than twenty global financial standards and adherence to both U.S. FATCA and the EU’s Common Reporting Standards,” he said, adding, “We meet none of the descriptions used by entities such as the OECD or Transparency International to define a tax haven.”

Mr. Travers, a senior partner of Travers Thorp Alberga, disputed the think tanks’ findings in much harsher terms.

“The use of the Cayman Islands in these circumstances is firmly rooted in United States tax law which intends that U.S. corporations should be in a position to trade globally without being subject to double taxation and therefore provides very specific deferral provisions. These are not ‘loopholes,’ but have a firm and incontrovertible foundation in U.S. tax law,” he said in an email to the Cayman Compass.

“Reports such as the U.S. PIRG report, which lack discipline in their analysis, serve no useful basis for any technical analysis of prospective revisions to U.S. tax law.

“Any such revisions need to contemplate and protect the preeminent competitive standing of U.S. corporations engaged in legitimate global trade or propose alternative effective measures,” he said.

Related Videos