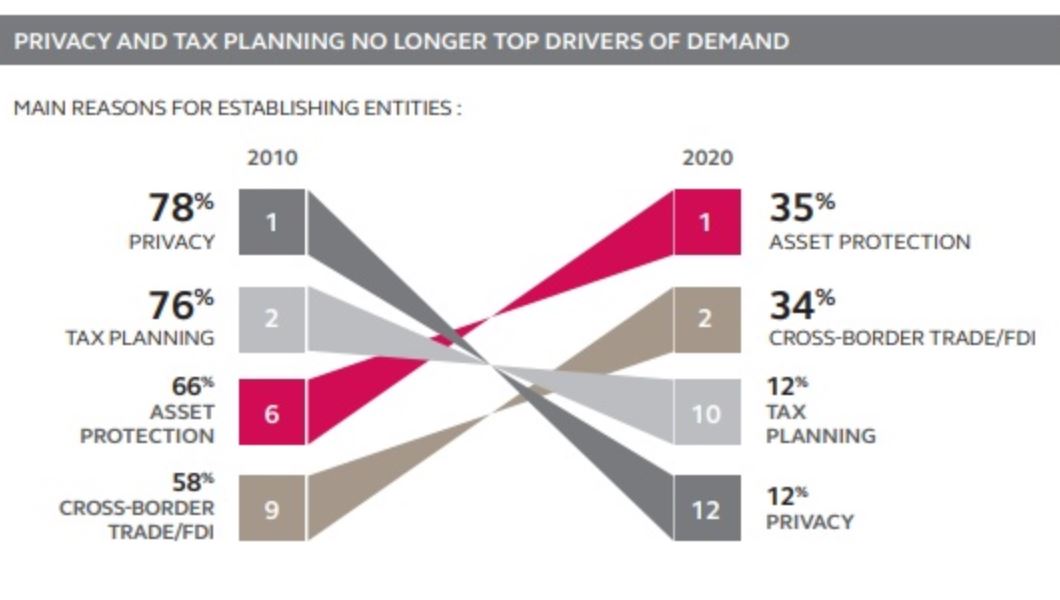

Asset protection and facilitating foreign direct investments are now the main reasons for establishing entities offshore. This is a drastic change from 10 years ago, when privacy and tax planning were at the top of the list, a study by corporate services provider Vistra has found.

The report, based on 620 interviews of industry experts, noted that respondents who relied on the British Virgin Islands and Cayman Islands for their offshore entities valued “stability, expertise and flexibility” as the most important attributes.

“When we launched this study a decade ago, the corporate services industry looked very different,” Jonathon Clifton, Vistra’s regional managing director for Asia-Pacific, said in a press release. “The industry was heavily fragmented, with a lot of single jurisdiction operators and niche providers. Since then, the industry has experienced unprecedented change with increased regulatory requirements and major geopolitical and economic shifts.”

The study shows that given the changing demands for offshore services and the greater complexity of cross-border business, respondents are less confident about their firm’s growth prospects amid the global COVID-19 pandemic.

The study shows that given the changing demands for offshore services and the greater complexity of cross-border business, respondents are less confident about their firm’s growth prospects amid the global COVID-19 pandemic.

Just 38% said they are confident, down from 75% when the study was previously done in 2018. Only 32% are confident about the ease of doing business across borders, down from 61% two years ago.

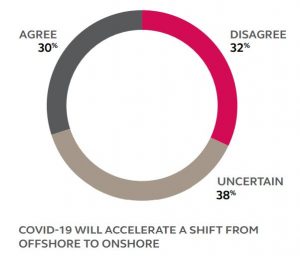

The uncertainty extends to the question of how COVID-19 is going to impact the onshore versus offshore dynamic. While 30% of respondents said the pandemic will accelerate the shift away from offshore, 32% said the opposite and 38% are uncertain.

In this uncertain climate, the report found some reasons why offshore centres would remain attractive.

In this uncertain climate, the report found some reasons why offshore centres would remain attractive.

Industry practitioners are less inclined to believe that regulatory cooperation across borders is going to increase. For the first time since 2015, the survey is seeing a declining share of participants who predict greater international convergence on information sharing, beneficial-ownership registries and tax-accounting standards.

In the current environment, governments are more concerned about their own corporations than tax transparency, the report noted.

Moreover, financial services professionals are questioning that global alignment on these measures is realistic within the next five years. In particular, the US stance against both national and harmonised rules for digital taxes has been a knock to multilateralism.

While privacy has been eroded, the process was slower than expected. Following FATCA, the common reporting standard and the European Union’s fifth anti-money laundering directive, the EU continues to push for more transparency. The UK’s exit from the EU makes it likely that trusts will be within the scope of future anti-money laundering legislation, the report said.

Privacy appears to be fading more slowly than survey participants had expected in 2017, when 30% predicted that beneficial owners’ privacy would be almost entirely eroded by 2022. Today only 5% of respondents think this is the case.

Although tax mitigation is no longer a dominant reason for using offshore structures and there will be more pressure on demand in the short term, the report argues tax-planning services are going to survive the decade ahead and that tax competition will eventually return.

Because of extensive government intervention in the economy in response to COVID-19, most governments are going to seek to recoup this spending through higher taxes, with corporations and the wealthy the main targets.

Meanwhile, the proliferation of regulations in recent years is not necessarily an obstacle for the industry, the report said.

As offshore centres have been among the early adopters of new regulations, one respondent noted that for clients more regulation is now in fact becoming a draw. “Ironically, if clients are now choosing between two jurisdictions, they would go for the one that has more robust regulation,” said the managing director for the Middle East at a corporate services firm.

The introduction of economic-substance legislation, following pressure by the EU with its tax blacklist, “has undoubtedly diminished some of the cost advantages associated with the likes of the Crown Dependencies and British Overseas Territories”, according to the report.

“But we believe there is a long-term role for tax neutral jurisdictions with strong legal systems, which are well regulated and share information globally, to help connect disparate parts of the global economy. In times of political tension, these jurisdictions not only serve as global connectors, they provide a neutral layer between sparring factions.”

Jurisdictions such as the BVI and Cayman have also become systemically important in the global financial services industry, Vistra said, with publicly listed companies, pension funds and sovereign wealth funds relying on the jurisdictions’ legal systems, professionalism and compliance measures.

“We believe that jurisdictions such as BVI, Cayman, the Channel Islands and Bermuda will still be thriving 10 years from now,” the report concluded.

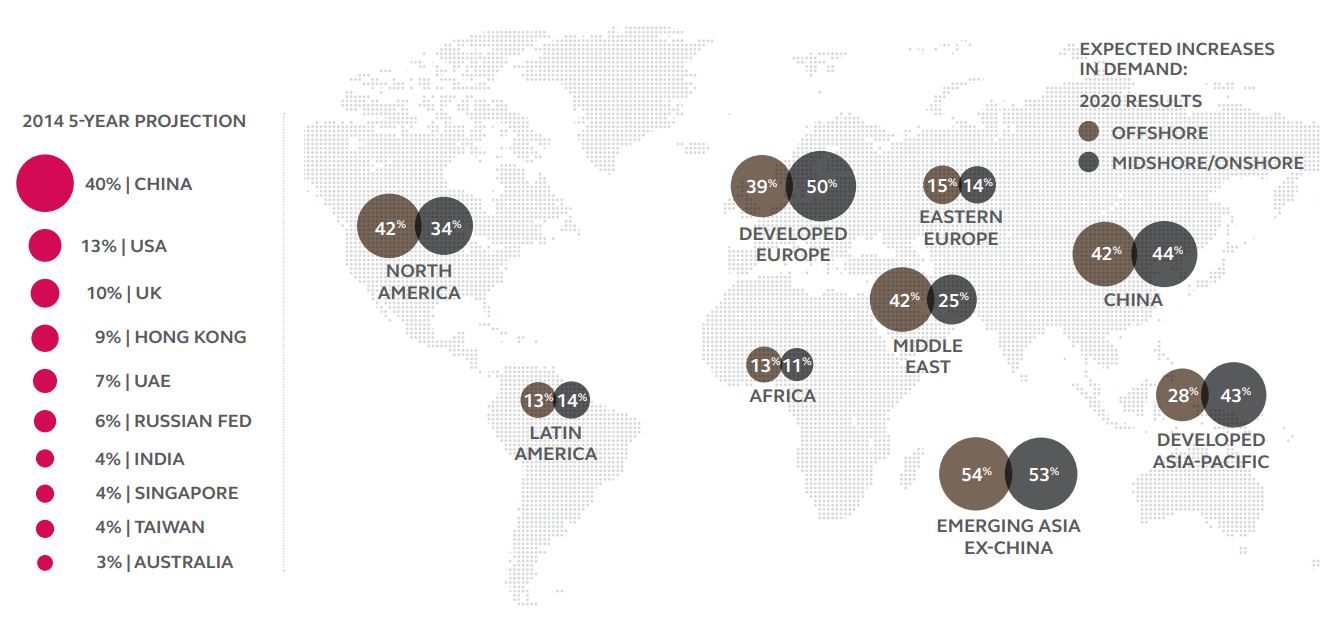

Future demand for offshore services is likely to come from emerging Asian countries, rather than China.

In light of the tensions between the US and China, industry practitioners are now questioning the long-held belief that China will be the main source of new business.

More than half (54%) expect rising demand for company-formation jurisdictions to come from emerging Asia, excluding China, and 42% cite China as a major source of increased demand.

Related Videos