Written by Marla Dukharan; Research fund by CFA Institute

With a population that reached roughly 60,000 pre-pandemic, about half of whom are non-resident/expatriate, the Cayman Islands has one of the smallest populations and the highest GDP per capita in the Caribbean, and indeed, the fifth highest globally in 2019 at almost US$93,000, according to the United Nations.

Cayman’s well-developed financial services sector and business domicile have attracted companies from around the world for decades, while its breathtaking landscapes and unparalleled experiences drove its tourism sector to average annual growth above 6% over the decade prior to the pandemic. These economic pillars have underpinned the creation of 12,288 jobs in the last 10 years, including 4,275 for Caymanians.

Cayman has a highly dollarised economy, where the US dollar is widely accepted as a means of payment and settlement, and over two-thirds of the deposit base is held in US dollar versus the Cayman Islands dollar. A currency board arrangement governs the issuance of the CI dollar, such that it is always fully backed by the US dollar and is therefore a strong and stable currency. As a matter of fact, it is the only currency in the Caribbean that is “stronger” than the US dollar, with the currency peg established in 1974 at US$1.20:CI$1.00, which still holds today.

The Cayman Islands economy is considered to be one of the most stable in the Caribbean. It is the only country with an Aa3 credit rating and stable outlook from Moody’s, which has not changed since 1997, based on its strong fiscal and external position, and its political stability and continuity – particularly in recent years, as the then-premier was the only leader of government ever to serve two successive terms.

The country held a General Election in April 2021 and elected almost an entirely new government, but there is every indication that this level of stability and good governance will be maintained going forward in Cayman.

Cayman’s political, economic, and institutional strength, coupled with strong fiscal and monetary management, provide the foundation for long-term, sustainable resilience and growth. In fact, the Cayman Islands is the only island economy in the Caribbean to have expanded for nine consecutive years through 2019, and the unemployment rate remained below 5% for six consecutive years prior to the pandemic.

Nonetheless, the pandemic revealed the country’s high exposure to a few economic sectors, and the pandemic-driven sudden stop caused visitor arrivals to fall in 2020 to the lowest level in nearly 40 years. The financial sector was minimally affected, contracting only 0.7% year-on-year in Jan-Sept 2020, but this sector has undeniably had its share of mounting challenges in recent years.

Nonetheless, the pandemic revealed the country’s high exposure to a few economic sectors, and the pandemic-driven sudden stop caused visitor arrivals to fall in 2020 to the lowest level in nearly 40 years. The financial sector was minimally affected, contracting only 0.7% year-on-year in Jan-Sept 2020, but this sector has undeniably had its share of mounting challenges in recent years.

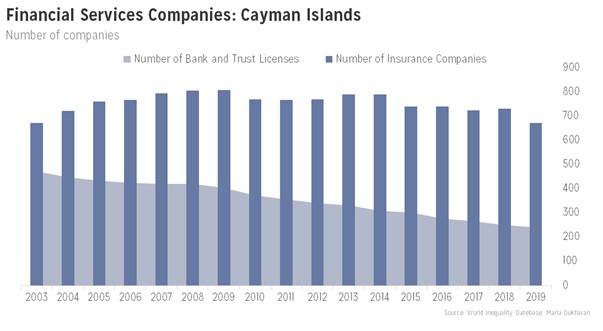

In fact, the financial and insurance services sector has been the second slowest growing sector in the economy over the last five years, averaging only 2.2% growth annually. The sub-index of banking institutions actually contracted in 2019, prior to the pandemic, by 2% year-on-year. The number of insurance companies registered in 2019 was the lowest in 16 years and less than half of what it was in the 1990s. Based on ongoing and mounting international pressure on the Cayman Islands, and on this industry more broadly, it is possible that this sector is experiencing a secular decline.

Unlike most countries in the Caribbean, Cayman’s economic activity is not dominated by the public sector, which accounts for only 5% of GDP and 14% of jobs. This is the case for two major reasons:

- The ease of doing business in Cayman is envied on a regional scale, which has underpinned this decidedly and almost uniquely private sector-driven economy.

- The fiscal rules which limit the size of the fiscal deficit and the level of debt, ensure that the government does not overspend in an effort to stimulate the economy (or buy popularity), and the state is therefore much less likely to crowd out private-sector activity, including activity in the capital market.

Cayman Islands capital market

Fiscal rules and the resulting surpluses which characterise the state’s finances, mean that there is little need for government borrowing. Indeed, as at 31 Dec. 2020, according to the finance minister, government debt stood at CI$248.6 million, and with an estimated GDP of CI$4.7 billion, translates into a debt/GDP ratio of 5.2% – certainly the lowest in the Caribbean, and one of the lowest in the world. Furthermore, the government’s bank account balances totalled CI$447.6 million, of which CI$104.3 million represents general reserves, according to the Ministry of Finance.

The government very rarely borrows therefore, even for capital expenditure. But in light of the pandemic and the possible need to finance the resulting fiscal deficit, the government arranged a precautionary line of credit with a consortium of domestic banks for US$403 million in 2020.

With respect to private sector capital market transactions, one would assume that an economy as strong, relatively well diversified, and private sector-driven as Cayman’s, ought to be supported by vibrant capital market activity. Ironically, we find that there is limited private sector capital market activity in the Cayman Islands.

Why is there limited domestic private sector capital market activity in Cayman?

The domestic banking sector currently consists only of non-indigenous banks, following the sale of Cayman National Bank to Republic Bank, which is headquartered in Trinidad and Tobago and is majority owned by that country’s government. As of December 2020, there were nine “Class A” banks and Trusts registered to operate in the Cayman Islands, which dominate the capital markets space.

These nine “Class A” commercial banks provide for a relatively competitive environment, especially when compared to most other English-speaking Caribbean territories, according to the ministry. “Furthermore, domestic lending rates are typically pegged to the US dollar prime rate, ensuring that Cayman’s bank lending rates are quite competitive,” the ministry added.

Given that all of Cayman’s domestic Class A banks have head offices/parent companies abroad, access to foreign capital becomes even easier, at least in theory. While this is a huge advantage to the borrower, it means that the local capital market could remain relatively untapped for such funds.

Financial depth

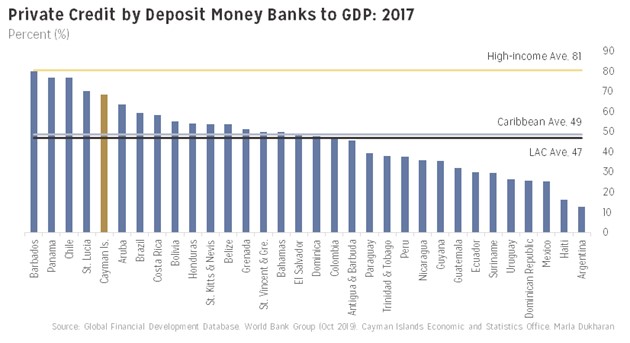

The size of the financial sector as measured by private credit to GDP is one of the highest in the hemisphere for the Cayman Islands at 68.7% in 2017 vis-a-vis an average of 47% for Latin America and the Caribbean and 49% for the Caribbean and compares more closely with high-income countries. The indicator has declined slightly in recent years for the Cayman Islands, as a result of the rapid expansion of GDP, falling to 60.3% in 2019, partly as a result of the rapid expansion of GDP.

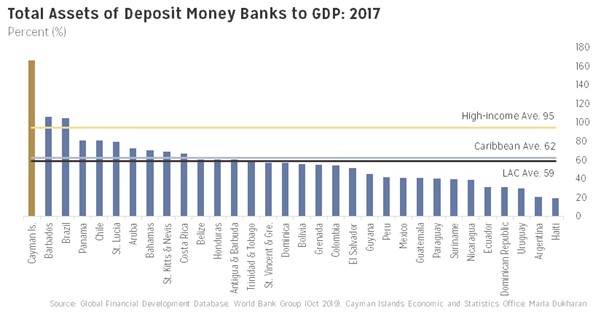

Total assets of domestic retail banks relative to GDP also stand out in the region, at 167% in 2017 as compared to the regional average, being more closely aligned with the average for high-income countries of 95%. This indicator has also declined as GDP expanded at a faster pace than domestic bank assets, falling to 148% in 2019, though remaining well above the average for high-income countries.

The highly dollarised nature of the Cayman Islands economy means that the US dollar and the CI dollar are easily interchangeable, and the CI dollar is not seen as the typical soft currency. Indeed, where domestic borrowers can access financing in US dollars, there may be a price advantage to doing so either locally or overseas, depending on the circumstances of the borrower.

The lack of constraints around access to foreign currency make lending in US dollars in the Cayman Islands less risky than in other Caribbean jurisdictions. For example, a foreign lender would be reluctant to lend US dollars to an entity operating in Trinidad and Tobago, where it is well known that access to US dollars is restricted and getting tighter by the day.

Since Cayman faces no such restrictions or tightness, formal or de facto (as is the case in Trinidad and Tobago), a domestic borrower of foreign capital can purchase any quantity of US dollars it needs at the local banks to repay its foreign debt. In fact, net foreign assets held by commercial banks amounted to 103% of GDP at the end of 2019.

According to the Cayman Islands Monetary Authority, as at Q3 2020:

-

- Retail banks issued CI$4.2 billion in non-resident debt and equity securities and zero in resident debt and equities;

- Resident financial corporations have accessed CI$47 million in loans from retail banks;

- Resident commercial private sector has accessed CI$1.2 billion in loans from retail banks;

- Total resident deposits in retail banks reached CI$9.3 billion out of CI$13.9 total deposits (67%), broken down as follows:

- Demand deposits: CI$3.6 billion

- Savings deposits: CI$3.6 billion

- Fixed deposits: CI$2.1 billion

- Other deposits: CI$4.6 billion

- Altogether, households have deposited CI$2.6 billion in retail banks.

In relative terms, therefore, local commercial banks are sufficiently capitalised and have ample liquidity to handle demands for funding. The Cayman Islands Development Bank is also a source of domestic credit to the private sector but is relatively small currently.

Because the Cayman Islands government has maintained its Aa3 credit rating as discussed earlier, this extends to Caymanian businesses being able to obtain low-cost financing on the international capital market. Larger companies can and do obtain the advice necessary to access external funding; however, it is not the primary funding source for small businesses in the Cayman Islands, according to the ministry.

So, if price and availability of liquidity are not the issue, what is?

According to CIMA, the private sector does not access the equity market to mobilise capital from investors or savers to productive sectors, partly because it is so much easier and cheaper to raise the necessary capital for business acquisition and expansion via traditional bank loans.

CIMA is also of the view that the investment culture is somewhat weak among Caymanian residents. Savings in traditional deposits in commercial banks, or investment in real estate, seem to be the preferred option among locals. Historically, there has been deep banking penetration for interest-bearing savings accounts, and for credit unions with higher rates of return and dividends, versus interest on savings accounts. The savings and investment products offered by insurance companies are also a preferred option. And finally, there is a historical or cultural preference for passive activity/rental income, and capital gains through real estate investment (especially since there is no capital gains tax).

Marco Archer, former minister of finance, and current CEO of the Cayman Islands Stock Exchange (CSX), believes that although the CSX provides a platform for the listing and trading of securities, while debt listings are huge and international, there is not sufficient participation with respect to the listing and trading of equities.

“We established a Stock Exchange 25 years ago, but to date, our equity listings are small, and, therefore, equity trading has not yet gained sufficient traction and acceptance with the average local investor. That is the demand side,” he said. “On the supply side, in addition to those local companies with debt and equity listings on stock exchanges in other jurisdictions, there are many successful and privately owned companies with sufficient liquidity and / or access to credit lines, and therefore choose not to utilise capital markets such as the CSX in order to raise capital.”

There are five entities whose equity is listed on the Cayman Islands Stock Exchange, one retail debt listing, but countless investment funds, specialist debt, corporate debt, insurance linked securities and catastrophe bonds, all denominated in foreign currencies. The debt listings are primarily by Cayman, Delaware, Irish, and UK incorporated entities and the instruments are mostly intragroup and issued outside of the Cayman Islands. This therefore ought not to be considered as Cayman capital market transactions.

Culture and policy-based restrictions are also major factors. According to Mike Anderson, managing director of RF Holdings Limited, one of the newest licensees operating in the Cayman Islands, “the capital market is not as active as it could be, and perhaps more innovative solutions would cater to the needs of the private sector entities trying to raise capital, but are unable to satisfy the traditional (real estate) asset-backed lending preferences of the commercial banking sector”.

Anderson believes that RF can play a major role in Cayman’s capital market development going forward. “Furthermore, the fact that 100% of Cayman’s domestic pension funds must be invested overseas, means that the Cayman Islands’ capital market is in effect being robbed of valuable long-term capital, which could be harnessed to invest in appropriate domestic commercial debt and equity,” Anderson went on to suggest.

Cayman’s absolute restriction on pension fund investment portfolios is unique in the Caribbean, where most countries place relatively low limits (typically around 25% maximum) on what proportion of pension fund assets can be invested abroad. It is clear that these legislated restrictions on pension funds, both in Cayman and across the region, should be reassessed with a view to optimising the prescribed mix of local versus foreign investment, and should be reviewed periodically. The International Monetary Fund has found local pension funds provide impetus for the development of local capital markets, with the institutional investor base creating positive externalities that can improve corporate performance and promote sound corporate governance.[1]

Apart from the pension fund restriction, another policy has been cited as a possible dampener on domestic capital market activity – the longstanding fixed exchange rate and currency board arrangement.

Darryl White, CEO of RBC Financial Caribbean Limited, and regional vice president of corporate and investment banking for RBC Caribbean, raised this as a possibility. “If you look at Jamaica for example in 2018 and 2019, we see that the stock exchange was the best performing in the world, and it is possible that the decoupling from the US’ monetary policy stance that a flexible exchange rate allows, could have contributed to this outcome. A foreign exchange regime such as Cayman’s gives rise to the veritable importation of US monetary policy, which may not be consistent with domestic needs and conditions, and which could affect the cost and availability of capital.”

Regulatory developments

Generally speaking, the Cayman Islands government is responsible for the drafting of acts and regulations. Following this, CIMA determines the relevant regulatory rules, policies, procedures etc., post-private sector consultation. These provide the industry with guidance on how to comply with acts and/or regulations. According to CIMA, as it currently stands, there is little-to-no market surveillance framework for the domestic capital market.

CIMA believes that the government may also wish to use a multi-pronged approach to:

- Require listing exchanges such as the CSX to allow trading and to be under regulatory supervision;

- Incentivise certain types of companies to float a number of shares on a trading exchange;

- Incentivise certain bond issues to be offered locally before they are offered internationally;

- Promote financial education and literacy, especially in areas of sound investment instruments and strategies;

- Evaluate the adequacy of consumer protection and address any gaps;

- Encourage government corporations to tap capital debt markets for their funding needs.

Additionally, the government may consider launching a national mutual fund or unit trust that would mop up liquidity and mobilise savings away from bank deposits, towards such mutual funds and unit trusts that would be listed to provide for liquidity.

The core drawback in using commercial banks to fund business ideas is banks’ tendency to over-focus on collateral and securitisation of loans, which is clearly the case in Cayman.

Banks are generally less likely to favour innovative, high-growth potential projects, having a bias towards lower risk. It is generally accepted that this is not conducive to entrepreneurship and growth of micro, small and medium enterprises in general. This creates a gap in terms of a new company’s ability to access capital where no collateral is available.

The ministry shared that the government has taken steps to address this gap by making funds available via the Cayman Islands Development Bank. The Cayman Islands Centre for Business Development was also established to assist small businesses with training and support. The centre also provides incubation offices and managerial support to maximise their credibility and ability to access financing, the ministry stated.

The ministry also shared that a sovereign wealth fund (SWF) has been proposed and remains on the agenda for the government. Indeed, past governments have established other funds that are unique to particular industries and situations, but the concept of a broader scale fund remains a conceptual idea at this time.

Certainly, questions surrounding the SWF’s scope and how it is funded must be considered keenly, preferably via public consultation. Additionally, how to entrench the SWF so that its objective and function is maintained across governments is also a major consideration.

Conclusion

The Cayman Islands economy is probably the best-run in the Caribbean. It is stable and prosperous, carrying the highest credit rating in the region, not having suffered any downgrades since its rating with Moody’s was established in 1997. The economy is driven mainly by private sector activity, and the government is relatively small and carries a net cash position.

The capital market in Cayman is therefore relatively small and quiet and is dominated by retail banks who prefer to lend against (real estate) assets. Much of the economic activity is supported through foreign direct investment (FDI) which also occurs largely outside of the local financial system, dampening the impact these activities have on financial development. However, we believe that a few policy amendments could help to support greater activity in this space.

In the first instance, relaxing the restrictions placed on pension funds, for example, could help to bring that liquidity back home, and drive the cost of capital down, and improve liquidity. It is also possible (with appropriate legislation) to channel some of that liquidity towards small and medium enterprises, who otherwise would not be able to access credit from the commercial banks if they do not have (real-estate) assets to leverage.

And finally, pension funds are an important source of long-term capital that could be used prudently to finance the sustainable development and resilience needs of a country. The Cayman Islands has been identified as one of the most vulnerable to sea level rise[2], and climate adaptive infrastructure spending may soon become a more urgent priority.

Changing the framework governing the CSX could also play a role in fostering a culture of issuing and investing in debt and equity instruments. And finally, building a strong regulatory framework for the CSX and for capital market activity more broadly, would underpin borrower and investor confidence.

[1] IMF, The Development of Local Capital Markets: Rationale and Challenges, WP/14/234, December 2014.

[2] Moody’s Investors Service, Sea level rise poses long-term credit threat to a number of sovereigns, https://www.moodys.com/research/Sovereigns-Global-Sea-level-rise-poses-long-term-credit-threat–PBC_1175883, January 16, 2020

Related Videos