Fear trumped greed to lead equity markets lower last week, mainly from concern over the economic impact of pending tariffs.

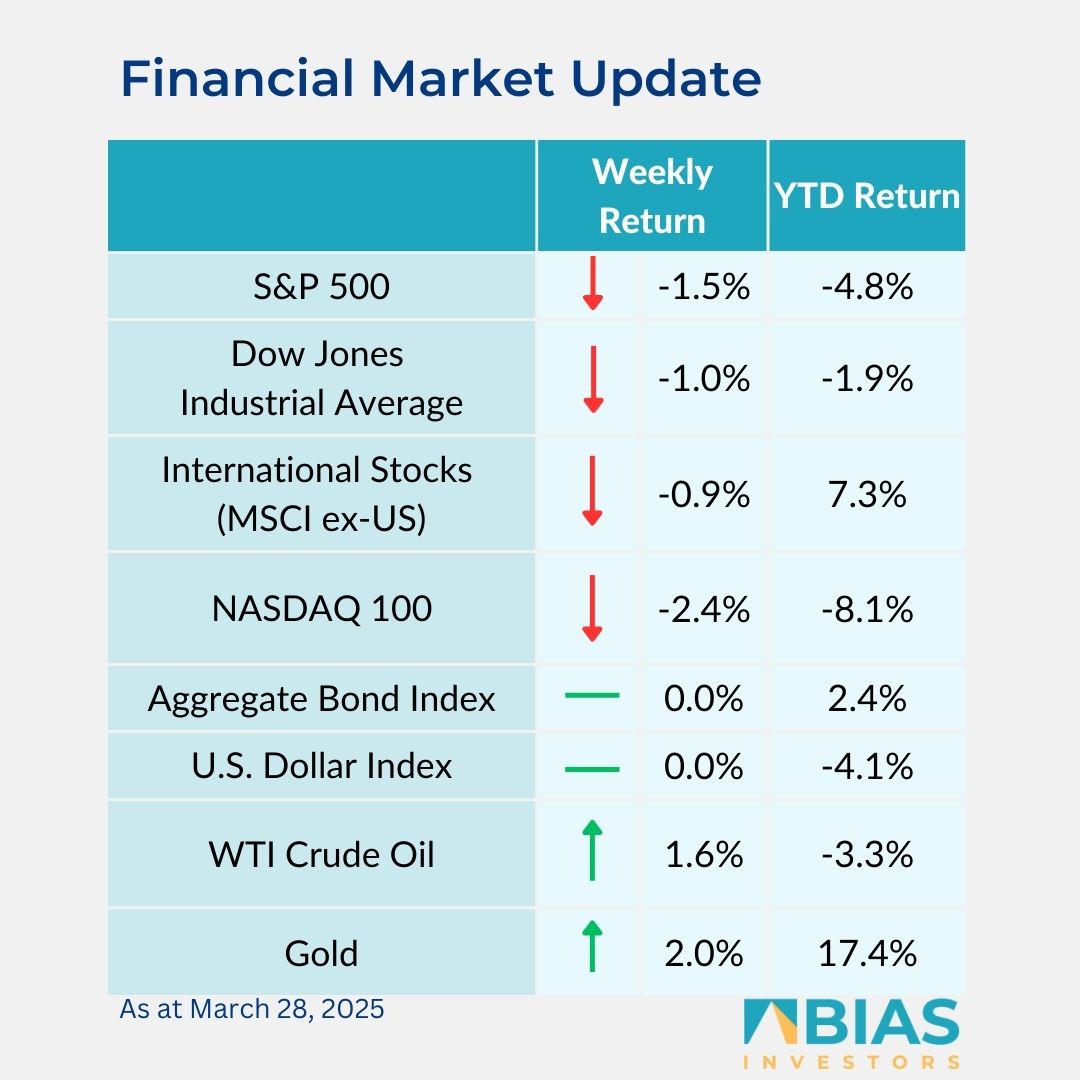

For the week, the S&P 500 Index was -1.5%, the Dow Jones Industrials -1.0%, and the NASDAQ -2.4%. The S&P 500 Index was led by the consumer staples, energy, and real estate sectors, while the information technology, communication services, and industrial sectors lagged.

The 10-year US Treasury note yield increased to 4.259% at Friday’s close versus 4.250% the previous week.

Automobile tariffs were announced for implementation on 3 April and the long-awaited reciprocal tariffs on countries that have active tariffs on US-produced goods are scheduled to be announced on 2 April.

Trade negotiations are likely to continue, country-by-country, so the economic impact and duration of tariffs are unknown. The tariff overhang has been a significant factor impacting investor sentiment for the past several weeks.

In other economic headlines, inflation remains sticky with February Personal Consumption Expenditures (PCE) Prices +0.3% month-over-month and core PCE prices, which exclude the impact of food and energy prices, +0.4% month-over-month.

Year-over-year PCE prices were +2.5% and core prices were +2.8%. This week’s calendar brings the March Employment Situation report scheduled for Friday. Current CME Fed funds futures indicate there could be up to 0.75% in reductions to the Fed funds rate by December.

Three companies in the S&P 500 Index are scheduled to report first quarter earnings this week. First quarter 2025 earnings growth is currently forecast at 7.3% year-over-year with 4.2% revenue growth. Full-year 2025 earnings are expected to grow by 11.5% with revenue growth of 5.4%.

In our ‘Dissecting headlines’ section, we look at news on tariffs.

Dissecting headlines: Everything everywhere all at once

The Trump administration announced a 25% tariff on all automobile imports effective April 3rd and select auto parts effective 3 May.

The move is designed to increase preference for US-made cars and encourage more US auto-production. Some US-flagged companies make a percentage of their cars outside of the US and import them, and some foreign-flagged automakers make cars in the US, so the impact per manufacturer is varied.

Based on data from Wards Auto, electrical vehicle makers Rivian and Tesla make all their US-sold cars domestically. This is followed by Ford at 78%, Honda at 64%, Stellantis at 57%, Subaru at 56%, Nissan at 53% and General Motors at 52%.

Other foreign manufacturers also make a reasonably high amount of cars in the US, with Toyota and BMW at 48% each, Mercedes at 43%, and Hyundai-Kia at 33%. Not all content in the vehicles is 100% sourced from the US, so the parts tariff will have impact beyond final assembly numbers.

Beyond the previously announced automobile, steel, aluminum tariffs, and tariffs announced on Canada, Mexico and China, 2 April is the day scheduled for the announcement of reciprocal tariffs equal to the existing tariffs that other countries have on US imports.

The specifics of the programme are unknown, and target countries include those in the European Union, along with Brazil, South Korea, India and others.

This large range of potential outcomes has become an overhang to the financial markets and investor sentiment during the past few weeks.

Better clarity, expected this week, could help better calibrate the economic impact. President Trump said he is open to carving out deals with countries seeking to avoid US tariffs, but those agreements would have to be negotiated after his administration announces reciprocal tariffs on 2 April.

Some successful negotiations with one or more nations could also help soothe investor concerns that there is an avenue to reduce the impending standoff in global trade.

![]()

BIAS Investors

24 Howard Street

Corporate Plaza Suites #81

Godfrey Nixon Way

George Town, Grand Cayman

Cayman Islands

W: biasinvestors.com

E: [email protected]

T: 345-943-0003

Subscribe to the BIAS Investors newsletter here.

Related Videos