A government video released earlier this year that promotes the planned cruise berthing facility offers a simple answer to the question of who would pay for the project: “It is the cruise passengers who will be paying for the cruise berthing facility and for the redevelopment of our cargo port. Verdant Isle, the preferred bidders, are merely advancing the funds to construct the facility and they will be repaid over 25 years.”

While this statement is correct in theory, things are more complicated in practice.

Details of the financing model for the project were presented at a government press conference on 29 July.

Currently, government is collecting three types of fee for each cruise passenger: A departure fee of US$7.32, a Port Authority fee of US$3 and an Environmental Protection Fund fee of US$3.90 for seasonal vessels (US$1.95 for year-round vessels).

Passengers must also pay a fee to the tender boat operators of US$5.25, bringing the total amount to between US$17.52 and US$19.47 per head depending on the type of vessel.

To fund the project, government will introduce a new fee of US$8.05 for year-round vessels and US$6.10 for seasonal vessels. At the same time, government will reduce its departure tax from US$7.32 to US$5 and passengers will no longer have to pay a tendering fee.

Both the port fee and the Environmental Protection Fund fee will remain. The total amount per cruise passenger disembarking in Cayman will thus be US$18, irrespective of the type of vessel. This means that while cruise passengers are technically paying for the project, US$5.25 that would otherwise have gone to the private tender operations and US$2.32 that would have been collected by government as revenue would go to Verdant Isle through the new project fee.

While the $5.25 is not an expense for the taxpayer, it comes at an initial cost to the economy. According to the economic impact study that was attached to the Outline Business Case for the proposed port, the direct net economic impact of the cruise berthing facility is a loss of $67 million in gross value added over 20 years, due to the loss of the tendering business. However, the impact study noted that the indirect effect of more tourists spending more money over time in Cayman, as a result of the cruise berthing facility, would outweigh the net direct economic loss over time.

Loss of future tax revenue

Government has argued that the loss of future departure tax revenue of $2.32 per passenger would be recovered over the years by a larger number of passengers arriving in Cayman because of the cruise berthing facility.

Mathematically this formula makes sense if there is an immediate jump in cruise arrival numbers to 2.5 million passengers per year – the number at which the net tax revenue would overtake what is currently levied from 1.9 million passengers. But there is no certainty that this level of growth will happen overnight or that it would be sustainable in the long term, given potential fluctuations in the global economy and other geopolitical factors which can impact tourism generally.

If we use the more conservative growth projections of government’s business case reports, the issue is less clear cut.

Do the math

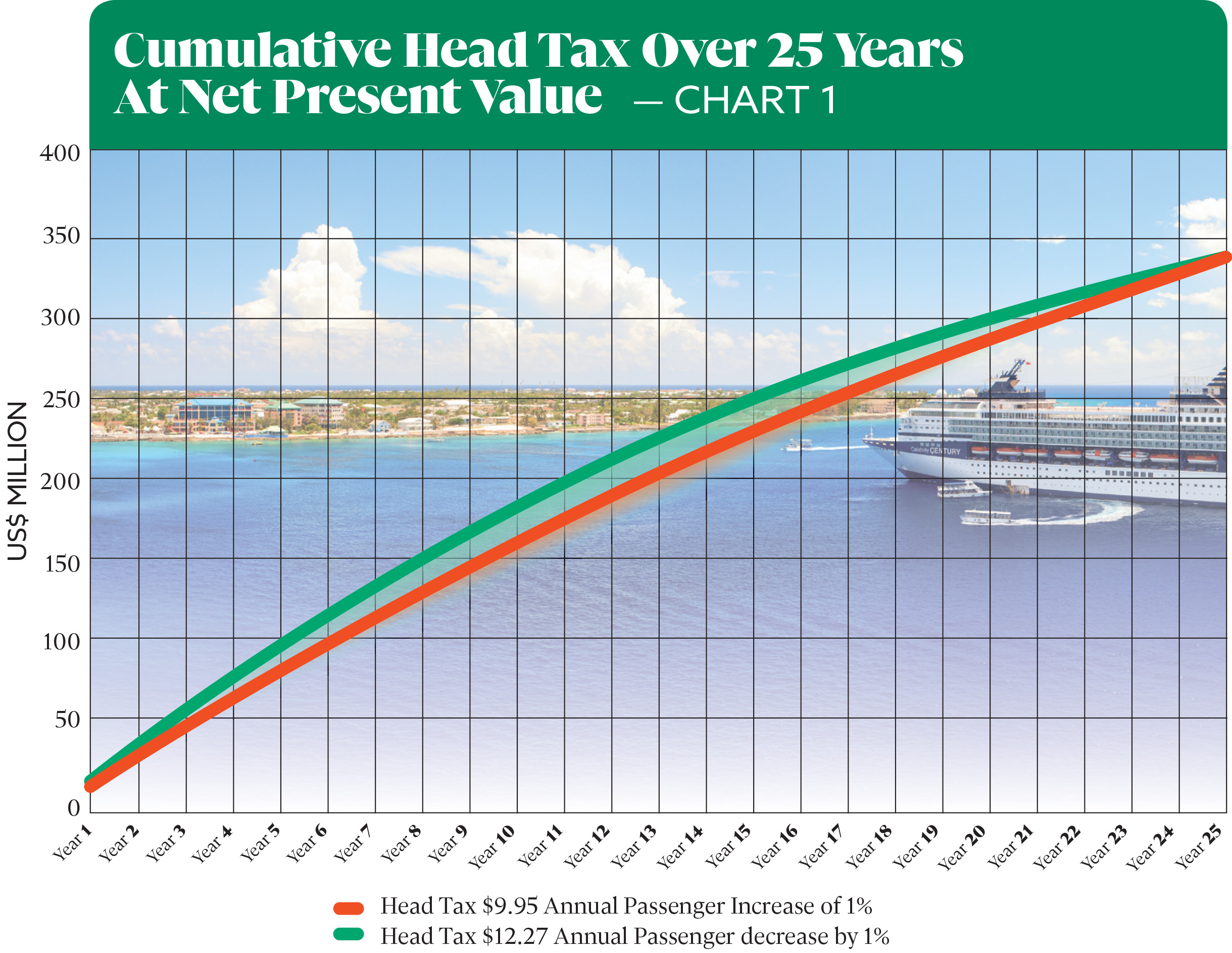

In ads on social media and its own brochure on the project, government encourages voters on the referendum to do the math. They are told that 2.5 million passengers paying $9.95 to the government would bring in more tax revenue ($24.8 million) than 1.9 million passengers paying the additional $2.32 for a total of $12.27 per person ($23.3 million).

This is true, but Cayman does not currently have 2.5 million cruise passengers.

Therefore, if we apply the base case of the economic impact study to this example, by contrasting a 1% passenger increase with a 1% passenger decline starting at 1.9 million passengers, the initial head tax revenue loss is not recovered after 25 years (see Chart 1).

There are two reasons for this: Firstly, a 1% passenger increase per year amounts to only 2.41 million passengers after 25 years, while a 1% decline would result in just under 1.5 million passengers. Secondly, the cash flows must be compared at net present value. Because of the time value of money, cashflows of equal size are more valuable, if they are received earlier. As a result, initial losses have a stronger impact than future gains of the same size.

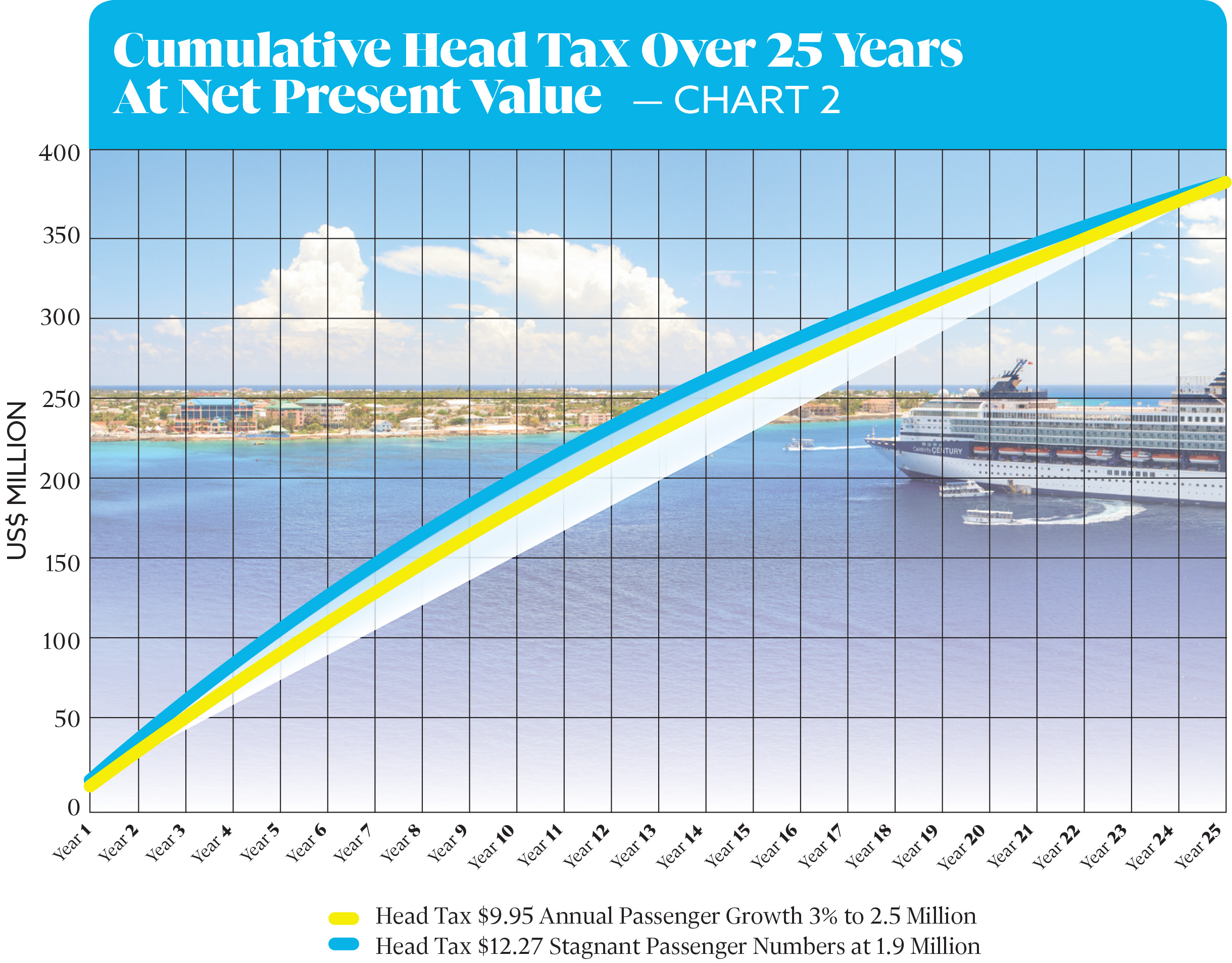

If we stay closer to the example given in government’s promotional material and assume a passenger growth rate of 3% per year, Cayman would see 2.5 million passengers in the ninth year of the project. If passenger numbers stay at 2.5 million for the remainder of the 25 years and we compare this to a stagnant 1.9 million passengers, given in the example, the tax loss would again not be recovered fully during the life of the project (see Chart 2).

To recover the initial loss of tax revenue, passenger growth – or decline, in the alternative scenario without a cruise berthing facility – will have to be stronger than originally assumed in the financing plan of the Outline Business Case.

Additional tax revenue could also come from head tax increases. During the 29 July press conference, Chief Officer Stran Bodden said the $18 total head tax “will be indexed at 2.5% per year as well”. Tax indexing is the adjustment of rates of taxation in response to inflation. In other words, it is anticipated that the fee will increase by 2.5% each year.

Related Videos