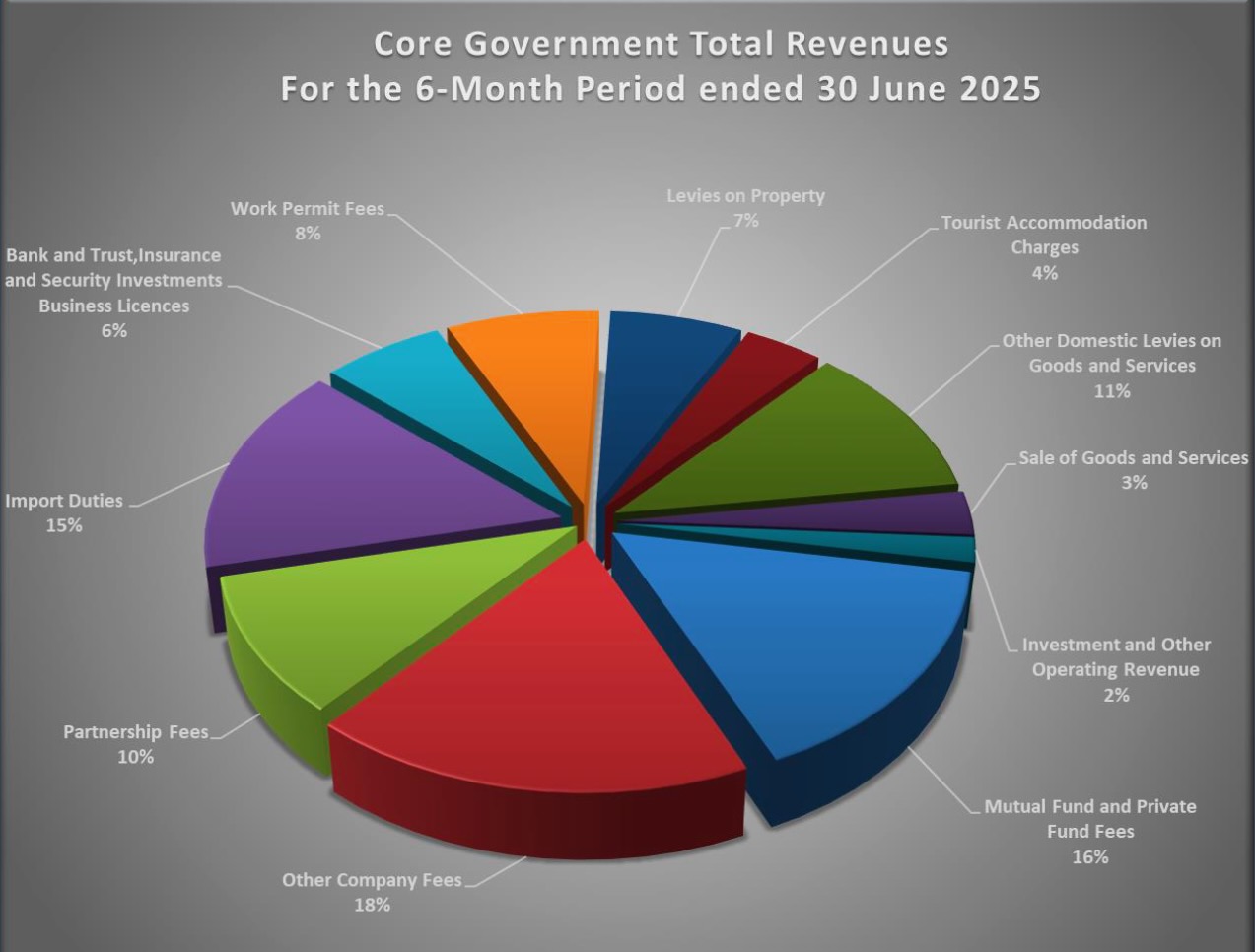

Fees from Cayman’s growing financial services sector accounted for roughly half of all government revenue in the first six months of 2025.

Government raked in more than $350 million from a mix of company fees, mutual and private fund fees, partnership fees, and bank, trust, insurance and securities licences.

That’s an increase of $51.5 million compared with the same period last year.

Rate hikes, which came into force in January, and solid business growth in the sector have helped swell government’s coffers in the first half of the year.

The influx of cash is a welcome shot in the arm at a time when government is spending more than ever and is forecast to be in a deficit position by the end of the year.

The increased income was offset by a spike in unbudgeted spending on financial assistance, healthcare, benefits for seamen and scholarships. Spending on civil service salaries and benefits have also increased substantially, as the Compass reported.

Although government had a $194 million surplus at the halfway point in the year, that is lower than at the same point last year and is expected to evaporate in the latter half of 2025. Such large budget surpluses are the norm in the first six months of the year, when most financial services fees are collected. A pre-election economic report and more recently comments from MP Wayne Patron indicate government is expecting to end the year with a deficit.

Government’s overall revenue and, in particular, the large increase over the past year are mainly due to financial services activity and fee increases.

Key areas of growth included:

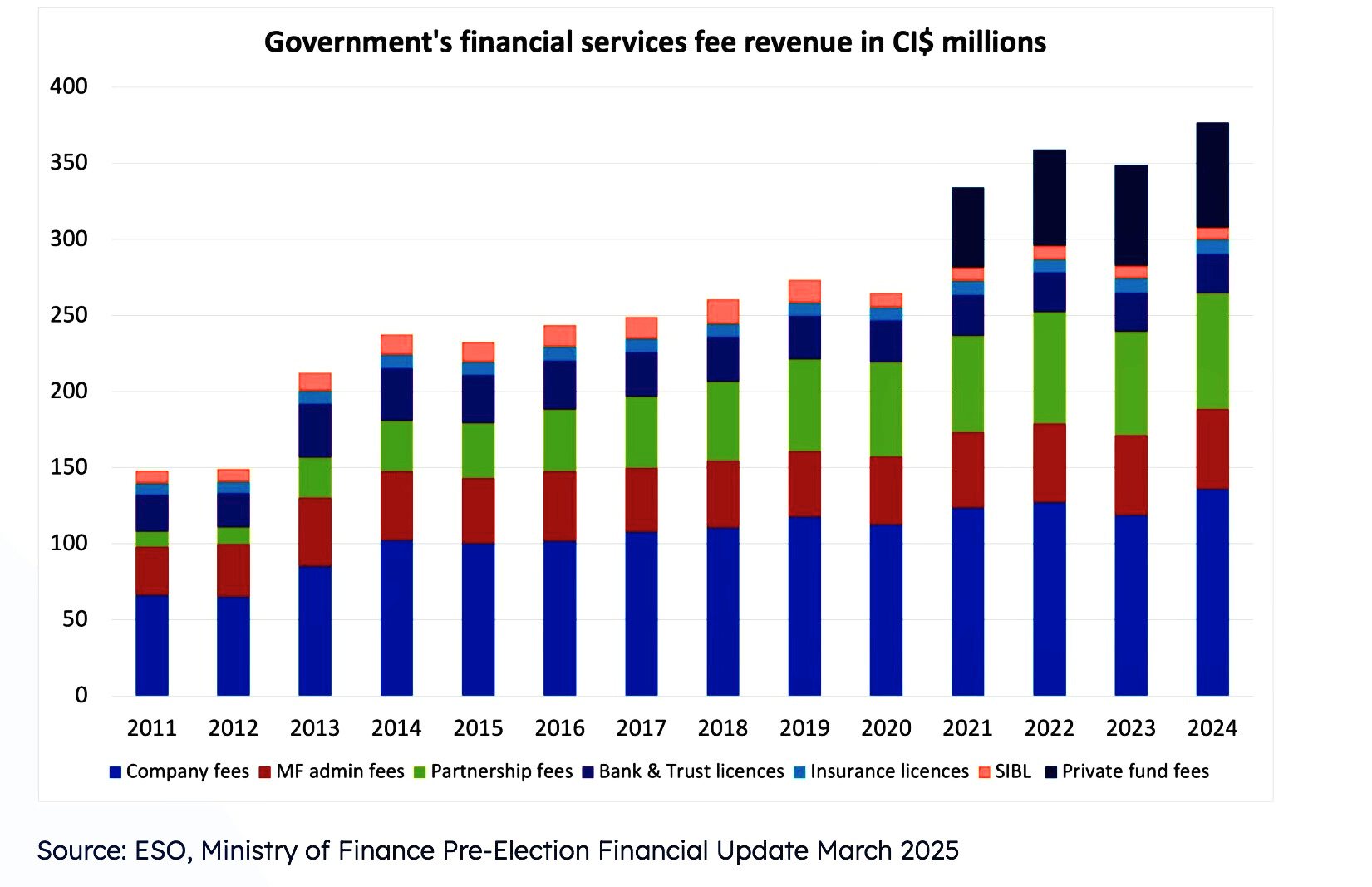

- Exempt company fees: up $17.1 million, driven by a 10% increase in fee rates.

- Partnership fees: up $8.9 million after similar rate hikes.

- Private fund fees: up $6.6 million year-on-year.

Collectively, fees from financial services made up around half of all government revenue in the first half of the year. That doesn’t account for the sector’s contribution to work permit or import duty revenue.

New companies

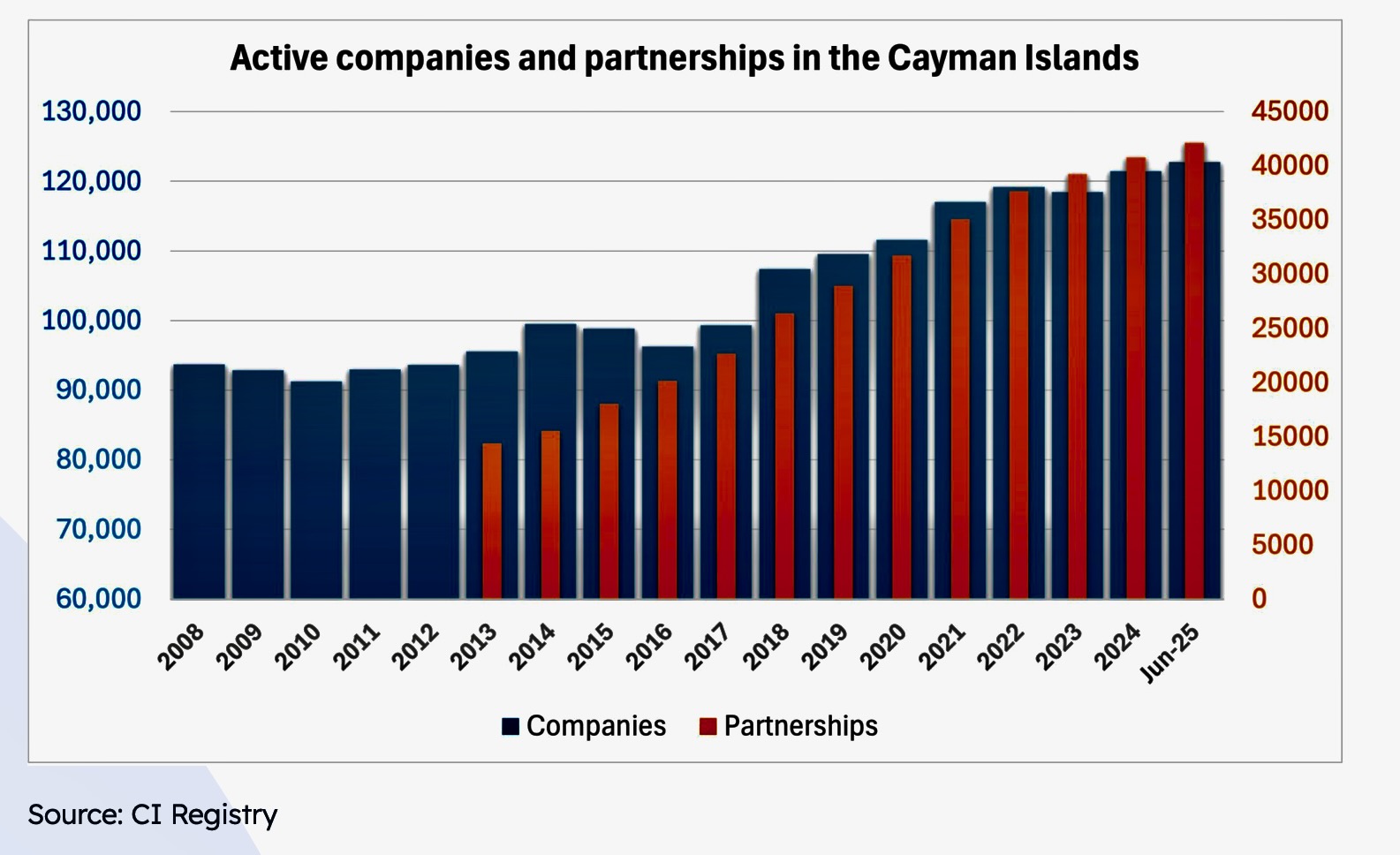

A total of 6,440 new companies were incorporated in Cayman during the first six months of 2025, according to reporting from Cayman Finance.

Data analysis on the industry organisation’s website highlights the growing contribution of the sector in the island’s economy since its nadir in 2011 in the wake of the financial crisis.

At that point, government was pulling in less than $150 million from the sector in fees – less than half of the record figures announced in the latest report.

The number of companies and partnerships has grown from 110,000 to 165,000 over the same period.

Economist and Compass columnist Simon Cawdery said the health of the sector was encouraging for Cayman. But he insisted the data should also serve as a reminder to government not to overburden the industry with regulation and red tape that could stifle that growth.

“This report is ever more evidence of how reliant Cayman and its government is on financial services. Not only are financial services essential to government’s budget but the second and third order benefits in terms of employment and spending in the community is massive,” he said.

“This report should be another wake up call to government to be careful not to kill the golden goose that has provided so much prosperity for Cayman. Regulation, immigration and work permitting issues and always-rising fees are at risk of doing to financial services what slowly boiling water does to frogs … kill them before anyone realises it’s too late.”

Anxiety about Cayman’s reliance on the financial services industry is not a new phenomenon.

Writing in this newspaper 50 years ago, Sir Vassel Johnson, the founder of the financial services industry, expressed similar concerns.

Related Videos

And more than 90% of our total revenue is spent on Govt. administration, which is why we need to fund capital projects by way of loans.