The stock markets on Thursday reacted with significant losses to President Donald Trump’s decision to ban travel to the US from 26 EU countries in an effort to contain the spread of COVID-19.

The FTSE100 was down 9.8%, the biggest one-day loss since October 1987 and its second-worst day ever. Germany’s DAX lost 11.4% and Europe’s Stoxx 600 lost 10.8%, as shares in European airlines fell by as much as 13% yesterday.

US markets deemed Trump’s address “the most expensive speech in history” with both the S&P500 and the Dow Jones losing almost 10%.

Crypto assets offered little respite to investors. Bitcoin lost as much as 24% as investors switched to ‘real’ cash, often to cover losses elsewhere.

New financial crisis?

New York University economist Nouriel Roubini took to Twitter to warn that pension funds regarded a “rolling recession” in the US and Europe as a baseline. However, he expects the recession to continue into the fourth quarter of the year.

Roubini, who is known as ‘Dr Doom’ for predicting the 2008 crisis, said the last financial crisis was caused by household debt, mortgages and leveraged banks in the US. The coming debt and financial crisis would come from corporate debt in collateralised loan obligations, leveraged loans, high-grade and high-yield bonds, commercial real estate and shadow banks. It could even affect capitalised banks with direct exposure to shadow banks, he tweeted.

Corporate debt levels, including riskier leveraged loans, are indeed at historically high levels. During the unprecedented period of very low interest rates following the last crisis, businesses have loaded up on debt.

So far, regulators are mainly concerned about the limited visibility of leveraged loan deals involving non-banks, like hedge funds and private equity funds, which have taken a significant share of the market since 2008. The Financial Stability Board estimates the non-bank lending sector has grown 75% since the financial crisis to $52 trillion in assets.

Financial regulators believe the non-bank sector is more susceptible to a sudden jump in non-performing loans because they do not have the same protection as banks against ‘runs’.

Regulated banks also have more leveraged loans on the books than in the past. Even if their direct involvement is low, they will typically invest in CLOs, composed of leveraged loans, or have exposure to the market through derivatives or prime brokerage.

The US CLO market alone has reached about $600 billion, while total leveraged loans amount to around $1.6 trillion.

In November 2018, Fitch Ratings reported that the trailing 12-month rolling default rate for leveraged loans ticked up to 1.8%; that level is still low, but a recession could change that.

Although CLOs offer diversification, spillover effects are possible, if different industries are hit at the same time by an economic downturn.

The disruption of supply chains caused by measures to curb the spread of the virus is only a precursor. The question is whether a wave of defaults and downgrades could lead to broader instability?

Bank capitalisation

This would largely depend on how quickly COVID-19 can be contained and how well-capitalised banks are. The more loss-absorbing capital banks have, the better they will withstand losses.

Banking regulators instituted new stress testing and capital requirements for banks after the last financial crisis. By and large, this led to banks being able to cope better with economic shocks than in the past.

However, the US has watered down some of these rules in recent years. And European banks are asking regulators to roll back some of the safety measures to be able to deal with the economic shock that is expected from the coronavirus.

In a letter sent to European Union authorities on Wednesday, banks asked for lower required liquidity and capital buffers and looser rules on bad loans – the reduction of the very rules designed to protect them in a crisis.

The European Central Bank has responded with a strong liquidity backstop, a reduction in capital requirements and delayed banking stress tests planned for this year.

Although these measures are positive for banks, investors rushed to sell off bank stocks on Thursday.

European banking shares like ING and ABN Amro were down 16% and 15%, respectively, while Deutsche Bank lost 14% and Credit Agricole was down 12.7%.

The ECB’s main aim is to support the credit flow to the economy, particularly for small- and medium-sized businesses that could get into trouble quickly.

The continued hammering of bank stocks indicates that investors believe the ECB measures alone, without fiscal stimulus by European governments, will not prevent a wave of corporate defaults that will ultimately load financial institutions with bad debt.

However, the nature of leveraged loans means that the potential impact of rising defaults would be gradual, especially when compared to the 2008 financial crisis. A rising cost of debt will also typically hit businesses only when they refinance – in other words, in the medium to longer term.

This gives banks and regulators some time to react. With capital still widely available at very low cost and central banks being supportive, the financial system will continue to provide banks with any needed cushion.

How long will the crisis last?

How quickly the spread of COVID-19 can be contained will determine whether there is a prolonged economic impact. With the World Health Organization declaring the coronavirus outbreak a pandemic, it is clear that, just like the flu, it will remain a regular, seasonal public health issue and not disappear.

The drastic measures taken to limit the spread of the virus by restricting the movement of people and banning large public gatherings is likely to reduce spikes and lower the maximum number of active cases.

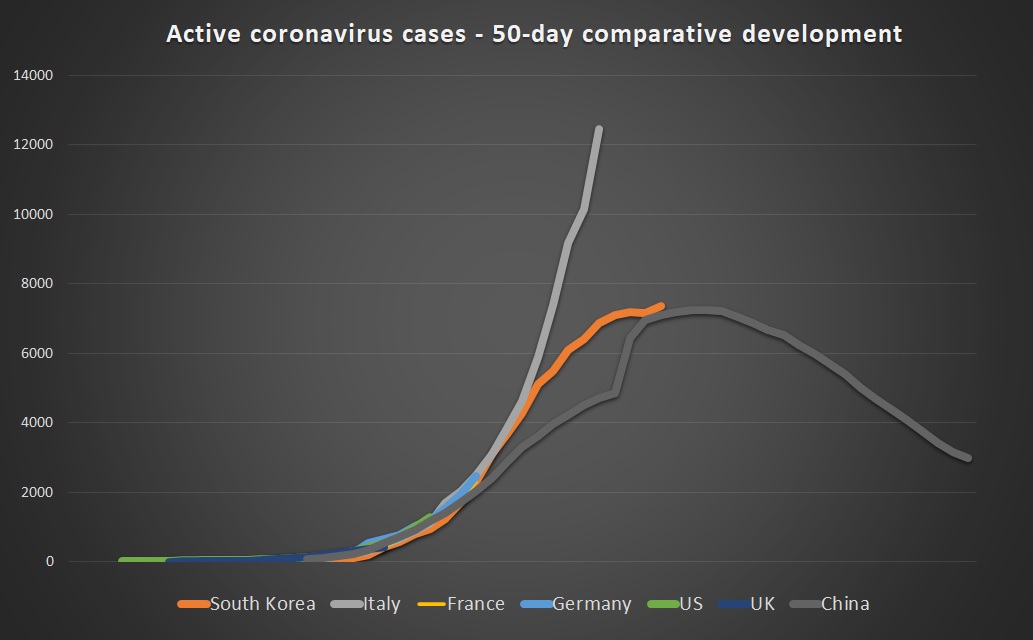

Data about the development of COVID-19 infections in China shows that only seven weeks after authorities started to count cases officially, the total number of new and active cases, as well as deaths, is declining rapidly (see chart above).

Because European countries have so far mirrored Chinese and Korean infection rates in these early stages, this year’s coronavirus outbreak could be limited to about three months in each individual country, provided the necessary measures are taken to limit infections.

Related Videos