Chief executive officers worldwide are concerned about their firms’ long-term business viability, with 45% of CEOs surveyed by PwC stating they do not expect their companies to survive beyond the next 10 years as tech and climate pressures accelerate.

PwC’s 27th Annual Global CEO Survey report, published on 17 Jan., noted, “Almost half (45%) of CEOs say they do not believe their current business will be viable in a decade if it continues on its current path – up from 39% in 2023.

The report noted that the impetus for companies to reinvent themselves is intensifying. “CEOs expect more pressure over the next three years than they experienced over the previous five from technology, climate change and nearly every other megatrend affecting global business,” it noted.

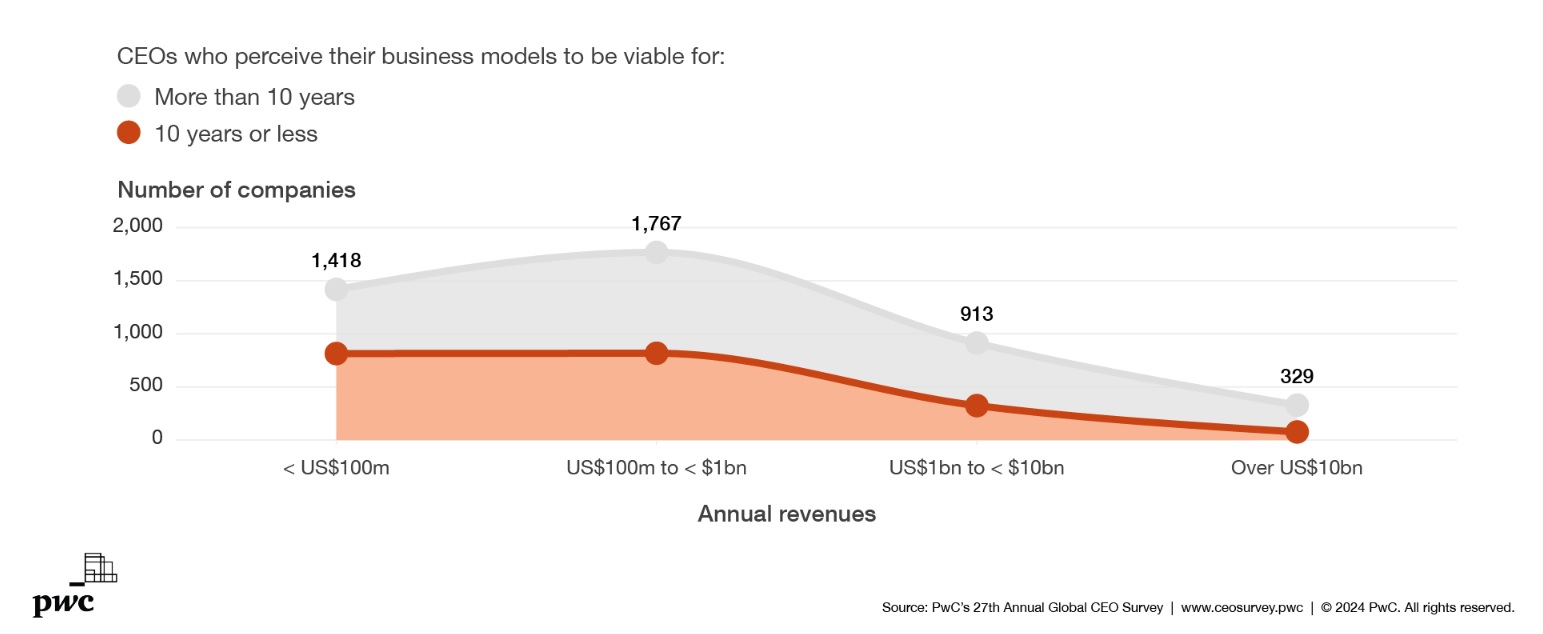

The survey shows that smaller companies are at greater risk: 56% of CEOs leading businesses generating less than US$100 million in annual revenue believe their companies will only be viable for 10 years or fewer without reinvention. This falls to 27% for those making US$25 billion or more in revenue annually.

“Reflecting uncertainty about how they will manage megatrends, CEOs are somewhat less confident than last year in their own company’s prospects for revenue growth over the next 12 months – down from 42% to 37%.”

However, despite that pessimistic outlook, the proportion of CEOs who believe global economic growth will improve over the next 12 months has more than doubled since last year, the report noted.

The survey, which interviewed 4,702 CEOs across 105 countries and territories between 2 Oct. and 10 Nov. 2023, found that 38% of CEOs are optimistic about global economic growth prospects over the next 12 months, up from 18% in 2023.

CEOs’ expectations of economic decline have also tumbled from a record high of 73% in last year’s survey to 45% this year, as perceived exposure to inflation and macroeconomic volatility fell by 16 percentage points, to 24%, and 7 percentage points, to 24%, respectively.

Despite ongoing conflicts, the proportion of CEOs who felt their company is highly or extremely exposed to geopolitical conflict risk fell 7 percentage points, to 18%.

Increasing headcounts

CEOs across all regions said they are more likely to plan to increase, rather than decrease, their headcount in the next 12 months, with 39% reporting that they expect to add 5% or more staff members.

While the trajectory is positive, “confidence is fragile as megatrends, including technological disruption – exemplified by generative AI – and the climate transition converge”, the report stated.

Graeme Sunley, PwC Cayman leader, said, “Despite rising optimism about the global economy, CEOs are actually less optimistic than last year about their own revenue prospects. Moreover, they are acutely aware of the need to transform their business to survive. If organisations globally and here in Cayman are to thrive over the short and long-term and deliver sustained value, they must accelerate the pace of reinvention.”

AI driving reinvention

CEOs overwhelmingly see generative AI as a catalyst for reinvention that will power efficiency, innovation, and transformational change, the report noted. Nearly three-quarters (70%) believe it will significantly change the way their company creates, delivers, and captures value in the next three years.

CEOs are also optimistic about the short-term impact. Over the next 12 months, almost three-fifths (58%) expect AI will improve the quality of their products or services, and almost half (48%) say it will enhance their ability to build trust with stakeholders.

They also expect better outcomes for their business – 41% expect AI to positively impact revenue and 46% expect it to positively impact profitability. The technology, media and communications sector is most positive about the impact on profit (54%), while energy, utilities and resources are least optimistic (36%).

But while CEOs are increasingly looking to the transformative benefits of generative AI, the great majority say it will require workforce upskilling (69%). They have also expressed concern about an associated rise in cybersecurity risk (64%), misinformation (52%), legal liabilities and reputation risks (46%), and bias towards specific groups of customers or employees (34%) in their companies.

Changing business models

Almost all (97%) CEOs note they have taken steps to change how they create, deliver, and capture value in the past five years, and over three-quarters (76%) have taken at least one action that had a large or very large impact on their company’s business model.

But while CEOs are taking action, they are faced with a number of challenges. Two-thirds (64%) cite the regulatory environment as inhibiting their ability to reinvent their business model to at least a moderate extent, 55% point to competing operational concerns, and 52% point to a lack of skills in their company’s workforce.

A further obstacle is inefficiency, the report noted. CEOs perceive significant inefficiencies across a range of their companies’ routine activities — everything from decision-making meetings to emails — viewing roughly 40% of the time spent on these tasks as inefficient. A conservative PwC estimate of the cost of that inefficiency would be tantamount to a self-imposed US$10 trillion tax on productivity.

The full findings of the survey can be accessed on pwc.com/ceosurvey.

Related Videos